MCU chips, short for Microcontroller Units, are highly integrated electronic components. The rise of emerging fields such as artificial intelligence, robotics, and edge computing has opened up new growth opportunities for the MCU market.

Definition of MCU

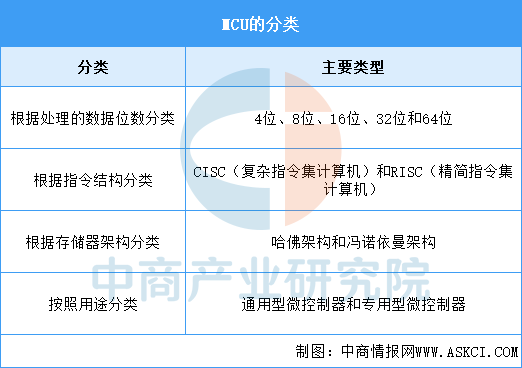

MCU stands for Microcontroller Unit, which is a highly integrated chip that combines a microprocessor core, memory, input/output interfaces (I/O interfaces), timers, and other functions into one. Based on the number of data bits processed, it can be classified into 4-bit, 8-bit, 16-bit, 32-bit, and 64-bit; based on instruction architecture, it can be divided into CISC (Complex Instruction Set Computer) and RISC (Reduced Instruction Set Computer); based on memory architecture, it can be divided into Harvard architecture and Von Neumann architecture; and based on usage, it can be classified into general-purpose microcontrollers and dedicated microcontrollers.

Source: Organized by the China Business Industry Research Institute

MCU Industry Development Policies

The national policy support for the MCU chip industry is comprehensive and multi-layered, aiming to promote the healthy and rapid development of the MCU chip industry through multiple means such as financial investment, tax incentives, talent training, intellectual property protection, and international cooperation, laying a solid foundation for the overall improvement of China’s electronic information industry.

Source: Organized by the China Business Industry Research Institute

Current Status of the MCU Industry

1. Global Market Size

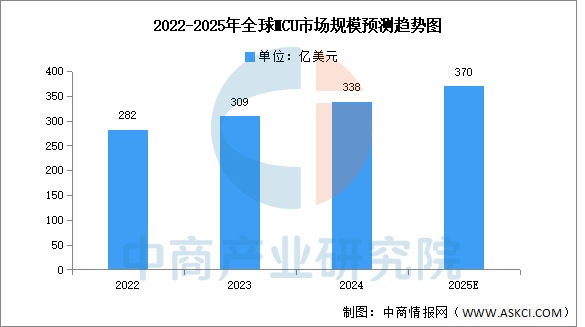

According to the “2025-2030 China MCU Chip Market Status Research Analysis and Development Outlook Report” released by the China Business Industry Research Institute, the global MCU market size continues to expand to $30.9 billion in 2023, influenced by demand from automotive and industrial AIoT. It is expected to reach approximately $33.8 billion in 2024. Analysts predict that as downstream demand continues to increase, the MCU market size will continue to grow, reaching $37 billion globally by 2025.

Data Source: Organized by the China Business Industry Research Institute

2. Chinese Market Size

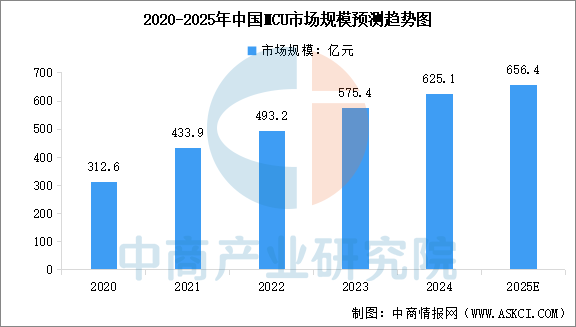

Against the backdrop of “domestic substitution” and “chip shortages”, domestic companies are accelerating the R&D, manufacturing, and application capabilities of MCU chips, gradually completing the localization in the mid-to-low-end MCU field and continuously penetrating into the high-end field, thereby enhancing the competitiveness of China’s MCU industry. The report indicates that the Chinese MCU market size will reach 62.51 billion yuan in 2024, an increase of 8.64% from the previous year. Analysts predict that the market size will reach 65.64 billion yuan in 2025.

Data Source: Frost & Sullivan, Organized by the China Business Industry Research Institute

3. Application Field Proportions

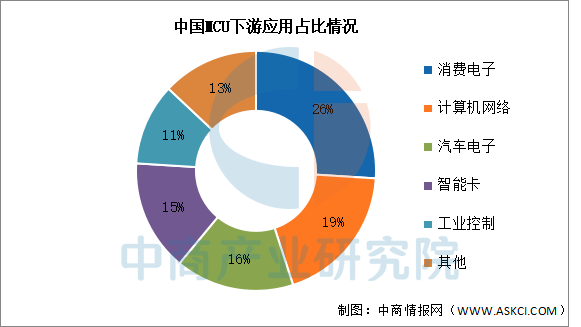

In China, the application proportion of MCUs in consumer electronics is 26%, in computer networks is 19%, and in automotive electronics, smart cards, and industrial control is 16%, 15%, and 11%, respectively.

Data Source: Organized by the China Business Industry Research Institute

4. Company Layout

The MCU industry is evolving along a dual track of “architecture upgrades + verticalization of scenarios”, with the penetration rate of RISC-V architecture exceeding 35%, and the localization rate of automotive-grade MCUs increasing from less than 5% to 18%. Technical competition focuses on high reliability (failure rate < 0.1 PPM), low power consumption (standby ≤ 1 μA), and AI integration (edge computing power ≥ 2 Tops), but high-end industrial MCUs still rely on imports (localization rate is less than 20%). Overcapacity has led to a 40% drop in consumer-grade MCU prices over three years, forcing companies to shift towards high-margin fields such as automotive and industrial control (gross margin over 50%). Geopolitical factors are accelerating supply chain localization, with the proportion of self-developed IP cores expected to reach 60% by 2025, and future breakthroughs needed in 5nm processes, functional safety certification (ISO26262), and the completeness of ecological toolchains.

Data Source: Organized by the China Business Industry Research Institute

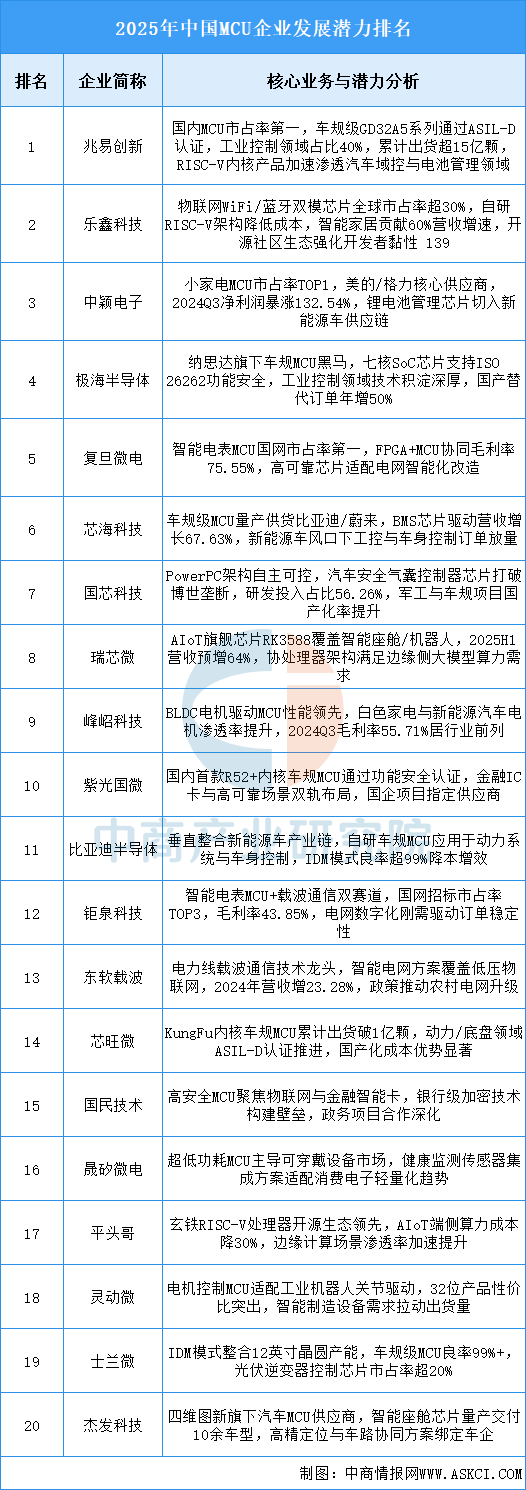

5. Company Potential Rankings

The MCU industry as a whole benefits from the threefold drive of automotive intelligence (over 100 MCUs per vehicle), AI edge computing, and domestic substitution policies (target market share of 30%+). The focus is on the penetration of RISC-V architecture (35%), high reliability of automotive-grade MCUs (failure rate < 0.1 PPM), and AI integration (edge computing power ≥ 2 Tops); however, it faces challenges such as tight supply of mature process capacity, localization rate of high-end industrial MCUs below 20%, and international ecological barriers. Growth in the next three years will depend on breakthroughs in functional safety certification (ISO26262), cost reduction and efficiency improvement in IDM models, and cross-scenario technology integration capabilities.

Data Source: Organized by the China Business Industry Research Institute

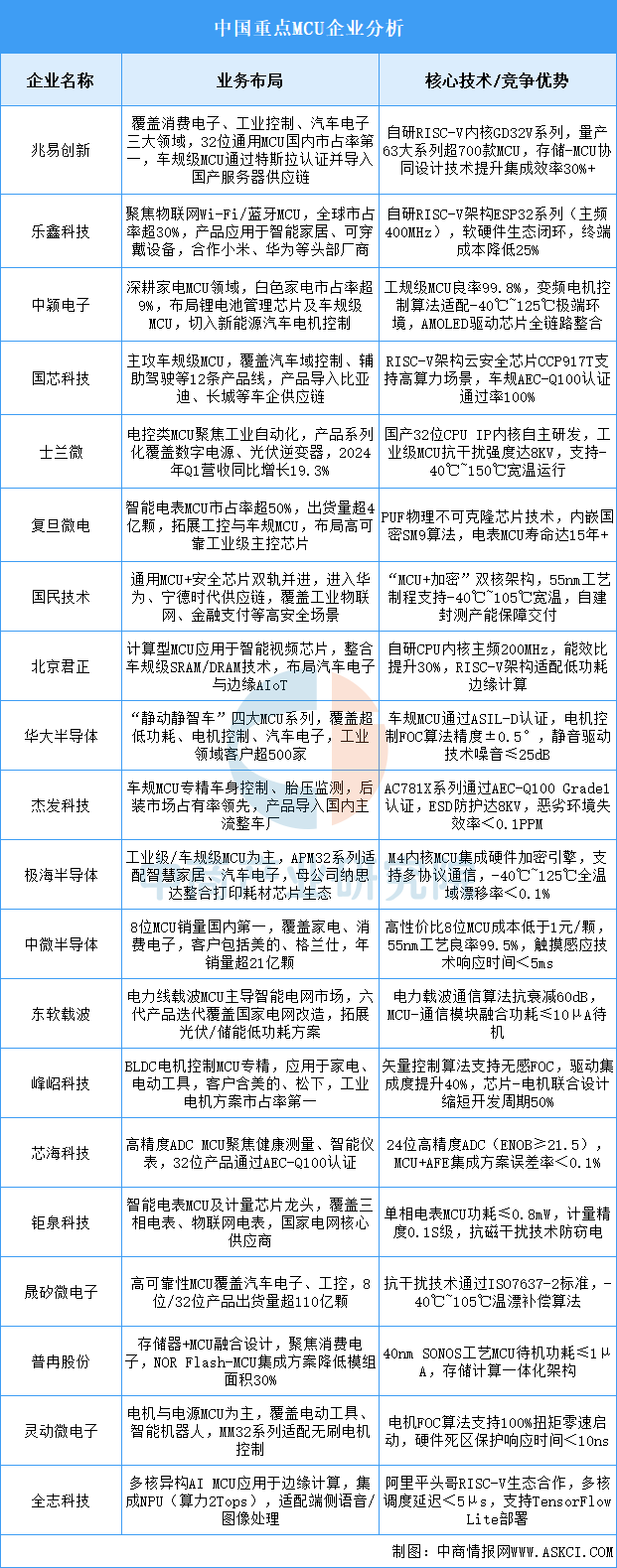

Key Companies in the MCU Industry

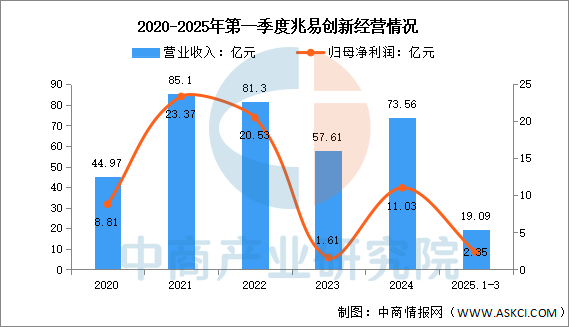

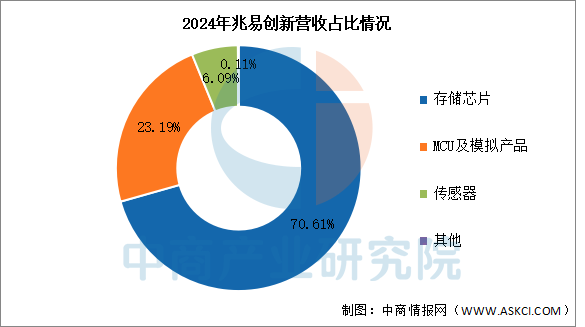

1. GigaDevice

GigaDevice Semiconductor Inc. focuses on the R&D, technical support, and sales of memory, microcontrollers, and sensors. Its main products include memory chips, MCUs, analog products, sensors, and technical services.

In the first quarter of 2025, it achieved revenue of 1.909 billion yuan, a year-on-year increase of 17.33%; net profit attributable to the parent company was 235 million yuan, a year-on-year increase of 14.63%. In 2024, its main products include memory chips, MCUs, and analog products, accounting for 70.61%, 23.19%, and 6.09% of total revenue, respectively.

Data Source: Organized by the China Business Industry Research Institute

2. Chipone Technology

Chipone Technology Co., Ltd. is engaged in IC design and sales. Its main products include industrial-grade MCUs, battery management chips (BMIC), AMOLED display driver chips, and automotive-grade MCUs.

In the first quarter of 2025, it achieved revenue of 319 million yuan, with year-on-year growth flat; net profit attributable to the parent company was 16 million yuan, down 48.39% year-on-year.

Data Source: Organized by the China Business Industry Research Institute

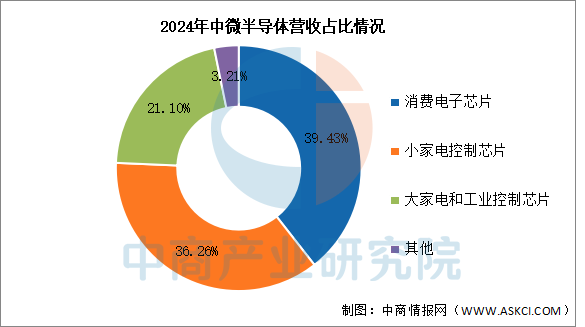

3. Zhongwei Semiconductor

Zhongwei Semiconductor (Shenzhen) Co., Ltd. focuses on the R&D, design, and sales of digital and analog chips, striving to provide chip-level one-stop solutions for smart controllers. Its main products include consumer electronics chips, small appliance control chips, large appliance and industrial control chips, and automotive electronics chips.

In the first quarter of 2025, it achieved revenue of 206 million yuan, a year-on-year increase of 0.49%; net profit attributable to the parent company was 34 million yuan, up 17.24%. In 2024, its main products include consumer electronics chips, small appliance control chips, and large appliance and industrial control chips, accounting for 39.43%, 36.26%, and 21.10% of total revenue, respectively.

Data Source: Organized by the China Business Industry Research Institute

4. Guomind Technology

Guomind Technology Co., Ltd. is engaged in the manufacturing and sales of lithium battery materials and is a leading enterprise in general-purpose MCUs and security chips in China, as well as a national high-tech enterprise. Its main products include chip products, negative electrode material sales and processing, and technical services.

In the first quarter of 2025, it achieved revenue of 304 million yuan, with year-on-year growth; net profit attributable to the parent company was a loss of 21 million yuan. In 2024, its main products include integrated circuits and key components, negative electrode materials, accounting for 50.42% and 47.06% of total revenue, respectively.

Data Source: Organized by the China Business Industry Research Institute

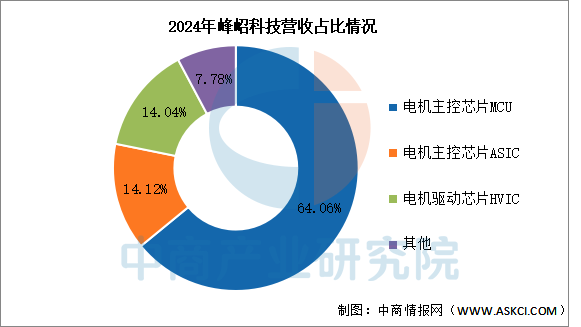

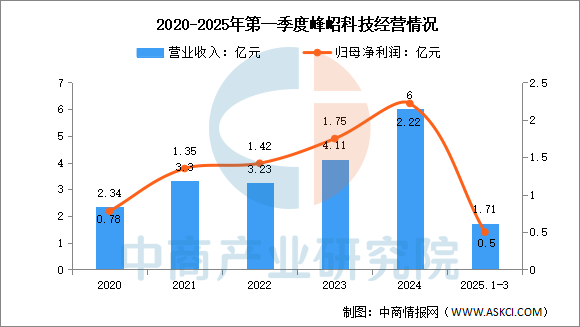

5. Fengqian Technology

Fengqian Technology (Shenzhen) Co., Ltd. focuses on the R&D, design, and sales of dedicated chips for motor drive control. Its main products include motor control chips MCU, motor control chips ASIC, motor drive chips HVIC, power devices MOSFET, and intelligent power modules IPM.

In the first quarter of 2025, it achieved revenue of 171 million yuan, a year-on-year increase of 47.41%; net profit attributable to the parent company was 50 million yuan, down 1.96% year-on-year. In 2024, its main products include motor control chips MCU, motor control chips ASIC, and motor drive chips HVIC, accounting for 64.06%, 14.12%, and 14.04% of total revenue, respectively.

Data Source: Organized by the China Business Industry Research Institute

Future Prospects of the MCU Industry

1. AI Integration Restructuring Functional Boundaries

The deep integration of edge computing and lightweight AI frameworks is driving MCUs to leap from basic control to intelligent decision-making. By integrating neural network acceleration units and multimodal perception technologies, MCUs can locally execute complex tasks such as voice recognition and predictive maintenance, significantly improving the accuracy of industrial equipment fault detection and real-time response capabilities. AI empowerment allows MCUs to break through traditional functional limitations, providing high-reliability intelligent cores for smart homes, industrial automation, and other fields, solving the computational bottleneck in edge scenarios.

2. Automotive Intelligence Driving High-End Innovation

The electrification and connectivity trends of new energy vehicles are pushing automotive-grade MCUs to iterate towards high safety and high integration. The ISO 26262 functional safety certification system forces companies to tackle core technologies such as dual-core lockstep and hardware redundancy; the demand for multi-sensor collaboration in smart cockpits and autonomous driving systems promotes the integration of communication interfaces and real-time control modules in MCUs. Technological upgrades help domestic MCUs penetrate high-end scenarios such as chassis control and battery management, breaking the monopoly barriers of overseas manufacturers in safety-critical areas.

3. Vertical Integration of the Industry Chain Ensures Autonomy and Control

Breakthroughs in the localization of upstream core components (such as VCSEL laser chips and SPAD detectors) significantly reduce dependence on imported equipment. Companies achieve full-chain collaboration from design to manufacturing by building their own wafer fabs and packaging testing lines; the low-cost energy support of green energy industrial parks further strengthens production capacity stability. Industry chain integration shortens R&D cycles and enhances product adaptability to automotive standards, providing a high-consistency supply chain guarantee for industrial control and automotive electronics.

The above information is for reference only. If there are any omissions or deficiencies, please feel free to point them out!

The “White Paper on the Development of China’s Industrial Parks (2025)” has officially started compilation.

The China Business Industry Research Institute has conducted research on the industrial chain investment map in Shandong.

The report on the construction of a modern industrial system in Linfen City during the 14th Five-Year Plan period has been successfully completed.

The China Business Industry Research Institute has conducted research on the digital, networked, intelligent, and green development of the manufacturing industry in Chuzhou City, Anhui Province.

Leaders from Shaoling District, Luohe City, Henan Province, visited our institute for inspection and exchange.

Leaders from Bayannur County, Harbin City, Heilongjiang Province, visited our institute for inspection and exchange.

Leaders from the Industry and Information Technology Bureau of Ningde City, Fujian Province, visited our institute for inspection and exchange.

Leaders from Yunfu City, Guangdong Province, visited our institute for inspection and exchange.

The “Research Report on Opportunities and Challenges of New Quality Productive Forces during the 14th Five-Year Plan in Pu’er City” has successfully passed expert review.

The “Research on Strategies to Enhance the Competitiveness of Kunming’s Service Industry during the 14th Five-Year Plan” has successfully passed expert review.

The “High-Quality Development Plan for the Photovoltaic Industry in Yibin” has passed expert review.

The “Solar Thermal Power Generation Equipment Manufacturing Industry Development Plan in Jiuquan (2023-2035)” has passed expert review.

China Business Industry Research Institute

Founded in 2002, the China Business Industry Research Institute is a new type of industrial think tank based in Shenzhen and serving the whole country. For over twenty years, it has adhered to the development concept of “Bay Area Gene, Global Vision”, with “data + platform” as the core driving force, relying on the multi-dimensional interaction of “capital + resources + projects” to provide high-value industrial consulting solutions for clients, assisting in industrial upgrading and high-quality development.

“Read the original text” to get more reports