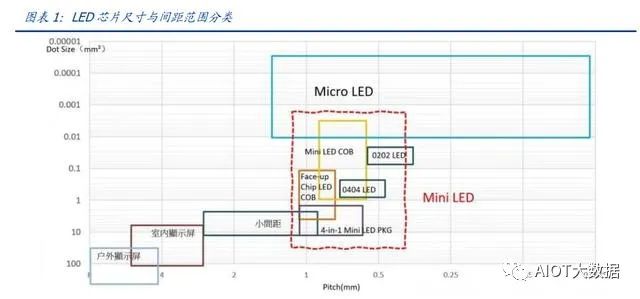

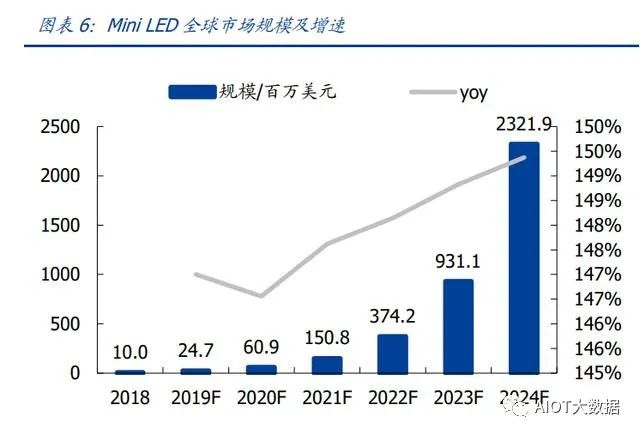

1. What Is Mini LED Technology?Generally speaking, Mini LED refers to LED chips that are 100 to 300 micrometers in size, with a chip spacing of 0.1 to 1mm, and are packaged in forms such as SMD, COB, or IMD. These micro LED device modules are often used in RGB displays or LCD backlighting.The quality factors of a display include resolution (number of pixels), PPI (pixels per inch), viewing distance, etc. Generally, LCD and LED screens are used for distances over 3 meters, while OLED, Mini LED displays (2-3 meters), and Micro OLED (within 1 meter) are used for closer viewing. Furthermore, Mini LED technology can also enhance the display effect in LCD backlight modules. Therefore, Mini LED technology can be directly used for RGB displays as well as for LCD backlight modules.Typically, LED RGB displays include LED screens, small spacing displays, Mini LED, and Micro LED.Small spacing: over 300 micrometers, with a chip spacing of 2.5 to 1mm, using traditional SMD packaging methods.Mini LED: 100 to 300 micrometers, with a chip spacing of 0.1 to 1mm, using SMD, COB, or IMD packaging. MicroLED: under 100 micrometers, with a chip spacing of 0.001 to 0.1mm, using mass transfer. Mini LED backlight + LCD and Mini LED displays are driven by two innovative paths. From the perspective of original components, the application of Mini LED is mainly divided into two schemes: using Mini LED chips + LCD for backlighting and directly using Mini RGB displays as self-luminous solutions. Currently, the Mini LED backlight scheme has entered an explosive growth period, with brands such as Apple and Samsung already launching related products; Mini RGB direct displays focus on commercial display market demands, showing advantages in commercial displays, decorative lighting for electronic products, tail lights, or ambient lighting. Since both schemes share similarities in industrial rules and technical principles, they can share some equipment, leading most companies to pursue both directions simultaneously to enjoy economies of scale.2. Mini LED Backlight: An Innovative Direction for LCD Technology with Vast Market PotentialMini LED backlight is an important innovative direction for LCD display technology. Compared to LCD, OLED is a substitute innovation in display technology, while Mini LED is an upgrade innovation for LCD, aimed at competing with OLED. Compared to the advantages of OLED such as contrast and color, Mini LED backlight products perform comparably, and they have significant advantages such as lower capital expenditures (cost-effective), flexible specifications (broad applications), adaptability to the development needs of the panel/LED optoelectronic industry chain (supply-driven), and long service life (especially suitable for TV scenarios).2.1. Mini LED Backlight Opens Commercialization Era, Market Growth Elasticity ExpectedThe Mini LED backlight market is officially starting to scale up, with commercialization of TV and IT applications expected to accelerate. According to Arizton’s forecast, the global Mini LED market size is expected to grow from $150 million in 2021 to $2.32 billion by 2024, with an annual growth rate exceeding 140%. Based on our calculations and industry tracking, this data significantly underestimates the market’s growth elasticity. With mainstream brands like Samsung and Apple introducing Mini LED backlights, a wave of innovation in the end-user market is expected. According to TrendForce, TVs and tablets are the first to commercialize; smartphones, automobiles, and VR are likely to enter the commercialization era in 2022-2023.

Mini LED backlight + LCD and Mini LED displays are driven by two innovative paths. From the perspective of original components, the application of Mini LED is mainly divided into two schemes: using Mini LED chips + LCD for backlighting and directly using Mini RGB displays as self-luminous solutions. Currently, the Mini LED backlight scheme has entered an explosive growth period, with brands such as Apple and Samsung already launching related products; Mini RGB direct displays focus on commercial display market demands, showing advantages in commercial displays, decorative lighting for electronic products, tail lights, or ambient lighting. Since both schemes share similarities in industrial rules and technical principles, they can share some equipment, leading most companies to pursue both directions simultaneously to enjoy economies of scale.2. Mini LED Backlight: An Innovative Direction for LCD Technology with Vast Market PotentialMini LED backlight is an important innovative direction for LCD display technology. Compared to LCD, OLED is a substitute innovation in display technology, while Mini LED is an upgrade innovation for LCD, aimed at competing with OLED. Compared to the advantages of OLED such as contrast and color, Mini LED backlight products perform comparably, and they have significant advantages such as lower capital expenditures (cost-effective), flexible specifications (broad applications), adaptability to the development needs of the panel/LED optoelectronic industry chain (supply-driven), and long service life (especially suitable for TV scenarios).2.1. Mini LED Backlight Opens Commercialization Era, Market Growth Elasticity ExpectedThe Mini LED backlight market is officially starting to scale up, with commercialization of TV and IT applications expected to accelerate. According to Arizton’s forecast, the global Mini LED market size is expected to grow from $150 million in 2021 to $2.32 billion by 2024, with an annual growth rate exceeding 140%. Based on our calculations and industry tracking, this data significantly underestimates the market’s growth elasticity. With mainstream brands like Samsung and Apple introducing Mini LED backlights, a wave of innovation in the end-user market is expected. According to TrendForce, TVs and tablets are the first to commercialize; smartphones, automobiles, and VR are likely to enter the commercialization era in 2022-2023. Apple launched the world’s first tablet product equipped with Mini LED backlighting, the iPad Pro. The pricing strategy for Apple’s first Mini LED backlight product is expected to drive high sales. The new 12.9-inch iPad Pro features 10,000 Mini LED backlights, with 2,596 zones and a contrast ratio of 1,000,000:1. The new 12.9-inch iPad Pro is equipped with the M1 chip, starting at a price of 8,499 yuan (the iPad Pro 2020 was priced at 7,899 yuan, lacking Mini LED backlight and the M1 chip).Mini LED has dynamic local dimming capabilities, enhancing the realism and vividness of images. The new 12.9-inch iPad Pro’s Liquid Retina XDR display adopts Mini LED technology. Over 10,000 Mini LEDs are divided into more than 2,500 local dimming zones, allowing for precise adjustment of the brightness of each dimming zone based on the content displayed on the screen, achieving a contrast ratio of 1,000,000:1, fully showcasing rich details and HDR content.The iPad Pro display features high contrast, high brightness, wide color gamut, and True Tone display advantages. Mini LED gives the Liquid Retina XDR display an extreme dynamic range, with a contrast ratio of up to 1,000,000:1, significantly enhancing detail perception. Additionally, this iPad display has impressive brightness performance, with a full-screen brightness of 1,000 nits and a peak brightness of up to 1,600 nits, along with advanced display technologies such as P3 wide color gamut, True Tone display, and ProMotion adaptive refresh rate.Apple leads the trend and accelerates the introduction of Mini LED in laptops and tablets. According to Digitimes, Apple will further release Mini LED-related products. Before Apple’s spring conference, Mini LED laptops and tablets were only released by MSI and Huashuo in 2020. Apple’s significant influence in terminal products is expected to create a demonstration effect, accelerating the adoption of Mini LED in laptop and tablet products. Furthermore, Apple’s strict requirements for its supply chain may cultivate stringent technical requirements for supply chain companies, promoting the development of the Mini LED industry.Samsung’s QLED technology has reached a new level, refreshing the TV experience. At CES 2021, Samsung launched the Neo QLED quantum television. This new product uses quantum Mini LED technology, eliminating lens scattering and packaging forms, with a size only 1/40 of traditional LEDs. Additionally, the use of ultra-thin micro layers, combined with Samsung’s self-developed AI quantum computing technology, allows for precise control of tightly arranged LED chips, presenting fine images and avoiding halo effects.

Apple launched the world’s first tablet product equipped with Mini LED backlighting, the iPad Pro. The pricing strategy for Apple’s first Mini LED backlight product is expected to drive high sales. The new 12.9-inch iPad Pro features 10,000 Mini LED backlights, with 2,596 zones and a contrast ratio of 1,000,000:1. The new 12.9-inch iPad Pro is equipped with the M1 chip, starting at a price of 8,499 yuan (the iPad Pro 2020 was priced at 7,899 yuan, lacking Mini LED backlight and the M1 chip).Mini LED has dynamic local dimming capabilities, enhancing the realism and vividness of images. The new 12.9-inch iPad Pro’s Liquid Retina XDR display adopts Mini LED technology. Over 10,000 Mini LEDs are divided into more than 2,500 local dimming zones, allowing for precise adjustment of the brightness of each dimming zone based on the content displayed on the screen, achieving a contrast ratio of 1,000,000:1, fully showcasing rich details and HDR content.The iPad Pro display features high contrast, high brightness, wide color gamut, and True Tone display advantages. Mini LED gives the Liquid Retina XDR display an extreme dynamic range, with a contrast ratio of up to 1,000,000:1, significantly enhancing detail perception. Additionally, this iPad display has impressive brightness performance, with a full-screen brightness of 1,000 nits and a peak brightness of up to 1,600 nits, along with advanced display technologies such as P3 wide color gamut, True Tone display, and ProMotion adaptive refresh rate.Apple leads the trend and accelerates the introduction of Mini LED in laptops and tablets. According to Digitimes, Apple will further release Mini LED-related products. Before Apple’s spring conference, Mini LED laptops and tablets were only released by MSI and Huashuo in 2020. Apple’s significant influence in terminal products is expected to create a demonstration effect, accelerating the adoption of Mini LED in laptop and tablet products. Furthermore, Apple’s strict requirements for its supply chain may cultivate stringent technical requirements for supply chain companies, promoting the development of the Mini LED industry.Samsung’s QLED technology has reached a new level, refreshing the TV experience. At CES 2021, Samsung launched the Neo QLED quantum television. This new product uses quantum Mini LED technology, eliminating lens scattering and packaging forms, with a size only 1/40 of traditional LEDs. Additionally, the use of ultra-thin micro layers, combined with Samsung’s self-developed AI quantum computing technology, allows for precise control of tightly arranged LED chips, presenting fine images and avoiding halo effects. Numerous well-known brands released their first Mini LED televisions in 2021, and the leading demonstration effect is expected to accelerate the penetration of Mini LED. Brands like Samsung, LG, Skyworth, and TCL have all released their first Mini LED televisions, accelerating terminal applications. Under the demonstration effect of leading manufacturers, more companies are expected to introduce Mini LED backlight products.2021 is expected to be the year of large-scale Mini LED TV shipments, with expected shipments surpassing 4 million units. According to AVC Revo’s predictions, 2021 Mini LED TVs will become the top-selling new display technology televisions. In 2018-2019, Mini LED backlight TVs were only in the thousands, far less than the million-level shipments of OLED TVs; however, in 2021, shipments are expected to rapidly increase to about 60% of OLED shipments. TrendForce predicts that Mini LED backlight TVs will reach 4.4 million units in 2021, accounting for about 2% of the overall TV market. Omdia predicts that global Mini LED backlight TV product sales will increase to 52.8 million units by 2025, with a CAGR of 53.73% from 2019 to 2025.The increase in smart car penetration will help the Mini LED display scale up. As the coverage of smart connected cars gradually increases, the growth rate of the in-car display market is promising. Mini LED technology can meet the demands of car manufacturers for high contrast, high brightness, durability, and adaptability to complex lighting environments inside vehicles, making its future development prospects broad.BOE’s car-mounted BD Cell display and car-mounted Mini LED displays are positioned for high-end automotive displays, applying flexible displays in automotive dashboards, in-car displays, tail lights, and other areas. In 2020, BOE’s car-mounted display shipment area has jumped to second in the world, and its market share for car-mounted display panels over 8 inches has risen to first in the world. The trend of larger, personalized, and ultra-high-definition in-car displays is gradually becoming prominent, and BOE’s smart cockpit solutions will integrate functions such as smart navigation, rearview images, in-car control, and entertainment information.

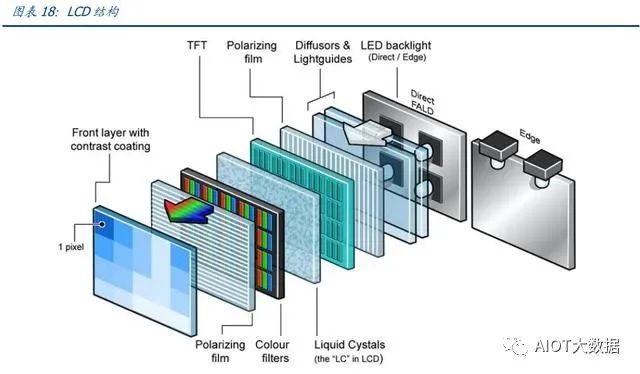

Numerous well-known brands released their first Mini LED televisions in 2021, and the leading demonstration effect is expected to accelerate the penetration of Mini LED. Brands like Samsung, LG, Skyworth, and TCL have all released their first Mini LED televisions, accelerating terminal applications. Under the demonstration effect of leading manufacturers, more companies are expected to introduce Mini LED backlight products.2021 is expected to be the year of large-scale Mini LED TV shipments, with expected shipments surpassing 4 million units. According to AVC Revo’s predictions, 2021 Mini LED TVs will become the top-selling new display technology televisions. In 2018-2019, Mini LED backlight TVs were only in the thousands, far less than the million-level shipments of OLED TVs; however, in 2021, shipments are expected to rapidly increase to about 60% of OLED shipments. TrendForce predicts that Mini LED backlight TVs will reach 4.4 million units in 2021, accounting for about 2% of the overall TV market. Omdia predicts that global Mini LED backlight TV product sales will increase to 52.8 million units by 2025, with a CAGR of 53.73% from 2019 to 2025.The increase in smart car penetration will help the Mini LED display scale up. As the coverage of smart connected cars gradually increases, the growth rate of the in-car display market is promising. Mini LED technology can meet the demands of car manufacturers for high contrast, high brightness, durability, and adaptability to complex lighting environments inside vehicles, making its future development prospects broad.BOE’s car-mounted BD Cell display and car-mounted Mini LED displays are positioned for high-end automotive displays, applying flexible displays in automotive dashboards, in-car displays, tail lights, and other areas. In 2020, BOE’s car-mounted display shipment area has jumped to second in the world, and its market share for car-mounted display panels over 8 inches has risen to first in the world. The trend of larger, personalized, and ultra-high-definition in-car displays is gradually becoming prominent, and BOE’s smart cockpit solutions will integrate functions such as smart navigation, rearview images, in-car control, and entertainment information. 2.2. Mini LED Backlight Achieves Local Dimming, An Important Innovative Direction for LCD UpgradingMini LED backlight is currently an important innovative direction for LCD upgrading, achieving local dimming capabilities through smaller backlight LED sizes and point spacing. The backlight source mainly consists of light sources, light guide plates, optical films, and plastic frames. Currently, there are three main types of backlight sources: EL, CCFL, and LED, which can be divided into side-lit and direct-lit (bottom backlight) based on the distribution position of the light source. Mini LED is a new innovative backlight method. Mini LED backlight features fine partitioning, which, combined with local dimming technology, can significantly improve LCD display quality and can compete with OLED in terms of wide color gamut, ultra-high contrast, and high dynamic range display. Additionally, by integrating flip-chip packaging and other technologies, precise control of packaging thickness can be achieved, resulting in smaller OD and broad application prospects for ultra-thin backlights. Most importantly, Mini LED backlight LCD products have a longer service life than OLED, making them more suited for TV scenarios.Mini LED backlight schemes directly affect the imaging quality of LCD displays. LCD screens control each pixel by applying different voltages, causing liquid molecules to produce differences in light transmittance under various current states, thus forming the desired image. The backlight source is a light source located behind the LCD, and its luminous effect will directly impact the visual effect of the display module. LCDs do not emit light themselves; the displayed graphics or characters are a result of their modulation of light.

2.2. Mini LED Backlight Achieves Local Dimming, An Important Innovative Direction for LCD UpgradingMini LED backlight is currently an important innovative direction for LCD upgrading, achieving local dimming capabilities through smaller backlight LED sizes and point spacing. The backlight source mainly consists of light sources, light guide plates, optical films, and plastic frames. Currently, there are three main types of backlight sources: EL, CCFL, and LED, which can be divided into side-lit and direct-lit (bottom backlight) based on the distribution position of the light source. Mini LED is a new innovative backlight method. Mini LED backlight features fine partitioning, which, combined with local dimming technology, can significantly improve LCD display quality and can compete with OLED in terms of wide color gamut, ultra-high contrast, and high dynamic range display. Additionally, by integrating flip-chip packaging and other technologies, precise control of packaging thickness can be achieved, resulting in smaller OD and broad application prospects for ultra-thin backlights. Most importantly, Mini LED backlight LCD products have a longer service life than OLED, making them more suited for TV scenarios.Mini LED backlight schemes directly affect the imaging quality of LCD displays. LCD screens control each pixel by applying different voltages, causing liquid molecules to produce differences in light transmittance under various current states, thus forming the desired image. The backlight source is a light source located behind the LCD, and its luminous effect will directly impact the visual effect of the display module. LCDs do not emit light themselves; the displayed graphics or characters are a result of their modulation of light. Mainstream LCD TVs or displays typically use overall control of the backlight, which cannot achieve partitioned dimming and generally only requires dozens of LED beads. The Mini LED backlight scheme achieves partitioned dimming through thousands of beads, representing an important innovative direction for LCD backlighting. The quality of the backlight source not only directly affects the image quality of the LCD but also the performance of the backlight source itself. Typical backlight sources mainly consist of light sources, light guide plates, optical membranes, and plastic frames. The current mainstream types are EL, CCFL, and LED, which can be divided into side-lit and direct-lit types. AIOT big data suggests that as LCD modules continue to develop towards being brighter, lighter, and thinner, side-lit CCFL backlight sources are becoming mainstream, leading to the emergence of Mini LED backlight methods. The cost of Mini LED backlight modules includes LED, SMT assembly, driving IC, backplane, etc., with most currently using PCB backplanes and passive driving combinations.Currently, AIOT big data believes that the Mini LED backlight TV technology solutions mainly include COB and POB; based on different substrates, they can be divided into PCB substrates and glass substrates. COB, or Chip on Board, means that the LED chip is directly placed on the substrate and then packaged as a whole; POB, or Package on Board, is commonly referred to as the starry sky scheme, where the LED chip is first packaged as a single SMD LED bead and then placed on the substrate.The Mini LED backplane mainly includes three schemes: PCB, glass substrates, and FPC. Research indicates that only about 60% of the light emitted from traditional backlight sources passes through the backlight module into the polarizing film after being reflected and diffused by optical films, leaving only 4% of light after passing through the LC and surface. Therefore, the design of the backlight scheme structure is particularly important. The three mainstream backplane schemes of PCB, glass substrates, and FPC have their respective advantages and disadvantages, which will also affect the technological design of the backlight scheme. The choice of substrate material directly determines the effectiveness of the Mini LED backlight scheme.The basic PCB backplane bears the functions of driving IC and wiring. After completing the circuit board manufacturing process, the required driving IC is placed on the circuit board to complete the backplane driving process. Currently, there are two connection methods between PCB backplanes and driving ICs: the first is a passive driving method where each pixel connects to its respective integrated driving IC on the back of the backplane; the second is an active driving method where each pixel has its own driving IC nearby.

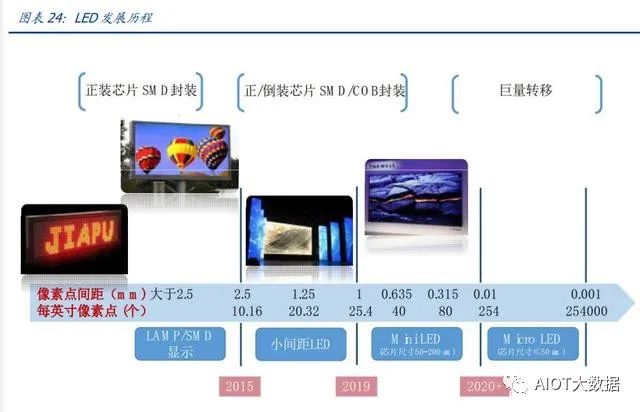

Mainstream LCD TVs or displays typically use overall control of the backlight, which cannot achieve partitioned dimming and generally only requires dozens of LED beads. The Mini LED backlight scheme achieves partitioned dimming through thousands of beads, representing an important innovative direction for LCD backlighting. The quality of the backlight source not only directly affects the image quality of the LCD but also the performance of the backlight source itself. Typical backlight sources mainly consist of light sources, light guide plates, optical membranes, and plastic frames. The current mainstream types are EL, CCFL, and LED, which can be divided into side-lit and direct-lit types. AIOT big data suggests that as LCD modules continue to develop towards being brighter, lighter, and thinner, side-lit CCFL backlight sources are becoming mainstream, leading to the emergence of Mini LED backlight methods. The cost of Mini LED backlight modules includes LED, SMT assembly, driving IC, backplane, etc., with most currently using PCB backplanes and passive driving combinations.Currently, AIOT big data believes that the Mini LED backlight TV technology solutions mainly include COB and POB; based on different substrates, they can be divided into PCB substrates and glass substrates. COB, or Chip on Board, means that the LED chip is directly placed on the substrate and then packaged as a whole; POB, or Package on Board, is commonly referred to as the starry sky scheme, where the LED chip is first packaged as a single SMD LED bead and then placed on the substrate.The Mini LED backplane mainly includes three schemes: PCB, glass substrates, and FPC. Research indicates that only about 60% of the light emitted from traditional backlight sources passes through the backlight module into the polarizing film after being reflected and diffused by optical films, leaving only 4% of light after passing through the LC and surface. Therefore, the design of the backlight scheme structure is particularly important. The three mainstream backplane schemes of PCB, glass substrates, and FPC have their respective advantages and disadvantages, which will also affect the technological design of the backlight scheme. The choice of substrate material directly determines the effectiveness of the Mini LED backlight scheme.The basic PCB backplane bears the functions of driving IC and wiring. After completing the circuit board manufacturing process, the required driving IC is placed on the circuit board to complete the backplane driving process. Currently, there are two connection methods between PCB backplanes and driving ICs: the first is a passive driving method where each pixel connects to its respective integrated driving IC on the back of the backplane; the second is an active driving method where each pixel has its own driving IC nearby. The choice of PCB board material is related to the power of the LED. In the PCB backplane scheme, the heat generated by the LED needs to be assisted by the substrate material on the board for heat dissipation; thus, high thermal conductivity materials can effectively diffuse and cool over large areas, while low thermal conductivity materials cannot dissipate heat effectively, leading to excessively high temperatures on the substrate.The size of the PCB backplane is limited, and currently, it is mainly achieved through splicing to implement backlight technology. During the PCB board manufacturing process, it undergoes numerous reflows, and internal materials release internal stress, causing warping and bending, which becomes more severe as the size of the PCB increases, leading to optical display differences. Therefore, the size of a single PCB board generally does not exceed 24 inches, and large-sized backlights often require multiple PCB boards to be spliced together.Glass backplanes are expected to gradually replace PCB backplanes as the new solution for Mini LED backplanes. As the Mini LED process gradually shrinks, the transfer process will become more challenging. In comparison, glass backplanes have better flatness, do not require splicing, and possess better process precision, high thermal conductivity, and excellent heat dissipation performance, making them a trend to become the new solution for Mini LED backlighting.3. Mini LED Display: Upgrading Requirements for Chip Structure, Packaging, and Other Technologies3.1. Mini LED Display Continues the Small Pitch Technology Route, Ongoing MiniaturizationMini LED direct displays fill the gap between traditional LED displays and Micro LED technology. Since the 1990s, with significant breakthroughs in dynamic display systems and blue light-emitting lamps, LED displays have gradually evolved from monochrome and dual-color to full-color screens.After over a decade of development, LED chip sizes have continuously shrunk, and pixel spacing has also decreased, resulting in higher PPI.In 2010, Leyard launched the first 2.5mm small-pitch LED television, and small-pitch LED displays have rapidly developed since 2013 in specialized display fields such as government and public services.As pixel spacing further shrinks to below 1mm, LED displays are referred to as Mini LED displays. The size of Mini LED is smaller than that of small-pitch LED, with tighter LED chip arrangements and higher PPI, leading to increased difficulty in production, testing, and maintenance technology upgrades.

The choice of PCB board material is related to the power of the LED. In the PCB backplane scheme, the heat generated by the LED needs to be assisted by the substrate material on the board for heat dissipation; thus, high thermal conductivity materials can effectively diffuse and cool over large areas, while low thermal conductivity materials cannot dissipate heat effectively, leading to excessively high temperatures on the substrate.The size of the PCB backplane is limited, and currently, it is mainly achieved through splicing to implement backlight technology. During the PCB board manufacturing process, it undergoes numerous reflows, and internal materials release internal stress, causing warping and bending, which becomes more severe as the size of the PCB increases, leading to optical display differences. Therefore, the size of a single PCB board generally does not exceed 24 inches, and large-sized backlights often require multiple PCB boards to be spliced together.Glass backplanes are expected to gradually replace PCB backplanes as the new solution for Mini LED backplanes. As the Mini LED process gradually shrinks, the transfer process will become more challenging. In comparison, glass backplanes have better flatness, do not require splicing, and possess better process precision, high thermal conductivity, and excellent heat dissipation performance, making them a trend to become the new solution for Mini LED backlighting.3. Mini LED Display: Upgrading Requirements for Chip Structure, Packaging, and Other Technologies3.1. Mini LED Display Continues the Small Pitch Technology Route, Ongoing MiniaturizationMini LED direct displays fill the gap between traditional LED displays and Micro LED technology. Since the 1990s, with significant breakthroughs in dynamic display systems and blue light-emitting lamps, LED displays have gradually evolved from monochrome and dual-color to full-color screens.After over a decade of development, LED chip sizes have continuously shrunk, and pixel spacing has also decreased, resulting in higher PPI.In 2010, Leyard launched the first 2.5mm small-pitch LED television, and small-pitch LED displays have rapidly developed since 2013 in specialized display fields such as government and public services.As pixel spacing further shrinks to below 1mm, LED displays are referred to as Mini LED displays. The size of Mini LED is smaller than that of small-pitch LED, with tighter LED chip arrangements and higher PPI, leading to increased difficulty in production, testing, and maintenance technology upgrades. Mini LED technology is similar to Micro LED, which will achieve superior display effects. Compared to small-pitch LEDs, Mini LED processes miniaturize and depackaging, sharing similarities with Micro LED technology paths, facilitating the development of related production and testing technologies, and accelerating the landing process of Micro LED. Micro LED can theoretically achieve better RGB performance, but there are currently technical challenges in mass transfer, driving ICs, epitaxial wafers, maintenance, etc., and costs are high, still in the technical accumulation stage.LED displays feature high brightness and can achieve ultra-large size displays, which other display technologies currently struggle to match. Traditional LED displays are mainly applied in outdoor ultra-large screen display fields. AIOT big data believes that small-pitch LED displays have advantages such as seamless display, good display effects, and long service life, and their costs have decreased rapidly in recent years, forming a trend to replace LCD and DLP. The application range has expanded from government public information displays to commercial displays. With increasing demand for small-pitch and ultra-small pitch displays in rental markets, HDR market applications, retail, and conference room markets, the demand for Mini LED TVs shows immense potential.Mini LED is a further extension of small-pitch LEDs. In direct display fields, Mini LED serves as an upgraded product of small-pitch displays, enhancing reliability and pixel density, with corresponding LED chip sizes ranging from 0.08 to 0.20mm, suitable for RGB displays. In backlighting fields, LCD displays employing Mini LED backlight technology significantly outperform ordinary LED backlit LCD displays in brightness, contrast, and color reproduction, competing directly with OLED. Micro LED (Micro Light Emitting Diode) miniaturizes traditional LED arrays into high-density integrated LED arrays, with pixel sizes below 50um.Mini/Micro LED is considered the mainstream and development trend of future LED display technology, representing a new product upgrade in LED display technology following indoor and outdoor LED displays and small-pitch LEDs, characterized by advantages of “film-like, miniaturization, and arraying,” gradually being introduced into industrial applications.The pitch of small-pitch LED beads has continuously upgraded from the initial 2.5mm, with 1.5-1.6mm becoming mainstream since 2017, and in 2019, the shipment proportion of 1.2-1.6mm reached 41.5%. In the coming years, pitches below 1.1mm will become the main driving force for small-pitch LEDs.

Mini LED technology is similar to Micro LED, which will achieve superior display effects. Compared to small-pitch LEDs, Mini LED processes miniaturize and depackaging, sharing similarities with Micro LED technology paths, facilitating the development of related production and testing technologies, and accelerating the landing process of Micro LED. Micro LED can theoretically achieve better RGB performance, but there are currently technical challenges in mass transfer, driving ICs, epitaxial wafers, maintenance, etc., and costs are high, still in the technical accumulation stage.LED displays feature high brightness and can achieve ultra-large size displays, which other display technologies currently struggle to match. Traditional LED displays are mainly applied in outdoor ultra-large screen display fields. AIOT big data believes that small-pitch LED displays have advantages such as seamless display, good display effects, and long service life, and their costs have decreased rapidly in recent years, forming a trend to replace LCD and DLP. The application range has expanded from government public information displays to commercial displays. With increasing demand for small-pitch and ultra-small pitch displays in rental markets, HDR market applications, retail, and conference room markets, the demand for Mini LED TVs shows immense potential.Mini LED is a further extension of small-pitch LEDs. In direct display fields, Mini LED serves as an upgraded product of small-pitch displays, enhancing reliability and pixel density, with corresponding LED chip sizes ranging from 0.08 to 0.20mm, suitable for RGB displays. In backlighting fields, LCD displays employing Mini LED backlight technology significantly outperform ordinary LED backlit LCD displays in brightness, contrast, and color reproduction, competing directly with OLED. Micro LED (Micro Light Emitting Diode) miniaturizes traditional LED arrays into high-density integrated LED arrays, with pixel sizes below 50um.Mini/Micro LED is considered the mainstream and development trend of future LED display technology, representing a new product upgrade in LED display technology following indoor and outdoor LED displays and small-pitch LEDs, characterized by advantages of “film-like, miniaturization, and arraying,” gradually being introduced into industrial applications.The pitch of small-pitch LED beads has continuously upgraded from the initial 2.5mm, with 1.5-1.6mm becoming mainstream since 2017, and in 2019, the shipment proportion of 1.2-1.6mm reached 41.5%. In the coming years, pitches below 1.1mm will become the main driving force for small-pitch LEDs. 3.2. Rapid Growth in Demand for Mini LED Displays in Commercial FieldsMini RGB self-luminous solutions are increasingly applied in commercial display markets, with significant application potential in scenarios such as theater displays, traffic advertising, rental displays, and sports displays. In public display fields, spliced video walls were originally one of the main applications, including technologies such as LCD, DLP, and small-pitch LEDs. DLP has low color saturation and high power consumption, while LCD video walls have seams. Therefore, small-pitch LED displays, which can be seamlessly spliced and flexibly set in size, are showing a trend of rapid growth.Displays are one of the important application fields downstream of LEDs. According to data from the National Semiconductor Lighting Engineering Research and Industry Alliance, the market size of China’s downstream LED application fields was 608 billion yuan in 2018, with LED general lighting, LED landscape lighting, LED display, and LED backlighting applications accounting for 48%, 14%, 13%, and 12% respectively. AIOT big data believes that as LED packaging device technologies continue to mature, LED displays have basically achieved high definition, high resolution, and stable long-term performance. The application scenarios for LED displays are increasingly diverse, widely used in advertising media, cultural performances, sports venues, high-end conference rooms, traffic control, high-end auto shows, security, and night economy fields, among which outdoor advertising and stage rental markets are already quite mature. According to data from the China LED Display Application Industry Association, from 2015 to 2019, China’s LED display sales increased from 31 billion yuan to 62.6 billion yuan, with an annual compound growth rate of 19.21%.

3.2. Rapid Growth in Demand for Mini LED Displays in Commercial FieldsMini RGB self-luminous solutions are increasingly applied in commercial display markets, with significant application potential in scenarios such as theater displays, traffic advertising, rental displays, and sports displays. In public display fields, spliced video walls were originally one of the main applications, including technologies such as LCD, DLP, and small-pitch LEDs. DLP has low color saturation and high power consumption, while LCD video walls have seams. Therefore, small-pitch LED displays, which can be seamlessly spliced and flexibly set in size, are showing a trend of rapid growth.Displays are one of the important application fields downstream of LEDs. According to data from the National Semiconductor Lighting Engineering Research and Industry Alliance, the market size of China’s downstream LED application fields was 608 billion yuan in 2018, with LED general lighting, LED landscape lighting, LED display, and LED backlighting applications accounting for 48%, 14%, 13%, and 12% respectively. AIOT big data believes that as LED packaging device technologies continue to mature, LED displays have basically achieved high definition, high resolution, and stable long-term performance. The application scenarios for LED displays are increasingly diverse, widely used in advertising media, cultural performances, sports venues, high-end conference rooms, traffic control, high-end auto shows, security, and night economy fields, among which outdoor advertising and stage rental markets are already quite mature. According to data from the China LED Display Application Industry Association, from 2015 to 2019, China’s LED display sales increased from 31 billion yuan to 62.6 billion yuan, with an annual compound growth rate of 19.21%. Small-pitch LEDs are showing a significant substitution effect in the large-screen splicing market against DLP and LCD. Small-pitch LED displays generally refer to LED displays with a resolution below P2.5 (inclusive). As SMD LED technology matures, small-pitch LED displays are gradually showing a trend of replacing traditional displays such as DLP and LCD. Compared to DLP and LCD, small-pitch LEDs have advantages such as seamless splicing, wide color gamut, low power consumption, and long lifespan; as well as the continuously decreasing prices of small-pitch LEDs, their market penetration in the large-screen splicing field is increasing. In 2020, small-pitch LEDs accounted for 61.2% of the Chinese large-screen splicing market, compared to 56.4% in 2019, an increase of 4.8%. Small-pitch LEDs continue to penetrate the indoor large-screen splicing market, accelerating the replacement of DLP and LCD.In cinema displays, Mini LED movie screens provide a high-quality visual experience. A typical movie screen that is 10 meters wide (diagonal 445 inches) can accommodate 150-240 viewers, while a 14-meter wide screen can hold 273 seats. Given that the audience is at a distance from the screen, P2.5 can meet the scene’s requirements. Mini LED screens can achieve HDR and high-brightness 3D experiences. With the unique advantages of Mini LED displays, despite currently being more expensive than traditional laser projection, Mini LED movie screens have the opportunity to secure a place in high-end cinemas.In large transportation advertising, excellent characteristics better match different scene requirements. Currently, major airports and stations domestically and internationally have extensively deployed LED displays, from information displays to advertising placements, LED displays have penetrated everywhere. There are numerous outstanding cases of LED displays in large global airports. Mini LED displays have smaller LED crystal particles, more robust overall screen integrity, better sealing, and optical design characteristics, overcoming issues such as small-pitch LED screens being easily damaged and COB products not being repairable on-site, thus excellently matching corresponding scene requirements.Rental displays with ultra-high-definition provide audiences with a stunning visual experience and artistic effects. Currently, rental displays mainly focus on high-end demands, such as stage performances, large exhibitions, and industrial design. With the development of the cultural and entertainment industry, the demand for high-quality LED displays is rapidly increasing. More 4K/8K displays will be presented for high-end concerts and exhibitions, and the rental display field often accompanies the demand for personalized customization, making full LED display companies capable of providing hardware facilities and control solutions likely to gain strong market competitiveness.In sports displays, the demand for LEDs in large international events is strong. LED displays have a long history of use in sports events. Large sports events often require clear, timely, and accurate responses to real-time match situations, making Mini LED display solutions likely to penetrate further. In the future, from international events to national and regional events, they will become important factors driving sports displays.4. Demand: Terminal Applications Drive Exceeding Expectations, Establishing the Commercialization Year for Mini LEDMini LED has vast application prospects in backlighting and displays. TVs, monitors, laptops, tablets, and in-car displays are potential fields where Mini LED backlighting is expected to penetrate. Mini LED RGB displays are gradually replacing traditional small-pitch and ultra-large size display solutions in commercial fields, continuously improving display effects. According to our calculations, the chip market driven by Mini LED backlighting exceeds 10 billion yuan, and the future space for Mini/Micro LED displays is very large, with market potential far exceeding that of backlighting, and there is still considerable room for improvement in technology maturity.Assumptions for TV Mini backlight shipments: Assuming that global TV shipments remain unchanged, the penetration rate for 55 inches and above continues to rise, with some high-end products featuring Mini LED backlight schemes, the mid-term penetration rate is projected at 10-15%.Assumptions for IT Mini backlight shipments: Assuming that global IT total shipments remain unchanged, penetration rates are expected to rise quickly due to Apple’s push (Apple’s iPad shipments of 50 million units, Mac shipments of 15-20 million units). In 2021, the new 12.9-inch iPad Pro is standard equipped with Mini LED backlighting, with annual sales of 5-6 million units, while the Macbook is optional (with Arm CPU costs reduced to offset). It is assumed that early penetration is primarily driven by Apple, with a higher unit price; later, Android will be introduced, leading to a decrease in average prices.Mini LED direct display demand estimation: Assuming that 10% of display devices are in Mini/Micro RGB display form, this implies an annual demand of 500 million units, approximately 2.5 times the current global capacity. Among these, TVs are the largest consumers, corresponding to 25 million chips for 4K TVs. The future space for Mini/Micro LED displays is very large, with market potential far exceeding that of backlighting, and there is still considerable room for improvement in technology maturity.The demand for high-end film materials for Mini LED is increasing, expected to drive a market space worth billions.Mini LED backlight TVs require the use of high-end new composite films and quantum dot films to improve display effects and achieve color emission solutions.Based on the aforementioned shipment assumptions, we estimate that the high-end film material market driven by Mini LED could reach the billion level by 2024.As technology matures, quantum dot films may also be integrated into composite films, at which point the value of composite films will increase.Transfer equipment will benefit sequentially from the large-scale release of Mini LED backlighting and direct displays, with significant elasticity. From the perspective of transfer equipment, due to the significant differences in efficiency and prices of different specifications of equipment in the industry, taking the industry’s central position as a reference. Through calculations, it has been found that Mini LED transfer solid crystal equipment will benefit rapidly from the large-scale release of Mini LED backlighting in these two years; in the future, it will benefit from the commercialization and large-scale release of Mini/Micro LED direct display TV products, which will have even greater elasticity.5. Technology: Active Layout of Various Links in the Industry Chain Supports the Rapid Rise of Mini LEDMini/Micro LED technology continues to upgrade, with numerous participants in the industry chain. In comparison, Mini LED display technology is relatively mature, gradually starting to penetrate commercialization in 2020/2021; Micro LED, due to higher technical specifications, is still in the technical introduction phase, with key technical difficulties including micro LED and mass transfer. For a micro LED display product, the basic components include substrates, micro LED chips, driving ICs, etc., with industry chain links including LED chip manufacturers, panel manufacturers, IC manufacturers, material manufacturers, LED packaging manufacturers, and LED application manufacturers.

Small-pitch LEDs are showing a significant substitution effect in the large-screen splicing market against DLP and LCD. Small-pitch LED displays generally refer to LED displays with a resolution below P2.5 (inclusive). As SMD LED technology matures, small-pitch LED displays are gradually showing a trend of replacing traditional displays such as DLP and LCD. Compared to DLP and LCD, small-pitch LEDs have advantages such as seamless splicing, wide color gamut, low power consumption, and long lifespan; as well as the continuously decreasing prices of small-pitch LEDs, their market penetration in the large-screen splicing field is increasing. In 2020, small-pitch LEDs accounted for 61.2% of the Chinese large-screen splicing market, compared to 56.4% in 2019, an increase of 4.8%. Small-pitch LEDs continue to penetrate the indoor large-screen splicing market, accelerating the replacement of DLP and LCD.In cinema displays, Mini LED movie screens provide a high-quality visual experience. A typical movie screen that is 10 meters wide (diagonal 445 inches) can accommodate 150-240 viewers, while a 14-meter wide screen can hold 273 seats. Given that the audience is at a distance from the screen, P2.5 can meet the scene’s requirements. Mini LED screens can achieve HDR and high-brightness 3D experiences. With the unique advantages of Mini LED displays, despite currently being more expensive than traditional laser projection, Mini LED movie screens have the opportunity to secure a place in high-end cinemas.In large transportation advertising, excellent characteristics better match different scene requirements. Currently, major airports and stations domestically and internationally have extensively deployed LED displays, from information displays to advertising placements, LED displays have penetrated everywhere. There are numerous outstanding cases of LED displays in large global airports. Mini LED displays have smaller LED crystal particles, more robust overall screen integrity, better sealing, and optical design characteristics, overcoming issues such as small-pitch LED screens being easily damaged and COB products not being repairable on-site, thus excellently matching corresponding scene requirements.Rental displays with ultra-high-definition provide audiences with a stunning visual experience and artistic effects. Currently, rental displays mainly focus on high-end demands, such as stage performances, large exhibitions, and industrial design. With the development of the cultural and entertainment industry, the demand for high-quality LED displays is rapidly increasing. More 4K/8K displays will be presented for high-end concerts and exhibitions, and the rental display field often accompanies the demand for personalized customization, making full LED display companies capable of providing hardware facilities and control solutions likely to gain strong market competitiveness.In sports displays, the demand for LEDs in large international events is strong. LED displays have a long history of use in sports events. Large sports events often require clear, timely, and accurate responses to real-time match situations, making Mini LED display solutions likely to penetrate further. In the future, from international events to national and regional events, they will become important factors driving sports displays.4. Demand: Terminal Applications Drive Exceeding Expectations, Establishing the Commercialization Year for Mini LEDMini LED has vast application prospects in backlighting and displays. TVs, monitors, laptops, tablets, and in-car displays are potential fields where Mini LED backlighting is expected to penetrate. Mini LED RGB displays are gradually replacing traditional small-pitch and ultra-large size display solutions in commercial fields, continuously improving display effects. According to our calculations, the chip market driven by Mini LED backlighting exceeds 10 billion yuan, and the future space for Mini/Micro LED displays is very large, with market potential far exceeding that of backlighting, and there is still considerable room for improvement in technology maturity.Assumptions for TV Mini backlight shipments: Assuming that global TV shipments remain unchanged, the penetration rate for 55 inches and above continues to rise, with some high-end products featuring Mini LED backlight schemes, the mid-term penetration rate is projected at 10-15%.Assumptions for IT Mini backlight shipments: Assuming that global IT total shipments remain unchanged, penetration rates are expected to rise quickly due to Apple’s push (Apple’s iPad shipments of 50 million units, Mac shipments of 15-20 million units). In 2021, the new 12.9-inch iPad Pro is standard equipped with Mini LED backlighting, with annual sales of 5-6 million units, while the Macbook is optional (with Arm CPU costs reduced to offset). It is assumed that early penetration is primarily driven by Apple, with a higher unit price; later, Android will be introduced, leading to a decrease in average prices.Mini LED direct display demand estimation: Assuming that 10% of display devices are in Mini/Micro RGB display form, this implies an annual demand of 500 million units, approximately 2.5 times the current global capacity. Among these, TVs are the largest consumers, corresponding to 25 million chips for 4K TVs. The future space for Mini/Micro LED displays is very large, with market potential far exceeding that of backlighting, and there is still considerable room for improvement in technology maturity.The demand for high-end film materials for Mini LED is increasing, expected to drive a market space worth billions.Mini LED backlight TVs require the use of high-end new composite films and quantum dot films to improve display effects and achieve color emission solutions.Based on the aforementioned shipment assumptions, we estimate that the high-end film material market driven by Mini LED could reach the billion level by 2024.As technology matures, quantum dot films may also be integrated into composite films, at which point the value of composite films will increase.Transfer equipment will benefit sequentially from the large-scale release of Mini LED backlighting and direct displays, with significant elasticity. From the perspective of transfer equipment, due to the significant differences in efficiency and prices of different specifications of equipment in the industry, taking the industry’s central position as a reference. Through calculations, it has been found that Mini LED transfer solid crystal equipment will benefit rapidly from the large-scale release of Mini LED backlighting in these two years; in the future, it will benefit from the commercialization and large-scale release of Mini/Micro LED direct display TV products, which will have even greater elasticity.5. Technology: Active Layout of Various Links in the Industry Chain Supports the Rapid Rise of Mini LEDMini/Micro LED technology continues to upgrade, with numerous participants in the industry chain. In comparison, Mini LED display technology is relatively mature, gradually starting to penetrate commercialization in 2020/2021; Micro LED, due to higher technical specifications, is still in the technical introduction phase, with key technical difficulties including micro LED and mass transfer. For a micro LED display product, the basic components include substrates, micro LED chips, driving ICs, etc., with industry chain links including LED chip manufacturers, panel manufacturers, IC manufacturers, material manufacturers, LED packaging manufacturers, and LED application manufacturers. Chip yield and consistency requirements are high. The consistency of Mini LED chips includes high-low consistency, color consistency, etc., while the maintenance difficulties of Mini LED displays are also significant technical challenges. Among them, red flip-chip LED chips generally require substrate transfer and solid crystal welding, thus facing higher yield challenges.The rapid miniaturization of Mini LED pixel spacing has significantly increased the design difficulty at the chip level, directly leading to low yields for Mini LED chips. Unlike LED chip front-mounted technology and vertical technology, flip-chip technology has advantages such as low voltage, high brightness, high reliability, and high saturation. Additionally, it can integrate protection circuits on the substrate of flip-chip welding, significantly aiding chip reliability. At the same time, flip-chip technology, which does not require gold wire on electrodes, can save significant costs, making it very suitable for densely packed applications. Flip-chip saturated currents are high, especially under high currents, showcasing advantages. Currently, the industry has universally adopted flip-chip structures in Mini LED chip design. Among them, blue and green flip-chip technology is relatively mature with higher yields, while red flip-chip technology generally requires substrate transfer and solid crystal welding, making it susceptible to process environment and uncontrollable factors, thus facing challenges in yield and reliability.

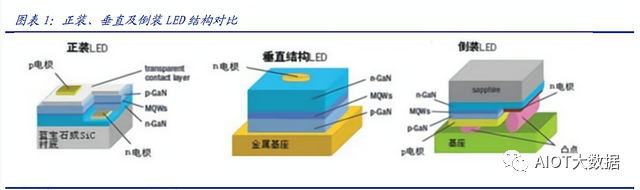

Chip yield and consistency requirements are high. The consistency of Mini LED chips includes high-low consistency, color consistency, etc., while the maintenance difficulties of Mini LED displays are also significant technical challenges. Among them, red flip-chip LED chips generally require substrate transfer and solid crystal welding, thus facing higher yield challenges.The rapid miniaturization of Mini LED pixel spacing has significantly increased the design difficulty at the chip level, directly leading to low yields for Mini LED chips. Unlike LED chip front-mounted technology and vertical technology, flip-chip technology has advantages such as low voltage, high brightness, high reliability, and high saturation. Additionally, it can integrate protection circuits on the substrate of flip-chip welding, significantly aiding chip reliability. At the same time, flip-chip technology, which does not require gold wire on electrodes, can save significant costs, making it very suitable for densely packed applications. Flip-chip saturated currents are high, especially under high currents, showcasing advantages. Currently, the industry has universally adopted flip-chip structures in Mini LED chip design. Among them, blue and green flip-chip technology is relatively mature with higher yields, while red flip-chip technology generally requires substrate transfer and solid crystal welding, making it susceptible to process environment and uncontrollable factors, thus facing challenges in yield and reliability. Mass transfer primarily refers to transferring a large number of micro LED chips to substrates through adhesion, with the core focusing on transfer efficiency and yield. There are many transfer technology solutions available in the market. Currently, stress adhesion and transfer are the mainstream methods, achieving more precise and smaller LED chip transfers, but the number of chips transferred in each operation is relatively small. Other methods include static transfer used by Longda and low-temperature bonding technology used by Mikro Mesa. The bottlenecks that mass transfer must overcome include equipment precision, transfer yield, transfer time, process technology, detection methods, reworkability, and processing costs.Rohinni significantly enhances transfer yield and efficiency, continuously increasing the cost competitiveness of scale production. Rohinni’s new composite transfer head can achieve over 99.999% placement yield, with a speed of transferring over 100 chips per second (i.e., over 100 times per second). This technology can be integrated into multi-head systems and has a significant speed advantage compared to existing pick-and-place technologies, making it a cost-effective technical solution for large-scale production of consumer electronic displays. Rohinni and its joint venture company BOE Pixey are entering the stage of large-scale production of Mini LED displays.Mini LED packaging mainly includes two solutions: COB (Chip on Board) technology and IMD (Integrated Mounted Devices) technology. COB technology directly packages LED chips onto the module substrate, encapsulating each unit as a whole. IMD technology integrates multiple groups (two, four, or six) of RGB beads into a small unit.COB packaging has advantages such as low power consumption, good heat dissipation, high saturation, high resolution, and no size restrictions on screen dimensions. However, the challenges of Mini COB packaging technology mainly lie in optical consistency and PCB ink color consistency. IMD can be seen as a small COB, facing challenges similar to those of COB packaging technology, but with reduced difficulty. Compared to COB technology, IMD technology enhances the mounting efficiency on the application side and improves the reliability of RGB chip packaging.UV/blue LED + luminescent medium method is currently an important way to achieve full-color light sources. Traditional luminescent media use phosphor, which has low conversion rates and larger granules; thus, quantum dot (nanocrystal) technology is gradually demonstrating superiority. Quantum dots exhibit electroluminescence and photoluminescence effects, emitting fluorescence when excited, with the emitted light color determined by the material and size. Therefore, adjusting the particle size of quantum dots can change their emitted light wavelengths. Quantum dots have diverse chemical compositions, and their emitted colors can cover the entire visible range from blue to red. Additionally, quantum dots possess high light absorption-emission efficiency, narrow half-widths, and wide absorption spectra, resulting in high color purity and saturation; moreover, quantum dot technology has a simple structure, thin profile, and flexibility.The Mini LED industry chain can be roughly divided into five links: chips, packaging/mass transfer and assembly, panels, systems (assembly), and brands.Chips: The chip manufacturing link involves a series of semiconductor processes to prepare epitaxial wafers into luminous particles, followed by testing key indicators, wafer grinding, cutting, sorting, and packaging. The current challenges in Mini LED chips include: 1) red flip-chip chips face issues of process consistency and low optical efficiency during small size cutting. 2) The miniaturization of chip size increases the precision requirements for equipment etching/lithography. 3) The consistency and reliability of LED chips, as well as maintenance requirements, are heightened.Packaging/mass transfer: Packaging mainly includes two solutions: COB is where LED chips are directly packaged onto the module substrate, while IMD integrates multiple groups of RGB beads into a small unit. The mass transfer technology link involves sorting chips and transferring them, with challenges in device sorting algorithms, transfer efficiency, and yield control.Panels: Panel manufacturers extending into glass substrate backlight solutions are expected to gain a stronger competitive position in the industry chain.Systems (assembly): Companies in the industry chain are continuously making progress in product introduction, research and development, and shipments. Foxconn is assembling the new Mini LED backlit iPads for international clients. Unilumin’s P0.7 products have been shipped in bulk. Leyard’s LCD module (LCM) with a thickness of 2.2mm backlight module is now in mass production, and modules of 2.0mm and below have been sent to both international and domestic clients for sampling.Mini LED Industry Chain OverviewThe industry chain includes upstream chip manufacturing, midstream packaging, and downstream module manufacturing. In the upstream chip manufacturing, GaN-based/GaAs-based epitaxial wafers are produced on substrates such as sapphire, SiC, or silicon wafers, followed by etching, cleaning, and other steps to obtain different types of LED chips. LED chip suppliers include mainland manufacturers such as Sanan Optoelectronics, HC Semitek, and Qian Zhao Optoelectronics, as well as Taiwanese manufacturers such as Epistar and foreign manufacturers such as Osram and Nichia. The midstream packaging link forms granulated finished products after solid crystal, wire bonding, glue application, and encapsulation steps, mainly serving to mechanically protect, enhance heat dissipation, improve LED performance, and optimize light distribution. Major LED packaging manufacturers include mainland companies like Nationstar Optoelectronics, Mulinsen, and Hongli Zhihui, as well as Taiwanese manufacturers like Epistar.Direct display and backlight module manufacturing are the downstream applications of the Mini LED industry chain. Direct display manufacturers include Leyard, Unilumin Technology, and Lehman Optoelectronics, while backlight module manufacturers include Zhaochi and Ruidi Optoelectronics. Additionally, panel manufacturers have also entered the Mini LED product manufacturing space, with TCL Technology and BOE both making strides. TCL launched the world’s first Mini LED Starry Screen using a glass substrate integrated LED solution in 2019, which has better performance advantages than existing PCB integration solutions and began mass production in 2020. In 2019, BOE established a joint venture with the U.S. company Rohinni to jointly develop Mini/Micro LED solutions. After overcoming technical challenges, BOE’s glass-based Mini LED backlight products achieved mass production and shipment in the fourth quarter of 2020, with initial deliveries focused on 65-inch and 75-inch TV products, with plans to expand product varieties based on customer demand and capacity conditions.Mainland Manufacturers Continue to Ramp Up, Taiwanese Manufacturers Form AlliancesCurrently, mainland LED industry chains are actively laying out Mini LED-related technologies and products. Leading LED chip manufacturer Sanan Optoelectronics has begun bulk shipments of Mini LED chips to domestic and international downstream clients such as TCL Huaxing and Samsung Electronics. Moreover, Sanan Optoelectronics’ wholly-owned subsidiary Quanzhou Sanan Semiconductor has jointly invested 300 million yuan with Huaxing Optoelectronics to establish a joint laboratory focusing on tackling key technological challenges in Micro-LED display engineering, including Micro-LED chip technology, transfer, bonding, colorization, detection, and repair. In the packaging and testing segment, mainland companies like Nationstar, Hongli Zhihui, and Ruidi Optoelectronics have all achieved mature product shipments. Nationstar has collaborated deeply with several domestic and foreign display companies, and multiple large-sized TV backlight products have achieved mass production. Ruidi has closely cooperated with well-known domestic and foreign electronics companies to develop various Mini LED backlight and display product solutions for applications in tablets, laptops, and TVs, and has led the market in releasing multiple Mini LED products. Meanwhile, downstream application manufacturers are also making frequent moves. In 2020, Leyard and Epistar established the world’s first large-scale production base for Mini/Micro LED in Wuxi, mainly focusing on the mass transfer technology of Mini/Micro LEDs, while integrating the production of self-luminous and backlight modules. Additionally, other manufacturers are actively promoting the industrialization of Mini LEDs. Unilumin has established a standard product line for Mini LED displays and achieved bulk production of P0.9 Mini LED products. The company also announced plans to add several new Mini LED intelligent production lines at its Huizhou base in 2020 to expand production capacity. Zhaochi’s Mini RGB products have completed product definition and achieved 4K display under 110 inches, 135 inches, and 162 inches, with Mini LED chips already entering small-scale trial production.As Mini LED requires higher precision transfer, assembly, and sorting equipment, related equipment companies such as ASM Pacific are also actively laying out related technologies and solutions. ASM Pacific has launched a fully automatic mass soldering production line, Ocean Line, which can transfer up to 10,000 LEDs at a time, achieving better gray control with excellent flatness, thus avoiding color difference issues even from different angles. Additionally, on the PCB side, the global leader, Pengding, is one of the few manufacturers mastering Mini LED backlight circuit board technology, and the company has laid out related production capacity in Huai’an, with the first phase of the project having been put into operation by the end of 2020, and the second phase expected to be put into operation in the second half of 2021.Under the pressure of production capacity from mainland manufacturers, Taiwanese manufacturers have begun to form alliances: Epistar and Longda jointly established Fucai Holding to seize Apple orders. In recent years, as mainland LED manufacturers have risen, the influence of Taiwanese manufacturers has diminished, with most unable to expand production capacity on a large scale to cooperate with brand manufacturers. Coupled with the alliances formed between mainland LED manufacturers and panel manufacturers increasing capital expenditures, the sense of crisis among Taiwanese manufacturers has greatly increased, prompting them to actively seek cooperation opportunities. In January 2020, the Taiwanese chip leader Epistar and packaging manufacturer Longda jointly established Fucai Holding Group, where Epistar focuses on LED chip epitaxy and granulation, while Longda primarily targets packaging technology. The alliance strategy among Taiwanese manufacturers has proven effective, with Fucai Holding quickly securing Apple orders. According to industry insiders cited by the Electronic Times, Fucai Holding is expected to begin producing Mini LED screens for the upcoming 12.9-inch iPad Pro in the first half of this year. Additionally, Taiwanese manufacturer Ruidi Optoelectronics will serve as a foundry for Apple’s Mini LED backlight modules. Apart from Taiwanese manufacturers, European and American companies are also actively vying for Apple orders. Osram plans to continue expanding equipment investments to produce Mini LED chips and is expected to ship Mini LED backlight boards for MacBooks to Apple in the second half of this year, with an initial monthly capacity of 100 million chips established in Malaysia.Exploring Mini LED Industry Development Trends from a Technological PerspectiveAs various links in the industry chain continue to ramp up, Mini LED technology is at a critical point of landing. Therefore, in terms of technology, many new technologies and variables have emerged, including chip, packaging, and substrate selection. This chapter will sort through the latest processes and technologies of Mini LED, exploring the technological directions most suitable for the development rules of the Mini LED industry chain, thereby providing guidance for investments in the Mini LED industry chain.Manufacturing Processes Are Relatively Mature, Transfer Technology Continues to InnovateThe LED chip manufacturing process primarily includes the front-end epitaxial wafer manufacturing, mid-stage epitaxy, and back-end chip cutting, involving dozens of specific processes, making it highly complex. However, due to the years of development in the LED industry, traditional LED chip manufacturing equipment and processes have become relatively mature, and the requirements for cutting precision and transfer equipment for Mini LED are not as stringent as those for Micro LED, making the difficulty of Mini LED chip manufacturing relatively lower. Chip manufacturers only need to enhance yields and output through process optimization to transition from conventional sizes to Mini sizes. In terms of transfer technology, compared to Micro LED, Mini LED has larger sizes and more rigid substrates, allowing for higher precision tolerances and greater flexibility during the transfer process. Currently, mainstream manufacturers are developing Mini LED-related transfer technologies, primarily including the following three: 1) The first scheme improves existing grabbing devices by setting multiple arms to increase pick-and-place efficiency. This scheme has lower technical difficulty, making it easier to achieve mass production, but it has capacity limitations and cannot achieve a large-scale increase. 2) The second scheme places the chip relative to the backplane and uses a pin to push the chip out for placement on the substrate. Compared to the first scheme, this one reduces repetitive movements of the arms, thus enhancing transfer efficiency. Moreover, if the chip’s placement on the blue film aligns with the control electrode position on the final backplane, along with multiple pins, it can achieve mass transfer, significantly improving transfer efficiency. 3) The third scheme is similar to the second, where chips are placed on a UV film and selectively transferred to the backplane using UV light. This scheme can achieve true mass transfer, but it requires high precision in chip sorting and placement on the UV film.Full Flip-Chip + COB, Forming a New Trend in Packaging TechnologyLED packaging technology is transitioning from traditional bracket-type packaging (such as SMD technology) to new bracket-free integrated packaging (such as COB technology). Traditional LED packaging technology primarily uses SMD (Surface Mounted Devices) technology, which employs flat brackets + glue forming and is assembled using surface mount technology, with flat copper pins that can be mounted on aluminum substrates or PCBs. Its process flow includes solid crystal, wire bonding, forming, cutting, sorting, and warehousing. SMD technology can achieve stable pixel spacing in the range of 1.2-1.5mm, possessing mature and stable technology, low manufacturing costs, good heat dissipation, and easy maintenance, making it a highly mature LED packaging technology.However, as LEDs develop towards Mini/Micro directions, the application of SMD technology is beginning to face limitations. Its low protection level and short lifespan defects have become apparent, especially when manufacturing display products with pixel spacing below P1.2, where SMD packaging technology encounters numerous insurmountable technical bottlenecks. For example, SMD technology cannot meet the panel-level pixel failure rate requirements for Mini LED display products. COB (Chip On Board) packaging technology is a bracket-free integrated packaging technology where LED chips are directly mounted on the PCB, achieving high integration pixel panel-level packaging on one side of the PCB while placing driving IC components on the other side without the need for any brackets or solder joints.Compared to traditional SMD technology, COB technology significantly reduces pixel failure issues in LED display panels and can achieve smaller dot pitches with higher arrangement densities. Therefore, COB technology is essential for significantly enhancing the pixel density and overall reliability of LED display systems, providing fundamental high-end panel manufacturing technology for 4K, 8K ultra-high-definition display products and Mini LED displays, making it an inevitable choice as LED display technology advances towards the million-level. Additionally, there are various limited integration packaging technologies between SMD and COB, mainly including 2in1, 4in1, and Nin1 packaging technologies. This technology is essentially a hybrid of SMD and COB packaging, reducing the number of bracket pins, reflecting the integrated idea of COB packaging, but it cannot truly eliminate the panel-level pixel failure issues at the million or ten-thousand levels, facing the same technical bottlenecks as SMD packaging technology in the Mini LED pixel range of 1.2-0.9mm.In addition to COB technology, the packaging side has innovatively introduced flip-chip processes to achieve higher luminous efficiency, arrangement density, and reliability. Traditional front-mounted technology has drawbacks such as electrode occlusion affecting luminous efficiency and complex processes with many solder joints. Flip-chip technology, by inverting the chip, allows light emitted from the light-emitting layer to be emitted directly from the other side of the electrode, avoiding electrode occlusion and solder joints in the packaging process, thus maximizing the luminous area and heat dissipation area and avoiding issues caused by poor soldering and contact. Moreover, the absence of solder joints can enhance chip arrangement density, further promoting LED displays to increase pixel density.Currently, in the pixel spacing range above 1.2mm, front-mounted chips can still be used, while in the pixel spacing range of 1.2-0.7mm, there are solutions for red front-mounted and blue-green flip-mounted chips. In the pixel range of 0.7-0.3mm, RGB must use flip-mounted chips. As LED technology accelerates towards Mini/Micro directions, flip-chip technology is expected to achieve rapid penetration.In summary, for the Mini LED industry, SMD packaging technology is currently the most mature and cost-effective packaging combination, which will be used in the promotion of mid-range Mini LED products. Looking towards the future, flip-chip COB technology is a new type of packaging technology aimed at the future, which will further amplify its luminous effect advantages, reliability advantages, and high-density arrangement advantages, likely achieving a replacement of SMD technology.Substrate Selection: PCB Opens the Market, Glass Substrate Poised for LaunchThe substrate is the carrier for LED chips, and Mini LED substrates include PCB solutions and glass substrate solutions. Currently, PCB is the most commonly used LED substrate, with advantages of mature technology and low costs, primarily promoted by LED industry chain manufacturers. Glass substrates are one of the key materials for LCDs, later promoted to LED substrates by panel manufacturers. As Mini LED applications deepen, higher requirements have been raised for substrates, and the relevant industrial landscape is expected to undergo changes. This section will compare the two substrates in terms of cost, performance, application, and prospects. From a material perspective, the price of PCB substrates is several times that of glass substrates, so if produced on a large scale, the material costs of glass substrates are actually lower. However, in terms of comprehensive costs, glass substrates require light masks for wiring, resulting in higher initial investment costs; if the production scale is not high, the average cost may exceed that of PCB substrates. Additionally, in terms of yield, domestic packaging manufacturers currently have more mature technology for PCB substrates, with stronger reliability and higher yield rates, making cost controllability stronger. Conversely, glass substrates have lower yield rates due to their fragility.Therefore, overall, PCB substrates currently still have cost advantages, but in the long term, as the scale and yield rates of glass substrates improve, the costs of glass substrates are expected to significantly decrease, possibly even below those of PCB substrates. In terms of performance, PCB substrates have weaker heat dissipation than glass substrates and are prone to warping and deformation during chip soldering due to high thermal density, especially in large-sized applications, leading to seam issues during the splicing of multiple backlight units. In contrast, glass substrates have low thermal expansion rates and strong heat dissipation, resulting in higher flatness, which is more conducive to the soldering of Mini LEDs, thus meeting high precision requirements.In terms of application prospects, PCB substrates are currently the first choice under domestic technical conditions, currently used in the vast majority of LED products. For scenarios requiring higher heat dissipation, higher flatness, or high-density assembly, glass substrates will be a better choice. At CES 2020, TCL officially launched the “MLED Starry Screen” using a glass-based Mini LED solution. This product features ultra-high brightness and outstanding imaging even in backlight conditions; its contrast ratio reaches 1,000,000 to 1, significantly improving compared to traditional LCDs; and it also performs well in HDR and dynamic backlight partitioning.In summary, we believe that for Mini LED products at this stage, PCB substrates are the choice of terminal manufacturers when market demand is relatively low, considering both cost and performance. Looking towards the future, as Mini LED demand increases, glass substrates are expected to achieve large-scale shipments, leading to cost dilution. At that point, the competitive advantages of glass substrates will be fully demonstrated, likely achieving a replacement of PCB substrates.