Key Points:

Key Points:

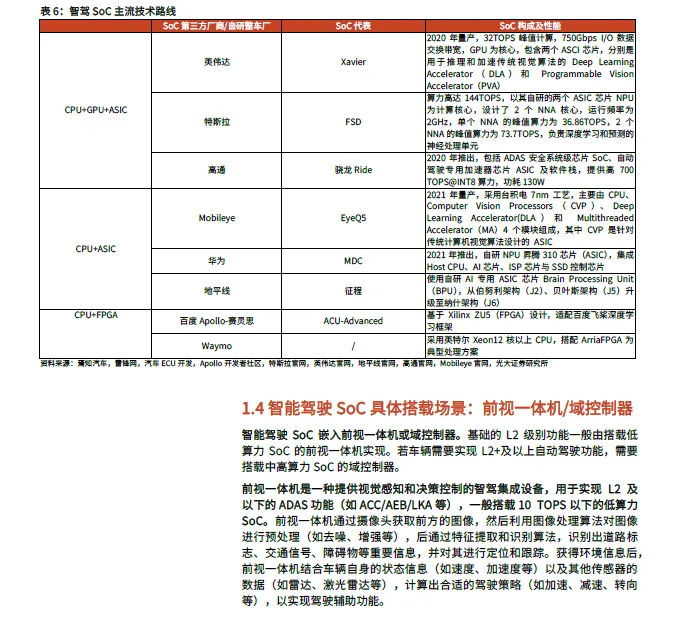

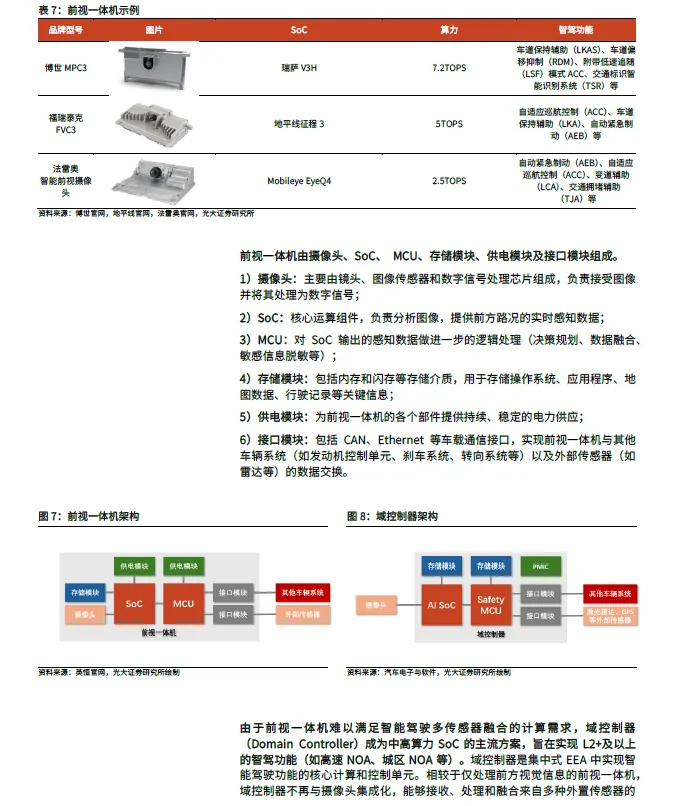

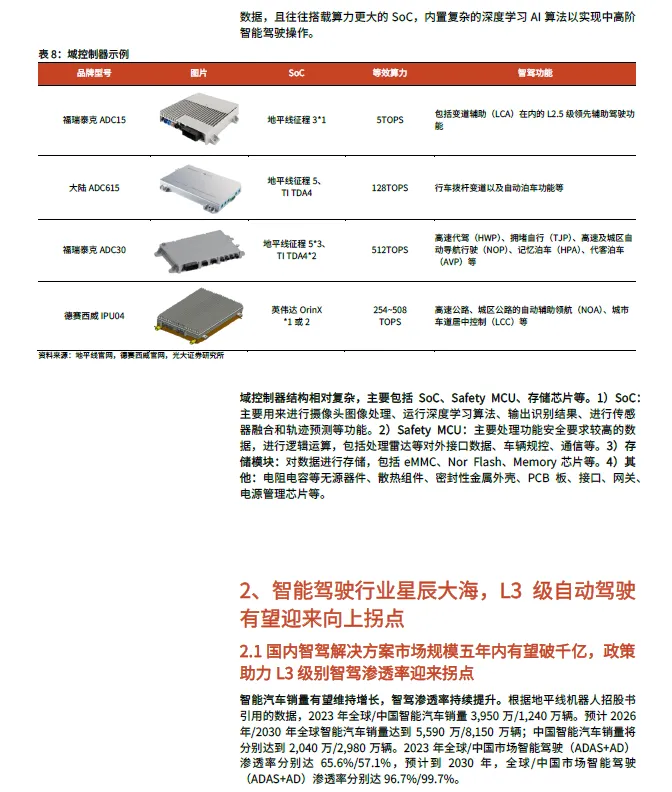

The automotive architecture is shifting from centralized to distributed, with SoC chips becoming core components of smart driving: As smart driving continues to advance, the traditional distributed electronic and electrical architecture of vehicles is gradually evolving towards a centralized architecture due to its inability to meet OTA upgrade demands, low computational efficiency, and insufficient information integration. Domain controllers are the core of the centralized electronic and electrical architecture, with two main implementation paths represented by Bosch and Tesla. In the era of domain controllers, high-performance, high-integration heterogeneous SoC chips will become core components of smart driving. In addition to domain controllers, smart driving SoC chips are also core components of front-view integrated machines.

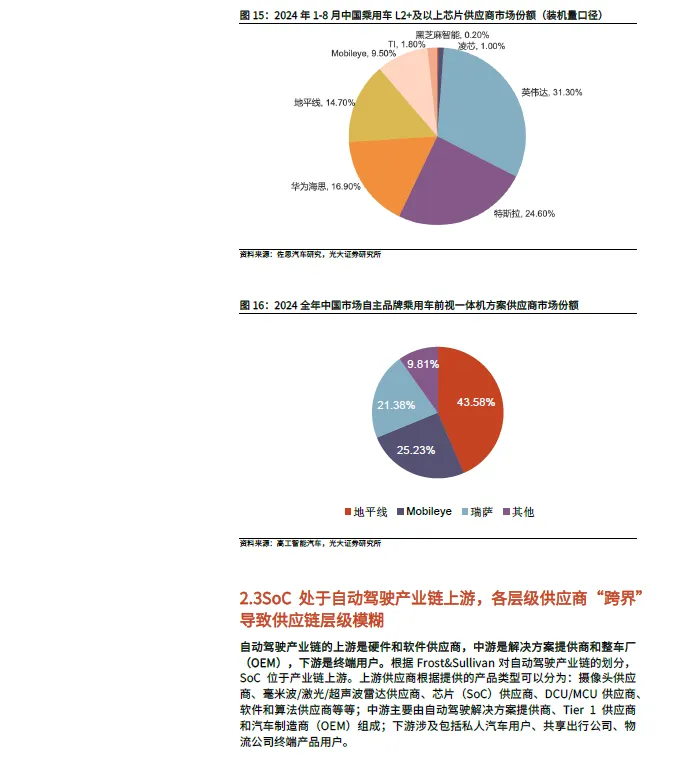

The domestic smart driving solution market is expected to exceed 400 billion RMB by 2030. Currently, in the high-end/mid-low-end SoC market, Nvidia and Horizon hold major shares. According to data from Zhaoshang Consulting cited in Horizon Robotics’ prospectus, global and Chinese smart vehicle sales are expected to reach 81.5 million and 29.8 million units, respectively, by 2030; the penetration rates of smart driving (ADAS+AD) are expected to reach 96.7% and 99.7% globally and in China, respectively. The global and Chinese smart driving (ADAS+AD) solutions market is expected to exceed 1 trillion and 400 billion RMB by 2030. In 2025, Wuhan and Beijing will successively introduce laws and regulations clarifying the rights and responsibilities of L3 and autonomous driving, coupled with the continuous penetration of L2+ smart driving, we believe that the penetration rate of L2+ and above smart driving is expected to reach an upward turning point. In terms of market share, Nvidia is expected to hold a major share (over 30%) of the high-end SoC market in 2024, while Horizon is expected to lead the mid-low-end market (over 40%), with shares expected to continue to expand.

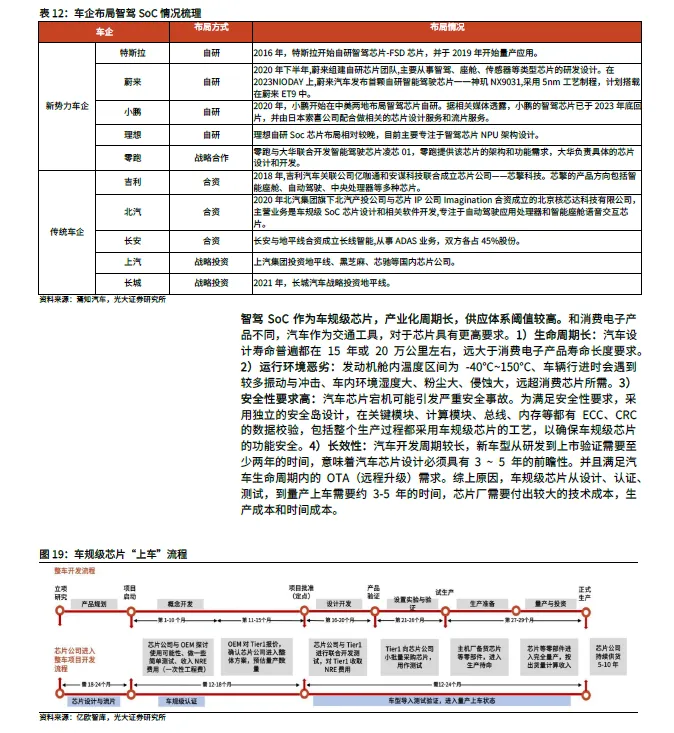

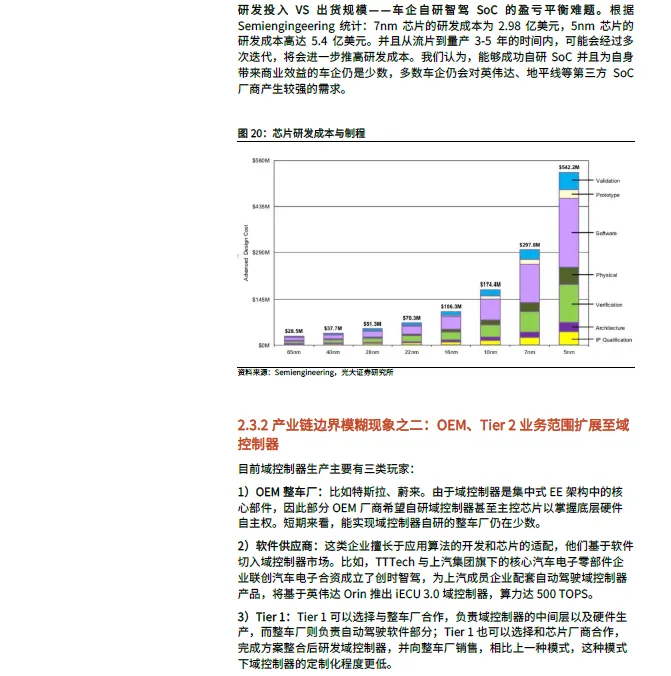

Automakers face challenges in achieving profitability while entering the SoC market, with third-party SoC manufacturers still playing an important role. Currently, mainstream automakers are actively entering the automotive SoC chip market, with strategies generally falling into four categories: self-research, joint ventures, strategic investments, and strategic partnerships. The development of automotive-grade chips, from design, certification, testing, to mass production, takes about 3-5 years, coupled with the significant investment required for advanced process chips, we believe that only a few automakers will successfully self-develop SoCs that bring commercial benefits, while most automakers will still have strong demand for third-party SoC manufacturers like Nvidia and Horizon.

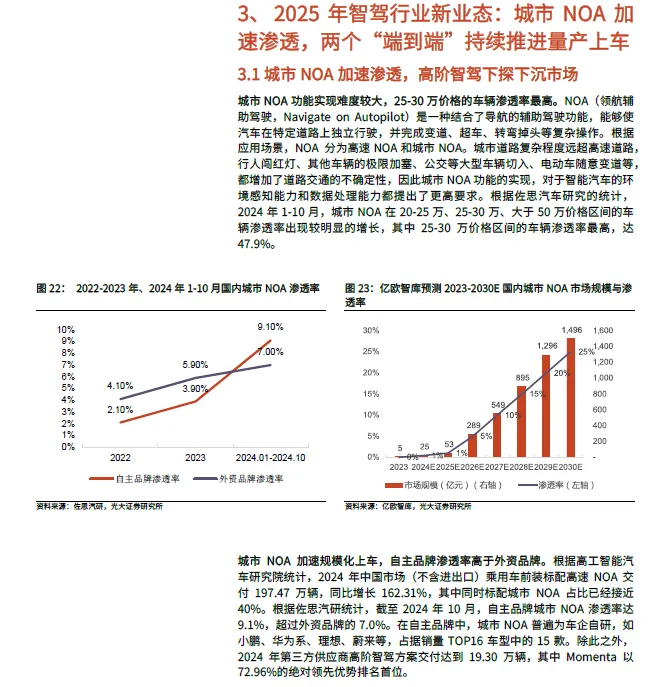

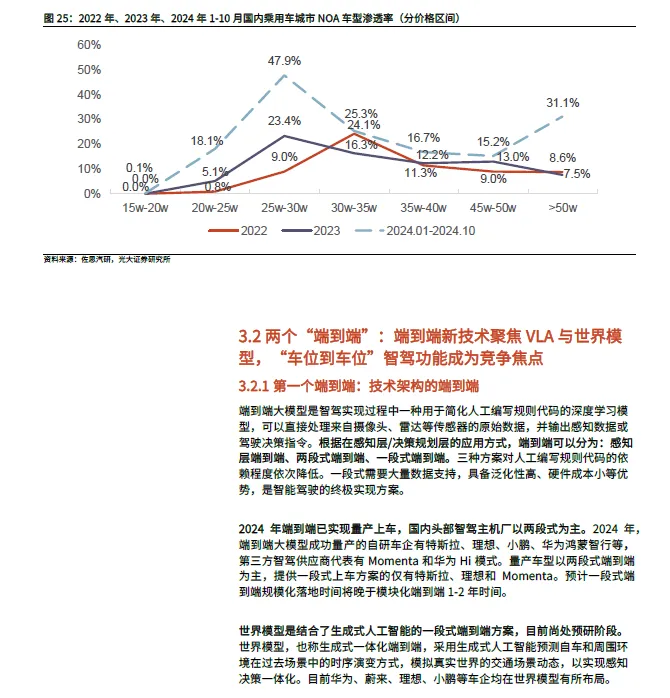

In 2025, urban NOA will accelerate its penetration into lower-tier markets, with two “end-to-end” solutions continuously advancing towards mass production, leading to a sustained increase in demand for cost-effective mid-to-high-performance chips. In 2024, urban NOA will enter the price range of 150,000 to 250,000 RMB, and in 2025, BYD will promote “smart driving equality,” which is expected to drive high-end smart driving down to models priced around 100,000 RMB. We believe that the penetration rate of urban NOA in models priced below 150,000 RMB will rapidly increase in 2025, leading to a sustained increase in demand for mid-to-high-performance chips. Additionally, from a technical perspective, the focus of new end-to-end technologies in 2025 will be on VLA and world models, with “parking space to parking space” smart driving functions becoming a competitive focus for major automakers, raising higher requirements for chip performance, solution provider capabilities, and OEM self-development capabilities.

Report Framework:

1) Review the technical details of smart driving SoC chips and the evolution of automotive electronic and electrical architectures, concluding that in the current domain centralized electronic and electrical architecture (EEA), SoCs are core components of smart driving. In the first part, we also review the actual application scenarios of smart driving SoCs: domain controllers and integrated machines.

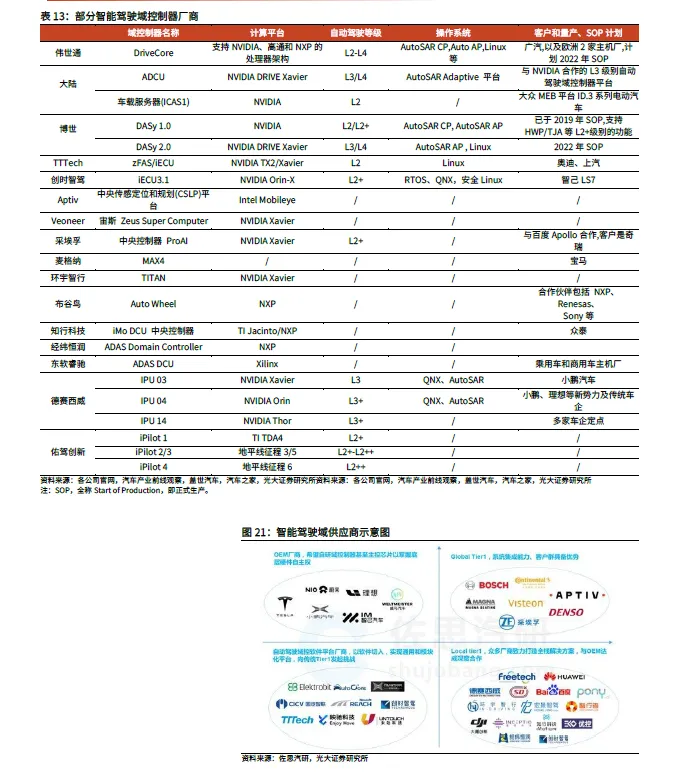

2) Provide a detailed overview of the scale and market share of the smart driving SoC industry, and analyze the changes in the automotive chip industry chain, specifically reflecting the involvement of OEMs in SoC development and the expansion of OEMs and some SoC suppliers into domain controllers.

3) The market is particularly concerned about the impact of OEM self-developed SoCs on third-party SoC manufacturers. In this article, we discuss the balance challenges of cost and shipment volume faced by OEM self-developed SoCs, concluding that only a few automakers will successfully self-develop SoCs that bring commercial benefits, while most automakers will still have strong demand for third-party SoC manufacturers like Nvidia and Horizon.

4) Provide a detailed overview of the trends in the smart driving industry in 2025: accelerated penetration of urban NOA and two “end-to-end” solutions moving towards mass production. At the same time, we analyze the competitiveness of smart driving SoCs in conjunction with new industry dynamics, specifically reflected in multiple dimensions such as computational power, continuity of technology routes, completeness of product matrices, software and hardware ecosystems, and solution provider ecosystems.