This article was originally published in IoT Insights on July 31, 2025, translated by Aerospace Yuxing.

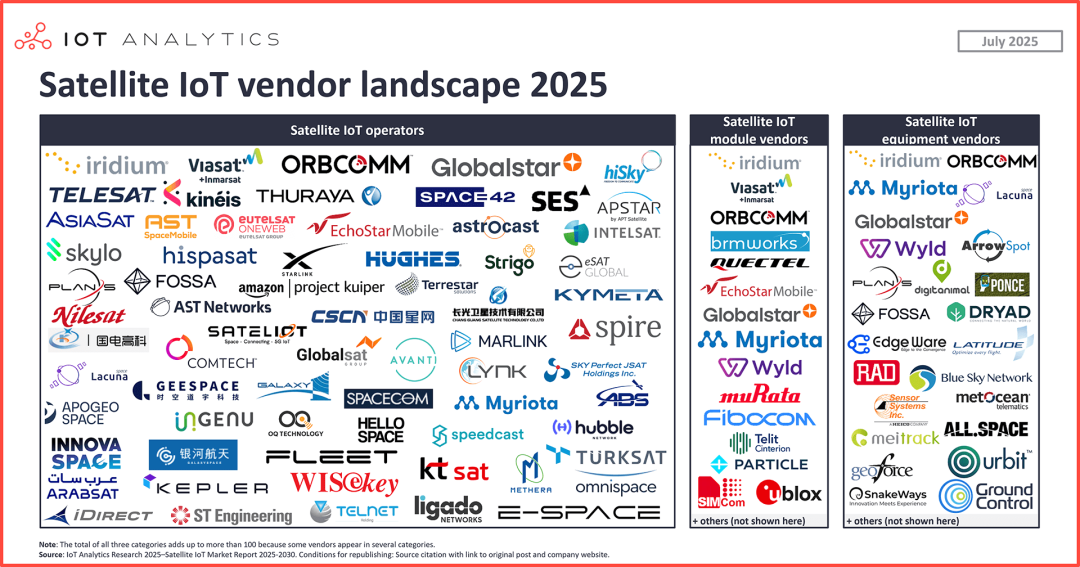

The latest IoT analysis report reveals the competitive landscape of satellite IoT: market fragmentation is intensifying, with over a hundred suppliers vying for market share, and market share is shifting from traditional operators to other entities.

The introduction of standards such as 3GPP Non-Terrestrial Networks (NTN) and support from government policies and investments are lowering the market entry barriers for new satellite IoT operators while creating new market opportunities for traditional operators. Both types of operators should examine the current market landscape and trends, assess their existing business and strategies, and make necessary adjustments to maintain competitiveness.

New technology standards and operator connectivity strategies are making satellite IoT more reliable and cost-effective. Adopters should understand these standards and strategies, evaluate IoT deployment solutions, especially in remote areas.

Current Status of Satellite IoT Development

According to the latest data from the “2025-2030 Satellite IoT Market Report” (June 2025 edition) published by IoT Insights, the number of global satellite IoT connections is expected to reach 7.5 million in 2024, accounting for only 0.04% of the total 18.8 billion IoT connections worldwide in 2024, and only 0.17% of cellular IoT connections. The core difference lies in the average revenue per user (ARPU): satellite IoT services provided by traditional operators typically charge a monthly fee of $40-70 per device, with an ARPU value reaching 15 times that of cellular IoT, fully reflecting the high quality and special application advantages of satellite connectivity services. In 2024, satellite IoT is expected to account for 3.8% of the revenue from cellular IoT, and this proportion is expected to rise in the future.

Technological innovations and the introduction of standardized protocols such as 3GPP Non-Terrestrial Networks (NTN) (which will be elaborated on later) are driving market growth by reducing satellite launch and service costs. This creates opportunities for new satellite network operators to compete alongside traditional service providers, thereby reshaping the competitive landscape of the industry.

Competition

Landscape

Market Fragmentation is Increasing

In 2024, seven major satellite network operators accounted for over 80% of the market share, including:

1. Inmarsat (UK)

2. Iridium (USA)

3. Orbcomm (USA)

4. Globalstar (USA)

5. Eutelsat OneWeb (Europe)

6. Hispasat (Spain)

7. Echostar (USA)

However, IoT Analytics predicts that by 2030, several new companies will enter the TOP 7 list, including Starlink from the USA and Amazon’s Kuiper project. It is expected that in the next decade, the market share of the top seven companies will continue to decline. Meanwhile, dozens of small companies are entering the market, such as Skylo (USA), Sateliot (Spain), and Plan Space (Turkey).

The race for global coverage and seamless service has already begun. In November 2024, the “Industrial IoT Status Report” released by the American satellite network operator Viasat indicated that 85% of surveyed companies faced challenges in advancing IoT solutions due to network connectivity issues in their target deployment areas.

IoT Analytics research found that satellite IoT operators are competing by deploying larger constellations to minimize coverage gaps and shorten satellite revisit cycles, thereby providing more reliable all-weather connectivity services. This competition is reshaping customer preferences—companies are increasingly inclined to choose suppliers that can provide stable, high-quality data transmission and are more willing to turn to operators that can effectively solve connectivity issues. This trend will drive dynamic changes in market leadership after 2025.

Competition

Landscape

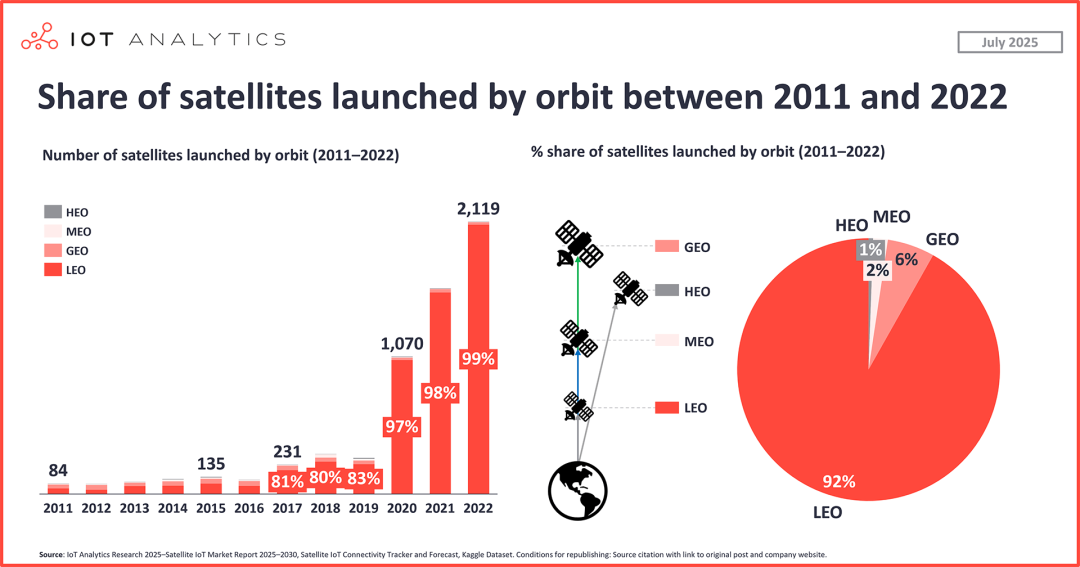

Low Earth Orbit (LEO) Satellite Constellations Become the Preferred Choice for IoT Operators

Nearly two-thirds of satellite IoT operators are opting for Low Earth Orbit (LEO) solutions. The report shows that 92% of satellites launched since 2011 are deployed in LEO orbit. By 2024, 63% of satellite IoT operators have deployed constellation systems in this orbit. These satellites operate at altitudes below 2000 kilometers, which have significant advantages in IoT applications compared to Geostationary Orbit (GEO) and Medium Earth Orbit (MEO) satellites. A key advantage is low latency—i.e., the short time it takes for data to travel to and from the satellite, which is crucial for real-time IoT applications such as asset tracking and remote monitoring.

In addition to connectivity advantages, LEO constellations are also more competitive in manufacturing and launch costs. For example, the UK satellite operator OneWeb achieves cost reduction by standardizing mass production, producing two lightweight satellites (147 kg) daily, and simplifying design and production scaling. Similarly, the American space exploration company SpaceX has reduced launch costs to below $3,500 per kilogram using reusable Falcon 9 rockets.

Competition

Landscape

Traditional Satellite Communication Operators Adopt a Hybrid Strategy to Strengthen Their Position

With the rise of new companies, traditional operators are accelerating strategic adjustments. Traditional satellite network operators, represented by Viasat and Iridium, have long dominated the satellite IoT market landscape. As disruptors like Starlink achieve success, traditional satellite network operators, especially those primarily operating medium and high orbit satellites (such as Luxembourg’s SES and France’s Eutelsat), have begun to comprehensively adjust their connectivity strategies to meet emerging demands, explore new revenue sources, and maintain market dominance. Currently, the industry has formed two major transformation paths: multi-orbit strategy and hybrid networking strategy.

“The current communication industry is undergoing a rapid transformation: well-funded market disruptors and new players are entering, new technologies are emerging to enhance spectrum capacity and efficiency, customer demand for global seamless coverage is rising, and the continuous integration of the communication ecosystem is making industry competition unprecedentedly fierce.” — Nancy Eskenazi, Senior Vice President of Global Legal and Regulatory Affairs at SES, pointed out in December 2024.

Competition

Landscape

Multi-Orbit System Integration Strategy

The multi-orbit constellation strategy helps traditional operators expand their service landscape.Currently, most traditional satellite network operators are laying out multi-orbit strategies through cooperation and acquisitions, aiming to integrate the advantages of various orbits and compensate for the limitations of a single orbit, thereby providing a more comprehensive service portfolio. For example:LEO satellites, while having low latency and cost advantages, can only cover about5% of the Earth’s surface per satellite per pass due to their near-Earth operating characteristics; whileGEO satellites can cover about35% of the Earth’s surface, they have higher signal latency.

By coordinating multi-orbit networks, satellite operators can provide diversified connectivity services to fully meet various IoT application needs, offering millisecond-level low-latency communication for scenarios such as real-time asset tracking; ensuring wide-area coverage in remote areas (where coverage range is prioritized over transmission latency or throughput); and enabling intelligent complementarity betweenLEO and highGEO satellites, automatically switching toGEO satellite backup links when coverage gaps occur withLEO satellites, achieving seamless service continuity.

The report shows that the acquisition of American peer Intelsat by Luxembourg satellite operator SES (completed in July 2025) is a typical practice of the multi-orbit strategy—through this acquisition, SES successfully integrated itsMEO constellation withIntelsat‘sGEO satellite system. Notably, prior to this acquisition, Intelsat had reached a strategic cooperation agreement with the French satellite operator Eutelsat Group regarding theOneWeb LEO constellation, while Eutelsat itself completed the merger with the UK’s OneWeb in September 2023, forming the Eutelsat OneWeb joint operating entity, aiming to build a global coverage network for the collaborative operation ofGEO andLEO constellations.

In 2024, the group of operators adopting or planning to implement multi-orbit strategies accounted for50% of the satellite IoT connection market share.

Competition

Landscape

Hybrid Networking Strategy

The hybrid networking strategy achieves seamless integration of terrestrial and satellite networks. Traditional satellite operators are actively collaborating with mobile network operators (MNOs) to build integrated hybrid networks. This model not only expands the service range for both parties but also significantly enhances network coverage capability and reliability. Typical application scenarios include: asset tracking devices equipped with both cellular IoT and satellite IoT dual modules can automatically switch to satellite links to ensure continuous data transmission when entering cellular network coverage blind spots.

In November 2023, Luxembourg satellite operator OQ Technology signed a memorandum of cooperation with German mobile network operator o2 Telefónica—OQ will provide a satellite network based onLEO narrowband IoT (NB-IoT), while o2 will contribute its cellular infrastructure andKite IoT platform to jointly build a globalNB-IoT connectivity system with seamless terrestrial and satellite network integration. Similarly, the American Viasat is collaborating with the Indian Ministry of Transport to launch India’s first direct device (D2D) satellite service for the state-owned operator BSNL. This service, based on the3GPP Release 17 standard, provides satellite connectivity capabilities for terminals such as smartphones, smartwatches, vehicles, and industrial equipment without the need for dedicated devices.

Analyst Insights: Survival of the Fittest, Industry Restructuring Ahead

Chief Analyst of IoT Analytics, Satyajit Sinha, pointed out:“Traditional giants likeIridium andInmarsat will not collapse overnight; their sustained market value stems from their proven evolutionary capabilities. However, for all practitioners—especially new operators—adapting to the new market reality has become a survival imperative: collaboration amongLEO constellations, cloud-native operations, and flexible pricing models have become essential options. AsStarlink is set to deploy over7,000 LEO satellites for commercial use by mid-2025, the price competition mechanism in the satellite market will completely reshape the industry competitive landscape before 2030.”

Click to read the original article: Satellite IoT competitive landscape: notable insights

★