Software-Defined Vehicles(SDV) technology is one of the most important topics in the automotive industry. Software defines the capabilities and detailed functions of all Electronic Control Units(ECU), including those that control mechanical systems. Over the past decade, theseECUs have significantly increased in complexity and code volume, and this trend will continue. InSDV, all software-related functions are connected to cloud computing systems.

Compared to traditional vehicles,SDV requires different organizational approaches, technologies, strategies, development, testing, and especially software management throughout the entire lifecycle. Advanced Driver Assistance Systems(ADAS) and Autonomous Vehicles(AV) software have increased the complexity and demands ofSDV. Artificial Intelligence(AI) technologies are also being explored and gradually applied inSDV, although the outcomes of this development are still unclear, it is expected that its impact will become quite significant in the next decade.

Challenges Facing Automotive Software

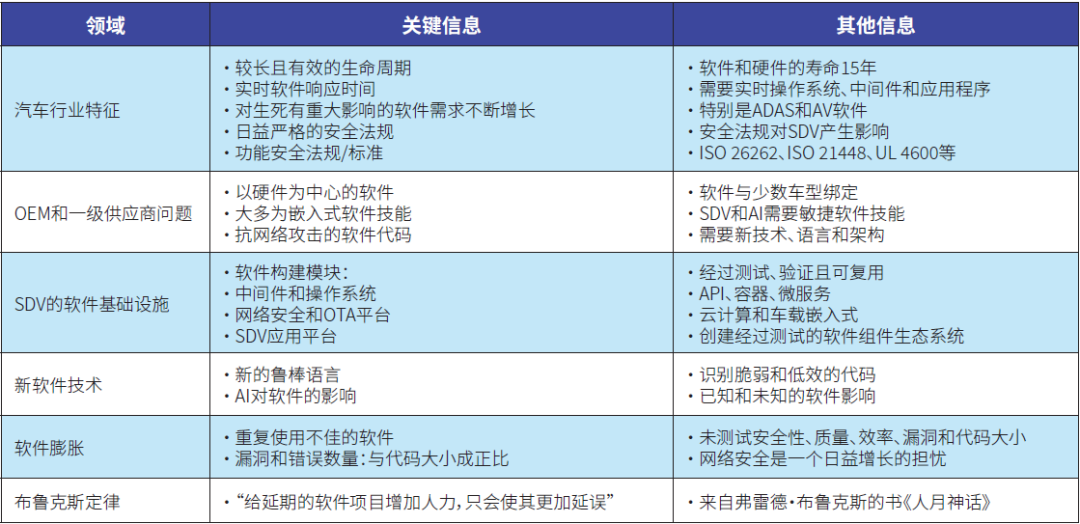

The characteristics of automotive electronics make the rapidly growing software portfolio transitioning toSDV technology more complex in terms of development, maintenance, and management. Table1 summarizes these characteristics and their impact on software platforms centered aroundSDV. These characteristics increase the complexity and effort required to enter theSDV era.

Table1:Challenges FacingSDV (Source:Egil Juliussen)

The lifecycle of automotive software is the longest in any industry, especially for mass-produced products with annual sales reaching tens of millions. Over the past decade, the complexity and scale of automotive software have dramatically increased. The total code volume of software platforms in some existing models has exceeded 100 million lines and may double in the next decade. So, the question arises, how will theSDV platform affect the total code size?

ManyECUs perform real-time operations, which means that there are specific time constraints for completing software tasks; otherwise, the software controlling the vehicle’s operating components(such as the engine, brakes, and steering) may fail, jeopardizing safety. ADAS andAV functions are also part of real-time software functionalities, and their importance is increasing. Since many real-time software functions involve life-and-death operations, theSDV software platform must comply with existing and emerging safety regulations and related standards.

Original Equipment Manufacturers(OEM), Tier 1 suppliers, and the software supply chain’sSDV software skills are an ongoing issue. In the next five to ten years, automotive software practitioners will be busy updating legacy software platforms that will be reused and improved in internal combustion engine(ICE) vehicles. OEM manufacturers and their software supply chains need to enhance theirSDV software skills during the transition from legacy software platforms.

There is an urgent need to develop software infrastructure forSDV platforms and software building blocks. They must be tested, verified, and reusable for about ten years, after which they will also need support and upgrades for approximately15 years.

New software technologies are constantly emerging, and more technologies are needed to identify vulnerable and inefficient code. AI technologies are rising in the automotive software field and will become a major factor inSDV software.

“Software bloat” is an important issue that has not received enough attention. Any software program consists of many components, including operating systems, middleware, software libraries, and specific applications. Due to the tight development cycles of these programs, most programs will use various third-party software components.

If not thoroughly checked and tested, these components will significantly increase the size of the program code. The number of software errors and vulnerabilities is always proportional to the size of the code. Fred Brooks(Fred Brooks) made a widely known observation in his classic work published in 1975, “The Mythical Man-Month”(The Mythical Man-Month)—”Brooks’ Law”: “Adding manpower to a late software project makes it later.”

For more insights into the issues related to software bloat, refer to the article “Why Bloat Is Still Software’s Biggest Vulnerability” for profound insights.

Overview of SDV Technology

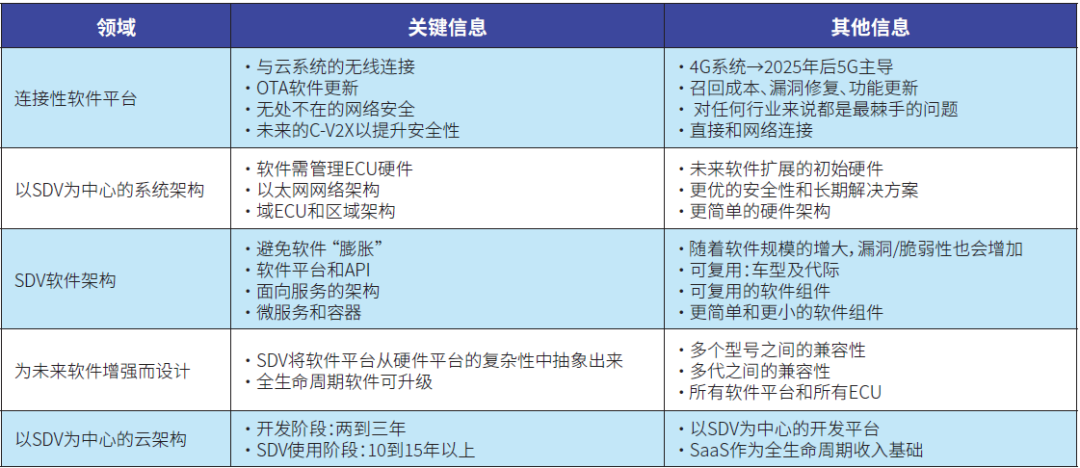

The term “SDV” has multiple usages, which can cause some confusion. Table2 summarizes the current meanings ofSDV technology.

Table2:Requirements forSDV (Source:Egil Juliussen)

Connectivity based onSDV is a core requirement for most software functions(includingOTA and cybersecurity). This connectivity can reduce the costs of software recalls, bug fixes, and feature updates.

TraditionalECUs are designed with a hardware-centric approach with added software. However,SDV requires a software-centric system architecture where the software requirements dictate the capabilities of the hardware. The initial hardware design should have the capability to support future software expansions. Upgradeable hardware will be an important direction for the future.

The software architecture ofSDV is crucial as it needs to be applicable to various vehicle models and generations. The design philosophy ofSDV includes considerations for future software enhancements. One key feature is to abstract the complexity of the software platform from the hardware platform. This means that theSDV software platform only needs to make minimal changes to run on various hardware platforms.

Service-oriented architecture, microservices, and container technologies have been widely adopted among large cloud service providers and also have advantages inSDV platforms. Microservices and containers are designed to be simpler, smaller, and more secure than traditional software components. Amazon Web Services(AWS) has been a leader in automotive software development in this regard.

The third key technology is the cloud architecture centered aroundSDV, which includes two important phases: during software development and throughout the vehicle’s entire lifecycle. The lifespan may become a key factor in the value proposition ofSDV software, as over time, software can shift from being a cost center to a profit center, as revenue generated from Software as a Service(SaaS) will eventually exceed the costs of software development.

Challenges Faced by Traditional OEM Manufacturers

Traditional OEM manufacturers selling ICE vehicles equipped with hardware-centric electronic systems face significant challenges in converting theirECUs toSDV architectures. TheseOEM manufacturers rely on sales of existing vehicles equipped with traditional electronics to fund the development ofSDV software. This means that software development must cover both the newSDV platform and updates to existing traditional software platforms.

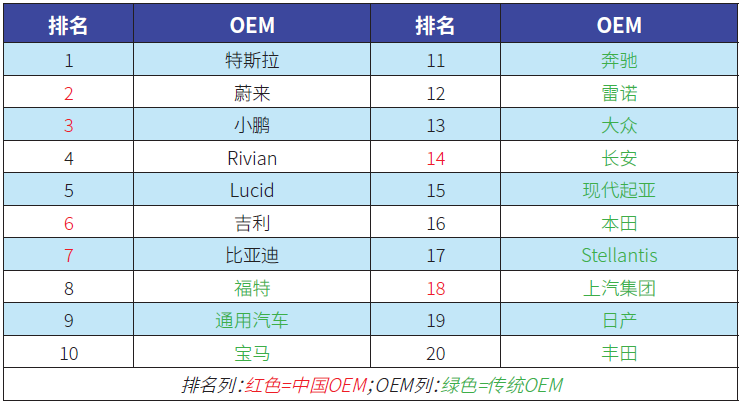

Battery Electric Vehicle(BEV) startups do not have the requirements of traditional software and can focus on developingSDV software. This means that in terms of expertise inSDV, BEV startups are far ahead of traditionalOEM manufacturers. Table3 illustrates this trend, based on the Gartner Digital Automotive Manufacturer Index, which ranks the top 20 manufacturers according to their ability to leverage digital technologies.SDV is a significant component of automotive digital technology.

Table3:Gartner 2024 Digital Automotive Manufacturer Index(Source:Gartner)

In the table, Chinese automotive manufacturers are marked in red in the ranking column, while traditional automotive manufacturers are marked in green in the OEM column. Notably, four of the top seven automotive manufacturers are Chinese automotive manufacturers. Furthermore, traditional automotive manufacturers lag behind BEV startups in terms ofSDV and other digital technologies.

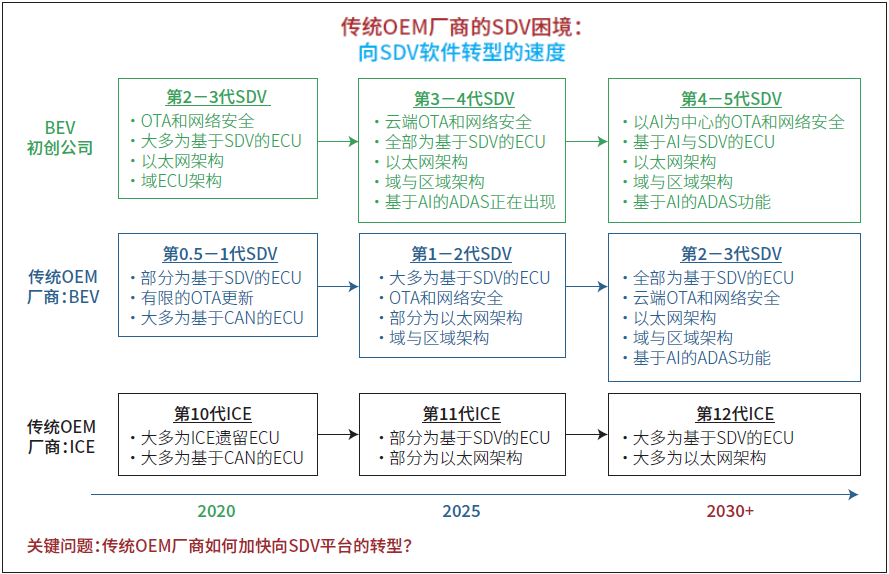

Figure1 further illustrates the dilemmas faced by traditional OEM manufacturers in transitioning toSDV platforms. The timeline of the conceptual diagram extends from2020 to2030 and beyond, providing an assessment of current and futureSDV trends.

Figure1: How Traditional OEM Manufacturers Accelerate the Transition toSDV Platforms? (Source:Egil Juliussen)

The three green boxes illustrate the progress of BEV startups in software iterations ofSDV. The generational divisions ofSDV vary among OEMs. The three blue boxes estimate the progress of traditional OEM manufacturers inSDV on BEVs, with significant differences among traditional OEM manufacturers. The black box illustrates the progress of traditional OEM manufacturers inSDV on ICE vehicles.

BEV startups are leading in deployingSDV systems compared to traditional OEM manufacturers and are expected to maintain this lead over the next decade. Numerous collaborations and joint ventures between BEV startups and traditional OEM manufacturers demonstrate this. If BEV valuations decline, similar collaborations and acquisition activities may increase.

Progress inSDV among traditional OEM manufacturers varies by company(as shown in the left blue box of the figure, from0.5 to1 generation). Several major traditional OEM manufacturers have limitedSDV functionalities, such as OTA updates, in their firstSDV iterations (i.e.,0.5 generation). While the next generation of products will see improvements, BEV startups are continuously optimizing theirSDV functionalities. Currently, AI-based functionalities have become a key development focus for many BEV startups.

It is more challenging for traditional OEM manufacturers to establishSDV work on ICE vehicles. Due to legal requirements in many regions, someSDV functionalities are gradually being implemented through core features such as OTA updates and cybersecurity.

The key question is whether and how traditional OEM manufacturers can accelerate the transition toSDV platforms. SomeSDV support activities discussed in the next section may help, but only time will tell.

SDV Support Activities

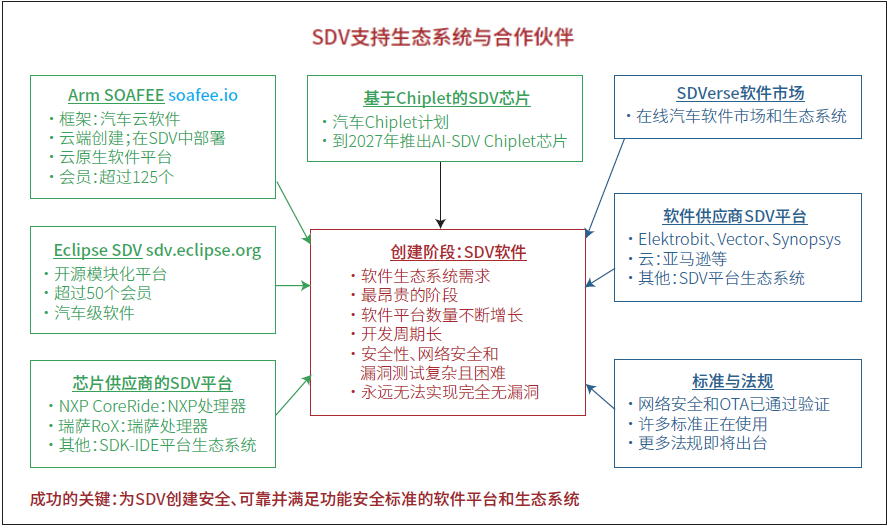

As theSDV platform becomes the most important software topic in the automotive industry, many organizations and companies are conducting an increasing number of activities focused on the software creation phase or development aspects. Figure2 illustrates some of these efforts, but many more are underway.

Figure2: The key to success is building a secure and reliable software platform and ecosystem forSDV. (Source:Egil Juliussen)

The two green boxes in the upper left represent two organizations focused onSDV development: Arm’s Embedded Edge Extensible Open Architecture(SOAFEE) andEclipse SDV. The green box in the top center represents a new organization developing chiplet technology to drive the creation of higher quality, software-centric hardware platforms forSDV. The green box on the bottom left contains chip companies withSDV platforms aimed at encouraging the use of their microprocessors in hardware systems. The two blue boxes in the upper right represent activities developing the software supply chain forSDV.

Arm’sSOAFEE is one of the early organizations dedicated toSDV software development, providing a cloud-native development framework for creating deployableSDV software. SOAFEE now has over128 members. Although General Motors is the only OEM member, most Tier 1 suppliers have joined.

The Eclipse Foundation has added an open-source platform forSDV software development. Eclipse SDV has over50 members, including key Tier 1 suppliers such as Bosch, Continental, Denso, Valeo, and ZF. Major OEM members include BMW, General Motors, and Mercedes-Benz.

Several chip suppliers are also providing software development platforms forSDV to promote the application of their chip series. All major automotive chip suppliers will launch development platforms focused onSDV. NXP will showcase its CoreRide platform at the Munich Electronics Fair(electronica) in November 2024.

A noteworthy new project is the automotive chiplet program led byimec, which will be announced in October 2024. The focus is on creating a chiplet-based system-on-chip(SoC) development ecosystem to accelerate the development speed of the hardware required forSDV platforms.

SDVerse: The SDV Market

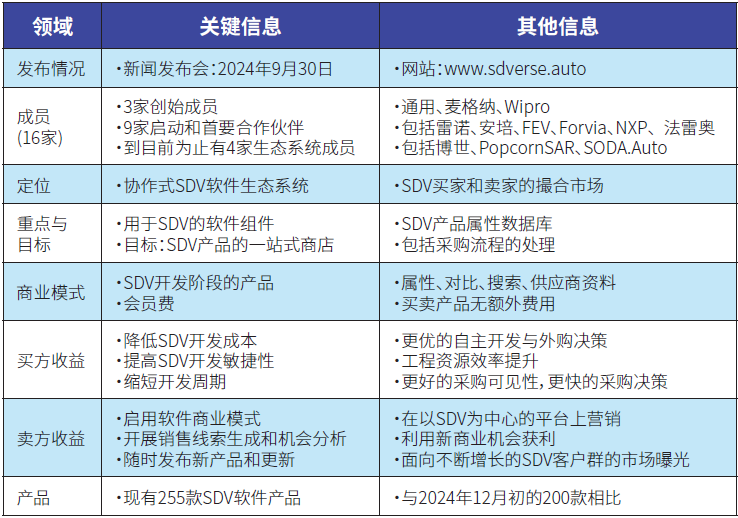

The online automotive software marketSDVerse held its first press conference on September 30, 2024, in Detroit.

Table4 summarizes the current status information ofSDVerse, positioning itself as a marketplace for matchingSDV buyers and sellers. The market currently has16 members, with General Motors, Magna, and Wipro as founding members.

Table4:SDVerse Online Automotive Software Market(Source:Egil Juliussen)

SDVerse focuses on a database ofSDV products and their specifications, aiming to become a one-stop shop for allSDV products. The core of its business model is a membership fee, allowing members to access theSDV product database without additional fees for purchasing or selling products themselves.

ForSDV buyers, the advantages include reducingSDV development costs through more informed make-or-buy decisions, shortening development cycles, and improving software engineering efficiency.

ForSDV sellers, they can gain visibility to potential customers and opportunity analysis, allowing sellers to update their product listings in theSDVerse database to announce updates to existing products or new product releases.

Ultimately, theSDVerse e-commerce platform may resemble Amazon for the automotive software industry. However, it is currently difficult to estimate the specific value ofSDVerse based on publicly available information, thus relying on feedback from companies that have usedSDVerse. During CES 2025,SDVerse held a conference and presented relevant information. Based on this feedback, theSDV industry is expected to benefit from the services provided bySDVerse, and the market’s prospects for success are promising.

Future success can be measured by evaluating two data points: the number of members and the number of software products for sale. Currently, the number of members is low, with only16 members, but it will take time for interested parties to plan funding to join the new organization. By the end of January 2025, the number of software products reached255, an increase from200 at the beginning of December 2024.

The rapid growth of membership and the expansion of the database of software products for sale will be key indicators ofSDVerse‘s progress.

The automotive industry is on the path to benefiting fromSDV, which will benefit customers, OEM manufacturers, and suppliers throughout the vehicle lifecycle. However, the development ofSDV is complex, time-consuming, and costly, requiring substantial resources. The automotive industry must accumulate more expertise around these resources and equip a larger workforce.

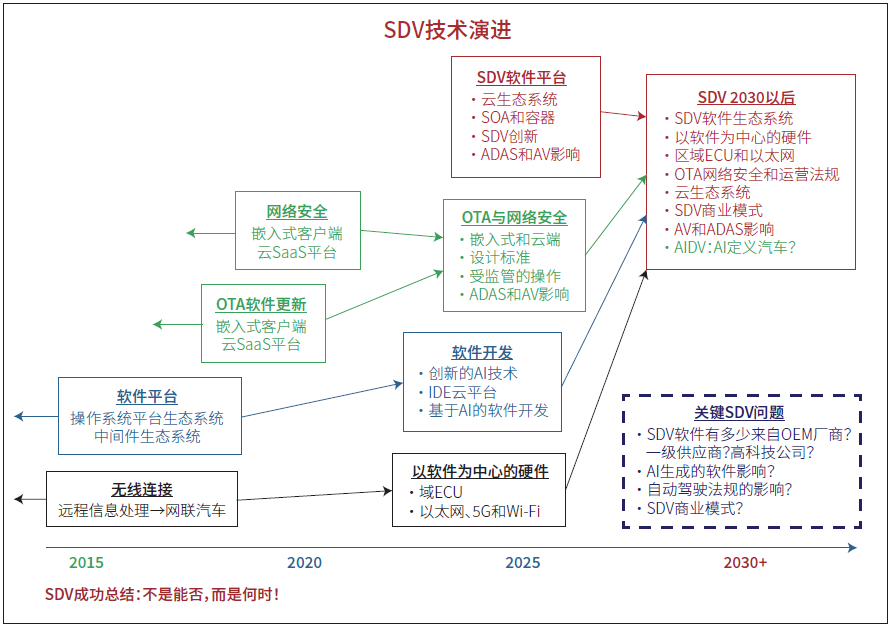

Figure3 outlines the evolution ofSDV, from software platforms and connected vehicles toOTA updates and cybersecurity, to the increasingly growing software-centric platforms. The key technologies ofSDV have evolved from four core functionalities: telematics(i.e., connected vehicles), an increasing number of available software platforms,OTA software updates, and cloud-connected in-vehicle cybersecurity platforms. These technologies are comprehensively improvingSDV and will replace all traditional hardware and software in the next decade.

Figure3: Summary ofSDV Success—Not “Whether,” but “When”(Source:Egil Juliussen)

It is expected that by2030, allOEM manufacturers will have adoptedSDV, and its functionalities will continue to enhance. A key question is howAI will influenceSDV. Some BEV startups have already defined AI-driven vehicles as the next generation ofSDV. While this possibility is high, the specific timing remains uncertain.

The ultimate conclusion is that the success ofSDV is not a question of “Whether,” but rather “When.”

(Edited by: Franklin)