👆If you wish to meet often, feel free to star 🌟 and bookmark it~

👆If you wish to meet often, feel free to star 🌟 and bookmark it~

Source: Content from Semiconductor Chip News.

Sales of semiconductor (chip) manufacturing equipment in Japan continue to thrive, with a significant increase of 17% in sales in June 2025, marking 15 consecutive months of double-digit growth (over 10%). Monthly sales have exceeded 400 billion yen for eight consecutive months, setting a historical record for the same period.

The Japan Semiconductor Equipment Association (SEAJ) announced on the 23rd that the sales of Japanese chip manufacturing equipment (3-month moving average, including exports) reached 404.592 billion yen in June 2025, a 17.6% increase compared to the same month last year, marking the 18th consecutive month of growth, with double-digit growth for 15 months. Monthly sales have surpassed 300 billion yen for 20 consecutive months, exceeding 400 billion yen for eight months, setting a historical record since statistics began in 1986.

Compared to the previous month (May 2025), there was a decline of 9.3%, marking the second consecutive month of month-on-month decrease.

In the first half of 2025 (January to June), the total sales of Japanese chip equipment reached 2 trillion 559.176 billion yen, a staggering increase of 20.0% compared to the same period last year, far exceeding the 2 trillion 1320.23 billion yen in 2024, setting a historical record.

Japan’s share of the global semiconductor equipment market (based on sales) reached 30%, ranking second in the world after the United States.

On July 3, SEAJ released an estimated report indicating that due to strong demand for AI server GPUs and HBM, Taiwan’s advanced wafer foundry (TSMC) will begin mass production of 2nm technology, with increased investment in 2nm, along with increased investment in DRAM/HBM in South Korea. Therefore, for the fiscal year 2025 (April 2025 – March 2026), the sales of Japanese chip equipment (referring to the sales of Japanese companies both domestically and overseas) have been revised upward from the previous estimate of 4 trillion 659 billion yen to 4 trillion 863.4 billion yen, which is a 2.0% increase compared to the fiscal year 2024, marking the second consecutive year of record high annual sales. The sales of Japanese chip equipment in fiscal year 2024 surged by 29.0% to 4 trillion 768.1 billion yen, marking the first time it has surpassed the 4 trillion yen mark, setting a historical record.

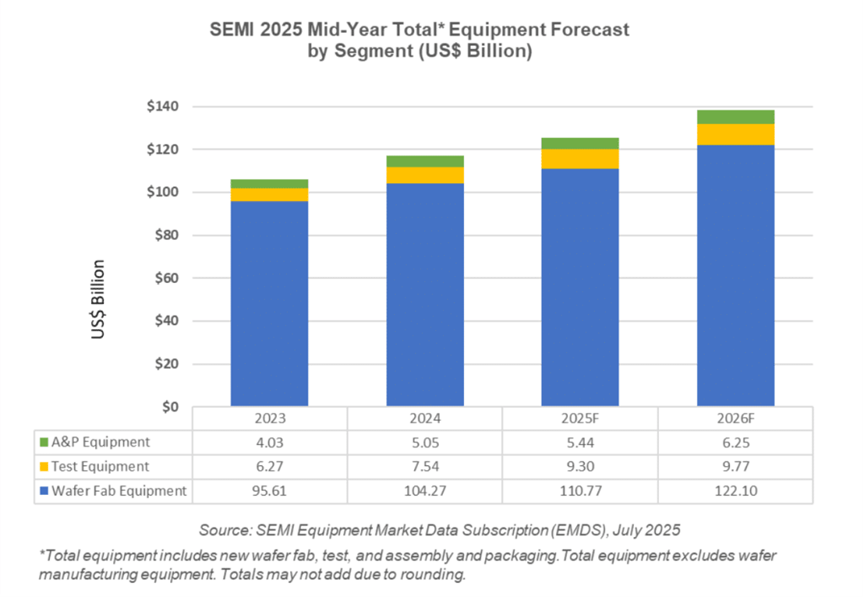

Chip equipment sales are approaching 122.5 billion USD

SEMI announced today that according to its “Mid-Year Semiconductor Equipment Overall Forecast – OEM Perspective,” the total sales of semiconductor manufacturing equipment by original equipment manufacturers (OEMs) is expected to reach a record high of 125.5 billion USD in 2025, a year-on-year increase of 7.4%. It is expected that semiconductor manufacturing equipment will continue to grow in 2026, with sales expected to reach a new high of 138.1 billion USD, mainly driven by advanced logic, memory, and technology transformation.

SEMI President and CEO Ajit Manocha stated: “Following strong growth in 2024, global semiconductor manufacturing equipment sales are expected to grow again this year and set a new record in 2026. Despite the semiconductor industry closely monitoring macroeconomic uncertainties, the demand for chip innovation driven by artificial intelligence is propelling capacity expansion and investment in cutting-edge production.”

Semiconductor Equipment Sales (by Sector)

Sales in the Wafer Fab Equipment (WFE) sector (including wafer processing, fab facilities, and mask/photomask equipment) are expected to grow by 6.2% to 110.8 billion USD by 2025, following a record high of 104.3 billion USD last year. This upward revision from SEMI’s end-of-year 2024 equipment forecast of 107.6 billion USD is mainly due to increased sales in foundry and memory applications. Looking ahead to 2026, WFE sector sales are expected to grow by 10.2%, reaching 122.1 billion USD. This growth is attributed to capacity expansion in advanced logic and memory to support AI applications, as well as ongoing process technology migrations across major segments.

The backend equipment sector is expected to continue the strong recovery that began in 2024. Following a year-on-year growth of 20.3% in 2024, semiconductor test equipment sales are expected to grow by another 23.2% in 2025, reaching a new high of 9.3 billion USD. Assembly and packaging equipment sales, which grew by 25.4% in 2024, are expected to grow by 7.7% in 2025, reaching 5.4 billion USD. The backend equipment sector is expected to continue expanding in 2026, with test equipment sales growing by 5.0% and assembly and packaging sales growing by 15.0%, achieving three consecutive years of growth. Factors driving this expansion include significant increases in equipment architecture complexity and strong performance requirements for AI and high-bandwidth memory (HBM) semiconductors. However, the ongoing weakness in the automotive, industrial, and consumer end markets may partially offset growth in this sector.

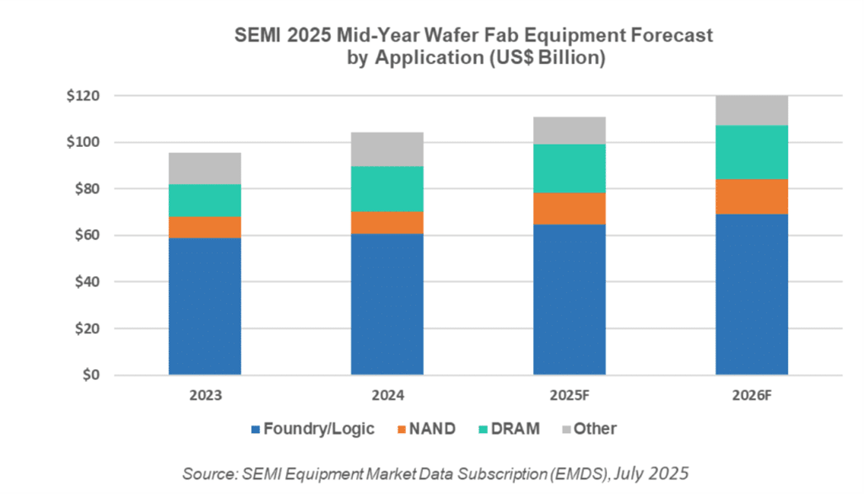

WFE Sales (by Application)

By 2025, WFE sales for foundry and logic applications are expected to grow by 6.7% year-on-year, reaching 64.8 billion USD, primarily driven by strong demand for advanced nodes. By 2026, this sector is expected to grow by another 6.6%, reaching 69 billion USD. As the industry moves towards mass production at the 2nm gate-all-around (GAA) node, increased procurement for capacity expansion and ongoing demand for cutting-edge technology will support this growth.

Memory-related capital expenditures are expected to increase in 2025 and continue to grow in 2026. NAND equipment sales are expected to recover from a sharp decline in 2023. Following a slight growth of 4.1% in 2024, NAND equipment market size is expected to grow by 42.5% in 2025, reaching 13.7 billion USD, and by 9.7% in 2026, reaching 15 billion USD, primarily driven by advancements in 3D NAND stacking technology and capacity expansion. Meanwhile, DRAM equipment sales surged by 40.2% in 2024, reaching 19.5 billion USD, and are expected to grow by 6.4% and 12.1% in 2025 and 2026, respectively, to support HBM (high-bandwidth memory) investments for AI deployments.

Regional Semiconductor Equipment Sales

By 2026, mainland China, Taiwan, and South Korea are expected to remain the top three destinations for equipment spending. During the forecast period, mainland China will continue to lead all regions, although sales in the region are expected to decline from the record investment of 49.5 billion USD in 2024. All other regions, except Europe, are expected to see significant growth in equipment spending starting in 2025. However, increasing trade policy risks may affect the growth rates across regions.

Click here 👆 to follow for more original content

*Disclaimer: The content of the article represents the author’s personal views. Semiconductor Chip News reprints it solely to convey a different perspective and does not endorse or support this view. If there are any objections, please feel free to contact us.

Recommended Reading

10 trillion, invested in semiconductors

Chip giants, market value plummets

Jensen Huang: HBM is a technological marvel

Jim Keller: RISC-V will definitely prevail

The 10 highest-valued chip companies in the world

If you like our content, please click“Looking”” to share with your friends~