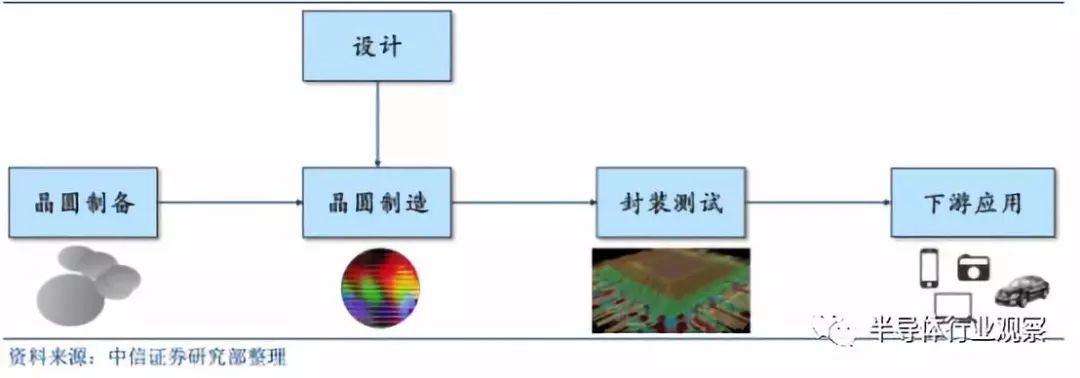

Wafers are the fundamental raw materials for manufacturing semiconductor devices. High-purity semiconductors are prepared into wafers through processes such as crystal pulling and slicing. These wafers undergo a series of semiconductor manufacturing processes to form extremely tiny circuit structures, which are then cut, packaged, and tested to become chips, widely used in various electronic devices. The materials for wafers have evolved over more than 60 years of technological advancement and industrial development, resulting in today’s industry landscape dominated by silicon, with new semiconductor materials as supplements.

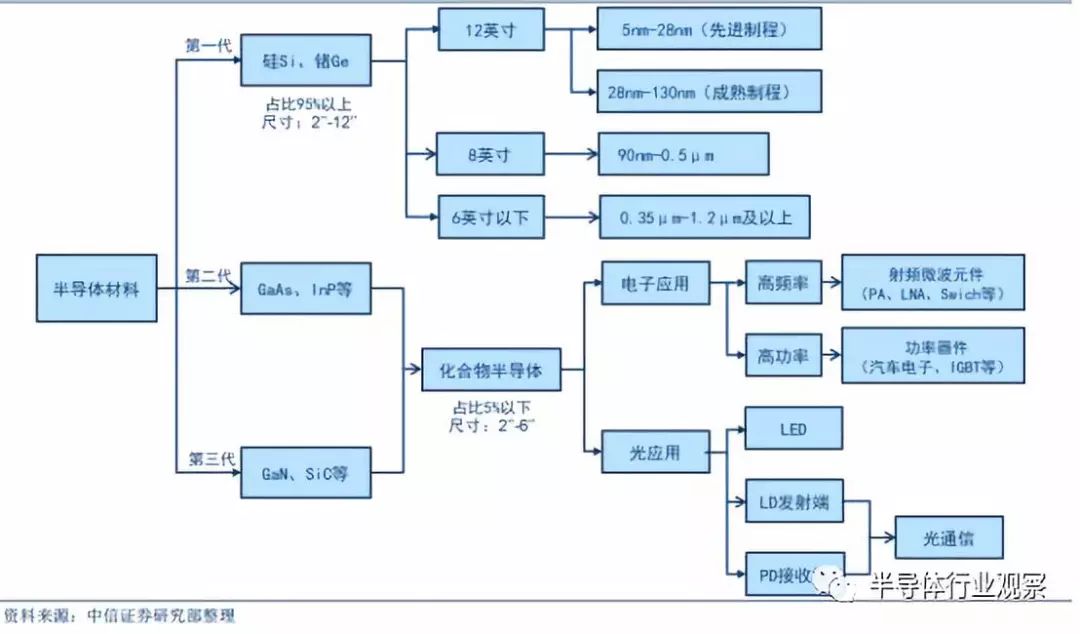

Basic Framework of Semiconductor Wafer Materials

In the 1950s, germanium (Ge) was the first semiconductor material used, initially in discrete devices. The advent of integrated circuits was an important step forward for the semiconductor industry. In July 1958, Jack Kilby at Texas Instruments in Dallas manufactured the first integrated circuit using a piece of germanium semiconductor material as the substrate.

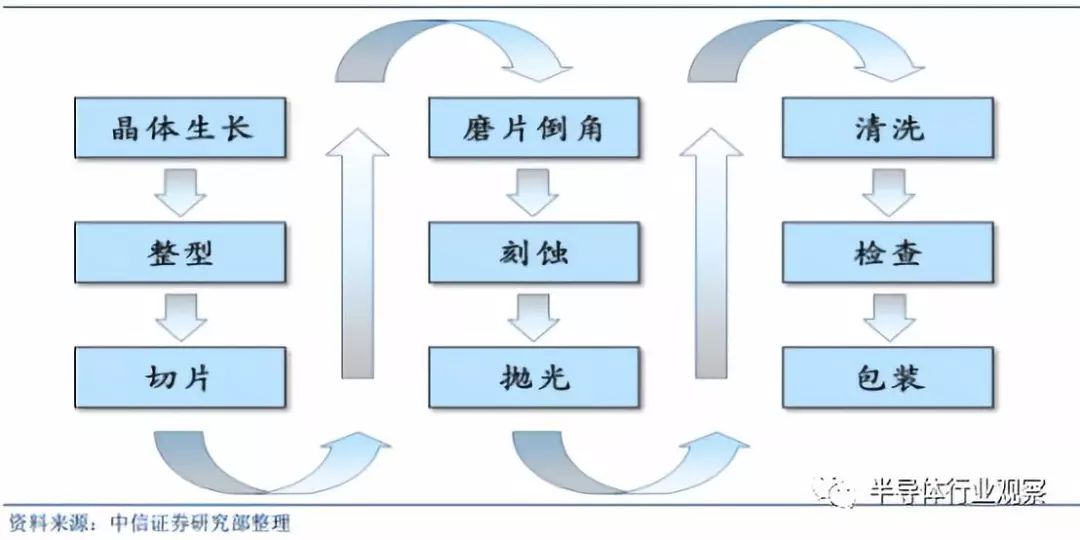

Semiconductor Industry Chain Process

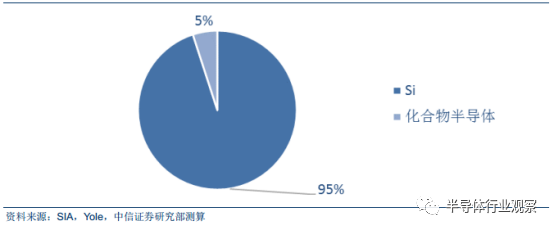

However, germanium devices had shortcomings in high-temperature resistance and radiation resistance, and were gradually replaced by silicon (Si) devices in the late 1960s. Silicon is extremely abundant, with mature purification and crystallization processes, and the silicon dioxide (SiO2) film formed by oxidation has good insulating properties, greatly enhancing the stability and reliability of devices. Therefore, silicon has become the most widely used semiconductor material. In terms of output value, over 95% of semiconductor devices and over 99% of integrated circuits globally use silicon as the substrate material.

In 2017, the global semiconductor market size was approximately $412.2 billion, while the compound semiconductor market size was about $20 billion, accounting for less than 5%. In terms of wafer substrate market size, the annual sales of silicon substrates in 2017 reached $8.7 billion, GaAs substrates about $800 million, GaN substrates around $100 million, and SiC substrates about $300 million. Silicon substrate sales accounted for over 85%. In the 21st century, its dominant and core position remains unchanged. However, the physical properties of Si materials limit their application in optoelectronics and high-frequency, high-power devices.

Semiconductor Market Share by Material

Since the 1990s, second-generation semiconductor materials represented by gallium arsenide (GaAs) and indium phosphide (InP) have begun to emerge. Materials like GaAs and InP are suitable for making high-speed, high-frequency, high-power, and optoelectronic devices, making them excellent materials for high-performance microwave and millimeter-wave devices and light-emitting devices, widely used in satellite communications, mobile communications, optical communications, GPS navigation, and other fields. However, GaAs and InP materials are scarce, expensive, and toxic, which can pollute the environment. InP is even considered a possible carcinogen, which greatly limits the application of second-generation semiconductor materials.

Third-generation semiconductor materials mainly include SiC and GaN, known as wide-bandgap semiconductor materials due to their bandgap width (Eg) being greater than or equal to 2.3 electron volts (eV). Compared to first and second-generation semiconductor materials, third-generation semiconductor materials have advantages such as high thermal conductivity, high breakdown field strength, high saturation electron drift velocity, and high bond energy, meeting modern electronic technology’s new requirements for high temperature, high power, high voltage, high frequency, and radiation resistance. They are the most promising materials in the semiconductor field, with important applications in national defense, aerospace, oil exploration, optical storage, and other fields. They can reduce energy loss by more than 50% in many strategic industries such as broadband communications, solar energy, automotive manufacturing, semiconductor lighting, and smart grids, potentially reducing equipment size by more than 75%, which is of milestone significance for the development of human technology.

Comparison of Wafer Material Properties

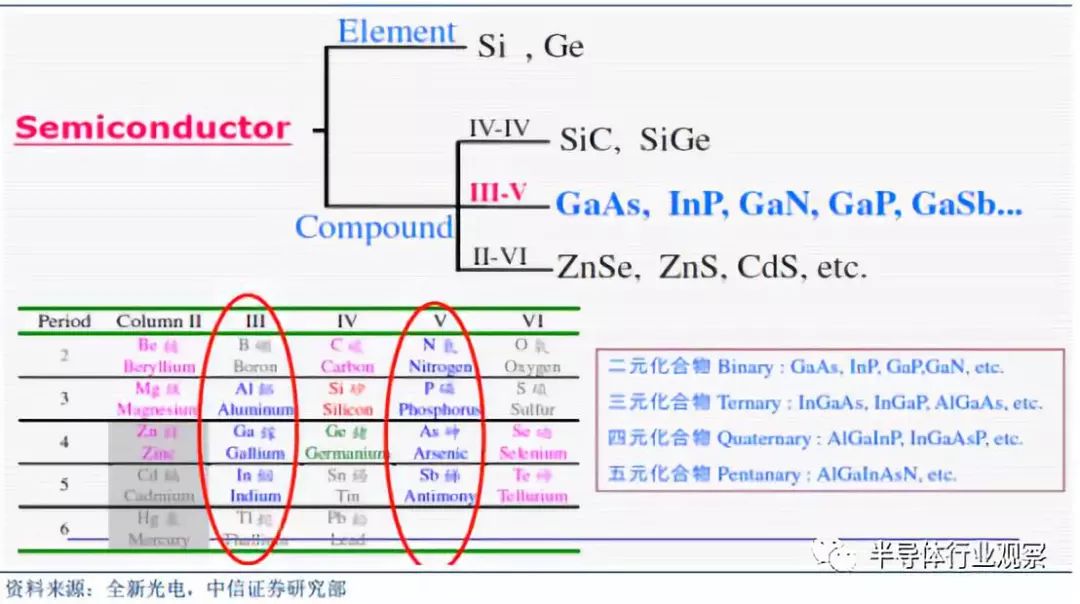

Compound semiconductors refer to semiconductor materials formed by two or more elements. Most second and third-generation semiconductors belong to this category. According to the number of elements, they can be divided into binary compounds, ternary compounds, quaternary compounds, etc. Binary compound semiconductors can be further classified into III-V, IV-IV, II-VI groups based on the positions of their constituent elements in the periodic table. Compound semiconductor materials represented by GaAs, GaN, and SiC have become the fastest developing, most widely used, and largest output semiconductor materials after silicon. Compound semiconductor materials possess superior performance and energy band structures:

(1) High electron mobility;

(2) High-frequency characteristics;

(3) Wide bandwidth;

(4) High linearity;

(5) High power;

(6) Material selection diversity;

(7) Radiation resistance.

Therefore, compound semiconductors are mainly used in the manufacture of RF devices, optoelectronic devices, power devices, etc., with significant development potential; silicon devices are mainly used in logic devices, memory devices, etc., and they are irreplaceable in each other’s applications.

Compound Semiconductor Materials

Wafer Preparation: Substrate and Epitaxy Processes

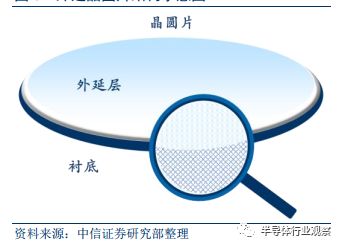

Wafer preparation includes two main steps: substrate preparation and epitaxy processes. A substrate is a wafer made from single-crystal semiconductor material. The substrate can directly enter the wafer manufacturing process to produce semiconductor devices or undergo epitaxy processing to produce epitaxial wafers. Epitaxy refers to the process of growing a new single crystal layer on a single-crystal substrate. The new single crystal can be made from the same material as the substrate or from a different material. Epitaxy allows for the production of a wider variety of materials, providing more choices for device design.

The basic steps of substrate preparation are as follows: semiconductor polycrystalline materials are first purified, doped, and drawn to produce single-crystal materials. Taking silicon as an example, silicon sand is first refined and reduced to metallurgical-grade silicon with a purity of about 98%. After multiple purifications, high-purity polycrystalline silicon (with a purity of over 99.9999999%, 9-11 nines) is obtained, and single-crystal silicon rods are drawn from a furnace. The single-crystal material is then mechanically processed, chemically treated, polished, and quality tested to obtain single-crystal polished wafers that meet certain standards (thickness, crystal orientation, flatness, parallelism, and damage layer). The purpose of polishing is to further remove residual damage layers from the processed surface. The polished wafers can be directly used to make devices or serve as substrate materials for epitaxy.

Basic Steps of Substrate Preparation

The epitaxy growth processes currently mainly include MOCVD (Metal-Organic Chemical Vapor Deposition) technology and MBE (Molecular Beam Epitaxy) technology. For example, New Optoelectronics uses MOCVD, while Epistar uses MBE technology.

Schematic Diagram of Epitaxial Wafer Structure

In comparison, MOCVD technology has a faster growth rate, making it more suitable for large-scale industrial production, while MBE technology is more suitable for certain cases, such as the production of PHEMT structures and Sb compound semiconductors. HVPE (Hydride Vapor Phase Epitaxy) technology is mainly used in GaN substrate production. LPE (Liquid Phase Epitaxy) technology is mainly used for silicon wafers, which have now been largely replaced by vapor deposition technologies.

Comparison of MBE and MOCVD Technologies

Wafer Size: Different Technological Development Processes

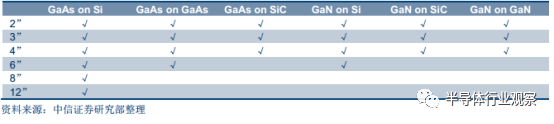

Silicon wafers can reach a maximum size of 12 inches, while compound semiconductor wafer sizes can reach a maximum of 6 inches. The mainstream size of silicon wafer substrates is 12 inches, accounting for about 65% of global silicon wafer production capacity. 8-inch wafers are also commonly used in mature processes, accounting for 25% of global capacity. The mainstream sizes for GaAs substrates are 4 inches and 6 inches; for SiC substrates, the mainstream supply sizes are 2 inches and 4 inches; for GaN self-supporting substrates, 2 inches is the main size.

Corresponding Sizes of Substrate Wafers

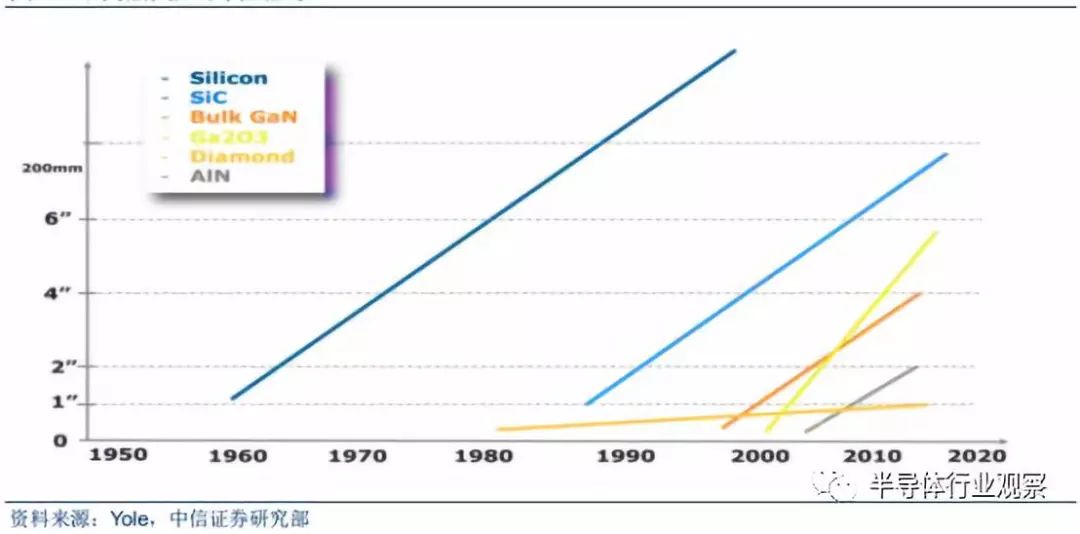

The size of SiC substrates has now reached 6 inches, with 8 inches currently under development (II-VI has already produced samples). However, the mainstream size still remains 4 inches. The main reasons are: (1) Currently, 6-inch SiC wafers are about 2.25 times the cost of 4-inch wafers, and by 2020, it is expected to be about 2 times, showing no significant progress in cost reduction. Additionally, changing equipment requires extra capital expenditure, and the advantage of 6 inches currently lies only in production efficiency; (2) The quality of 6-inch SiC wafers is relatively lower than that of 4-inch wafers, so 6-inch wafers are mainly used to manufacture diodes, as it is simpler to produce diodes on lower quality wafers than on MOSFETs.

Corresponding Wafer Sizes for Epitaxial Growth

GaN materials lack single-crystal materials in nature, hence epitaxy is conducted on heterogeneous substrates such as sapphire, SiC, and Si. Currently, through hydride vapor phase epitaxy (HVPE) and ammonothermal methods, 2-inch, 3-inch, and 4-inch GaN self-supporting substrates can be produced. In commercial applications, GaN epitaxy on heterogeneous substrates remains predominant, while GaN self-supporting substrates have the greatest application in lasers, achieving higher luminous efficiency and quality.

Different Wafer Size Development History

Silicon: Mainstream Market, Strong Demand in Segmented Fields

From the perspective of silicon wafer supply vendors, Japanese companies dominate, maintaining a stable oligopoly. Japanese manufacturers hold over 50% of the silicon wafer market share. The top five manufacturers account for over 90% of the global market. Among them, Shin-Etsu Chemical from Japan accounts for 27%, SUMCO from Japan accounts for 26%, and the two Japanese companies combined account for 53%, more than half. Taiwan’s GlobalWafers acquired American SunEdison Semiconductor during the downturn of the wafer industry in December 2016, rising from sixth to third place with a share of 17%. Germany’s Siltronic holds a share of 13%, while Korea’s SK Siltron (formerly LG Siltron, acquired by SK Group in 2017) holds a share of 9%. Unlike the top four manufacturers, SK Siltron only supplies Korean customers.

Additionally, there are smaller companies such as France’s Soitec, Taiwan’s Taisil, Hejing, and Jiajing. The major manufacturers differ in the types and sizes of wafers they supply. Overall, the top three manufacturers offer a diverse range of products. The top three manufacturers can supply Si annealing wafers and SOI wafers, with only Shin-Etsu from Japan able to supply 12-inch SOI wafers. Germany’s Siltronic and Korea’s SK Siltron do not provide SOI wafers, and SK Siltron does not supply Si annealing wafers. However, there is basically no difference in sizes of Si polished wafers and Si epitaxial wafers among manufacturers.

Competitiveness of Silicon Wafer Suppliers

For the past 15 years, Japanese manufacturers have consistently held over 50% of the silicon wafer market share. There has been no significant regional transfer of silicon wafer production capacity. According to Gartner, in 2007, the top three companies in silicon wafer market share were Japan’s Shin-Etsu (32.5%), Japan’s SUMCO (21.7%), and Germany’s Siltronic (14.8%); in 2002, the top three were Japan’s Shin-Etsu (28.9%), Japan’s SUMCO (23.3%), and Germany’s Siltronic (15.4%). A significant recent market change was Taiwan’s GlobalWafers acquiring American SunEdison, rising from the sixth to the third largest manufacturer. However, Japanese manufacturers have consistently maintained over 50% market share.

Japan’s competitiveness in the fab segment has declined, while it continues to maintain a leading position in the materials segment. In the mid-1980s, Japan’s semiconductor industry held over 50% of the world’s market share. Japan’s advantage in semiconductor materials has continued since the last century, while its competitiveness in wafer manufacturing has significantly weakened, with a clear regional transfer occurring in the semiconductor fab segment. The reasons are that the fab segment is closer to the demand side and experiences greater market fluctuations; however, silicon wafers are highly homogeneous, and new entrants need a considerable amount of time to validate their products with customers; moreover, wafers account for less than 10% of the cost in wafer foundries, making foundries reluctant to risk switching to immature products for minor price differences.

Changes in Market Share of Silicon Wafer Suppliers Over the Past 15 Years

Silicon Wafer Demand Vendor Landscape: Dominated by Foreign Firms, Domestic Firms Show Promise

In IC design, major players dominate the market with high barriers to entry, and since 2018, AI chips have become a new growth driver. Qualcomm, Broadcom, MediaTek, Apple, and other manufacturers are the strongest, while China’s HiSilicon has emerged. As technology advances, leading to upgrades in terminal products, the demand for IC products for innovative applications such as AI chips continues to expand. It is expected that by 2020, the AI chip market size will grow from about $600 million in 2016 to $2.6 billion, with a CAGR of 43.9%. Currently, both domestic and foreign IC design firms are actively laying out the AI chip industry. NVIDIA is the leader in the AI chip market, while AMD and Tesla are jointly developing AI chips for autonomous driving.

For domestic firms, Huawei’s HiSilicon was the first to launch the Kirin 970 AI chip in September 2017, which has successfully been integrated into models like the P20; Bitmain’s BM1680, the world’s first tensor acceleration computing chip, has been successfully used in Bitcoin mining machines; and Cambrian’s 1A processor, Horizon’s Journey and Sunrise processors have also emerged. IC design must be market-oriented to better serve downstream customers. Mobile processing chip and baseband chip manufacturers like HiSilicon and Spreadtrum have rapidly risen to the top ten global IC design firms due to the explosive growth of the Chinese smartphone market in recent years. HiSilicon chips have been fully integrated into Huawei smartphones, and companies like Samsung and Xiaomi have also adopted self-developed chips. Today, China is the largest terminal demand market globally, giving domestic IC design firms a significant development advantage.

Global IC Design Firms Ranking in 2017

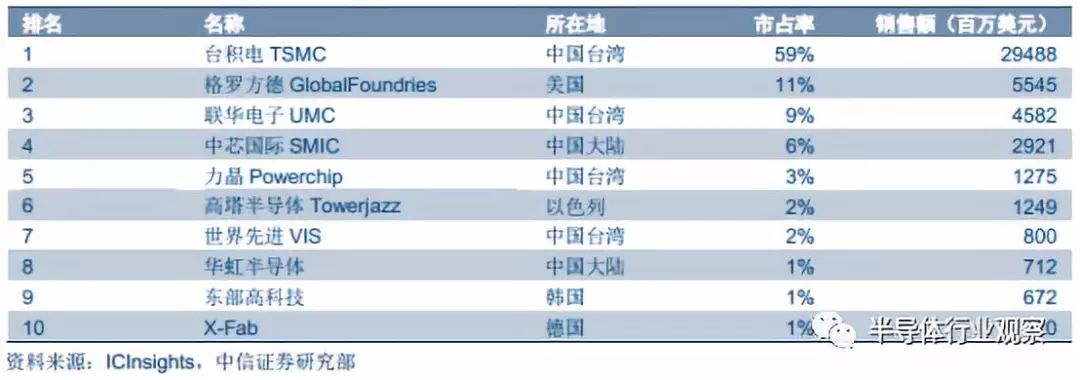

In terms of foundry manufacturing, Capex of manufacturers is growing rapidly, led by giants like Samsung and TSMC. In terms of capital expenditure, the competition in the global advanced process chip market is fierce, with the top three chip manufacturers—Samsung, Intel, and TSMC—each having Capex reaching the level of $10 billion, with 2017 figures being $44 billion, $12 billion, and $10.8 billion respectively. It is expected that Samsung’s total Capex in the next three years will approach $110 billion, while Intel and TSMC’s Capex in 2018 is expected to reach $14 billion and $12 billion respectively, both showing significant growth, benefiting giants in capturing the market through the development of advanced process technologies and the expansion of production lines.

From a process perspective, TSMC is leading the industry, currently producing 10nm process chips on a large scale, with 7nm process expected to go into mass production in 2018; China’s leading foundry, SMIC, currently has the capability for 28nm process mass production, while TSMC had already achieved 28nm mass production capability as early as 2011, indicating a significant gap between mainland manufacturers.

Global Pure-Play Foundry Manufacturers Ranking in 2016

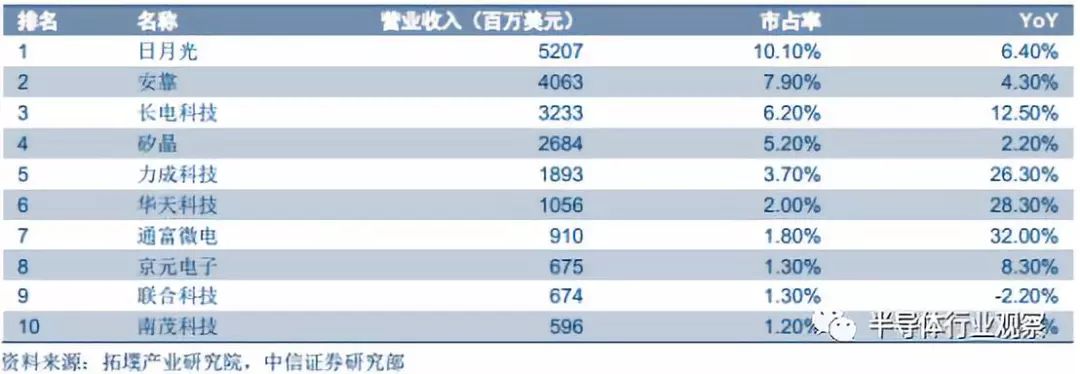

In packaging and testing, the trend of high-end manufacturing and packaging integration is becoming apparent, with the technology gap between mainland manufacturers and Taiwanese manufacturers narrowing. Packaging and testing technology has developed through four generations, with the highest-end technology achieving integration between manufacturing and packaging. TSMC has established two major advanced packaging ecosystems—CoWoS and InFO—and plans to double InFO production capacity to meet the demand for Apple’s A12 chip.

Leading packaging and testing company ASE Technology Holding has mastered top-tier packaging and microelectronics manufacturing technologies, being the first to mass-produce TSV/2.5D/3D related products. In March 2018, ASE established a joint venture with Japan’s TDK to expand its SiP layout. Due to the relatively low technical barriers in packaging technology, mainland manufacturers are rapidly catching up, and the technology gap with global leaders is gradually narrowing. Mainland manufacturers have largely mastered advanced technologies such as SiP, WLCSP, and FOWLP, with applications in FC, SiP, and other packaging technologies already in mass production.

Global Semiconductor Packaging Manufacturers Ranking in 2017

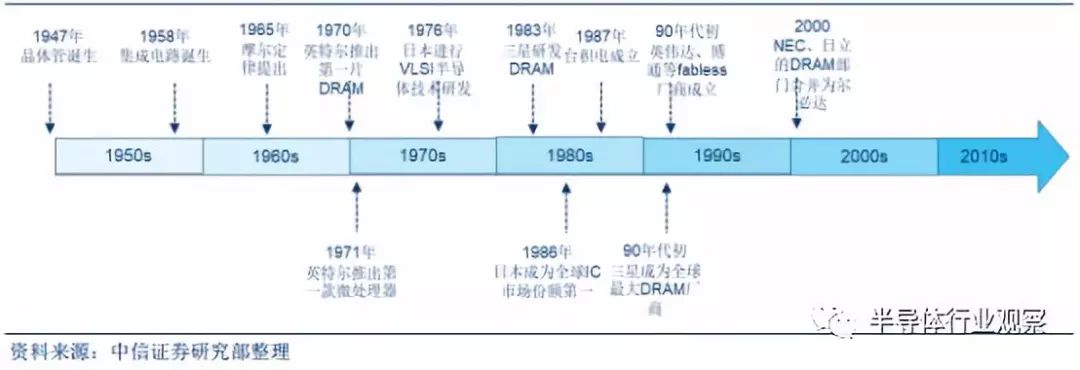

A new round of regional transfer is oriented towards mainland China. Although the top firms in IC design, manufacturing, and packaging are mainly located in the United States and Taiwan, the semiconductor manufacturing industry has experienced a development history from the United States to Japan to Korea and Taiwan: In the 1950s, the semiconductor industry originated in the United States, with the invention of the transistor in 1947 and the integrated circuit in 1958. In the 1970s, semiconductor manufacturing shifted from the United States to Japan, with DRAM being an important entry point for the industrial development of Japan, which had led the semiconductor industry in the 1980s. In the 1990s, the industry shifted to Korean firms like Samsung and Hynix, while the wafer foundry segment shifted to Taiwan, with TSMC and UMC rising. In the 2010s, the explosion of smartphones and mobile internet, along with the rapid growth of IoT, big data, cloud computing, and artificial intelligence industries, have made China a new destination for regional transfer due to its demographic dividend and shifting demand.

Historical Regional Transfer of the Global Semiconductor Industry: US-Japan-Korea

Silicon Wafer Downstream Application Breakdown: Size and Process Drive Technological Progress

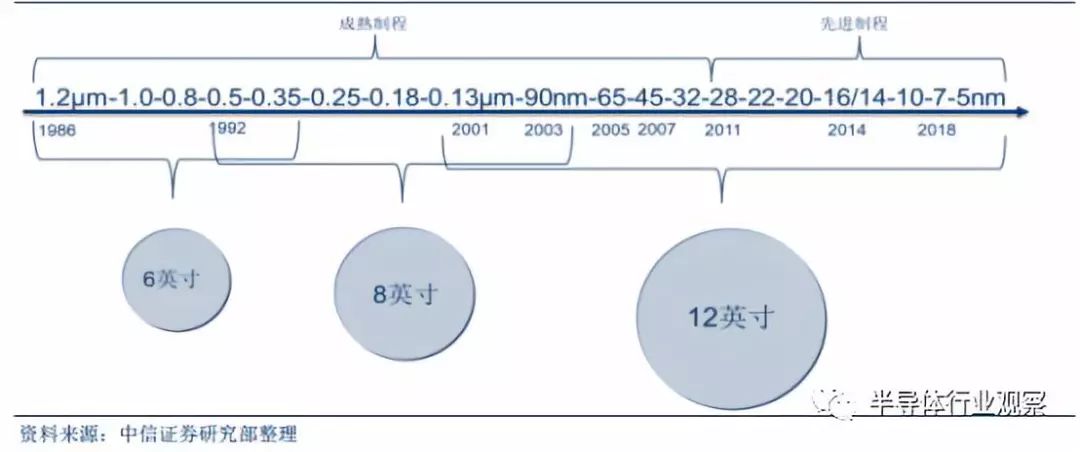

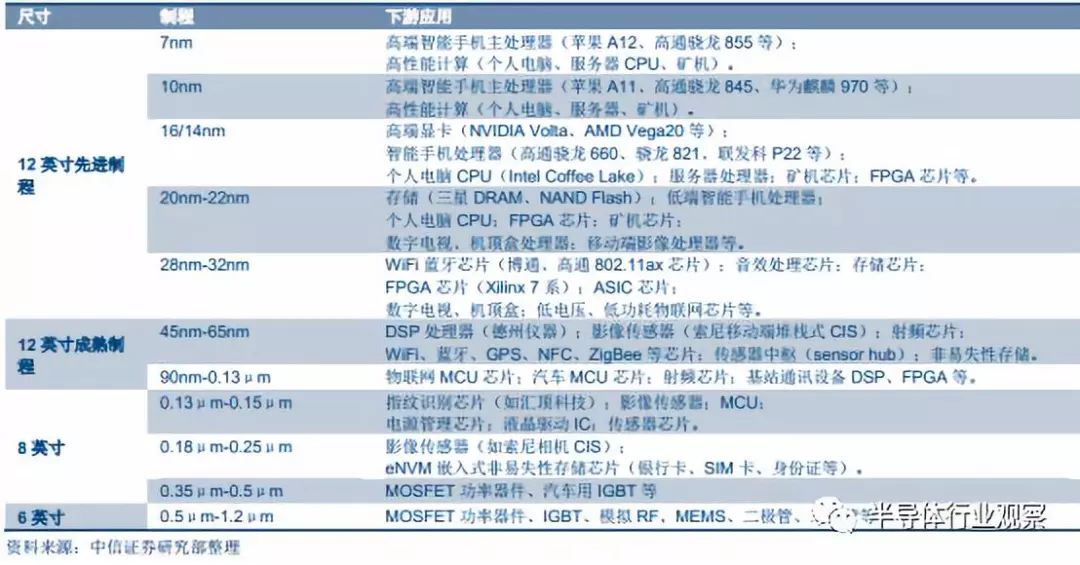

Wafer size and process technology develop in parallel, with each process stage corresponding to wafer sizes. (1) Process progress → transistor miniaturization → increased transistor density → performance enhancement. (2) Increasing wafer size → more chips produced per wafer → efficiency improvement → cost reduction. Currently, production equipment for 6-inch and 8-inch silicon wafers has generally depreciated, leading to lower production costs, primarily producing mature processes above 90nm. Some processes yield products on wafers of adjacent sizes. 5nm to 0.13μm processes use 12-inch wafers, with 28nm serving as a boundary that distinguishes advanced processes from mature processes, mainly because new designs and processes such as FinFET are introduced after 28nm, greatly increasing the difficulty of wafer manufacturing.

Silicon Wafer Size Correspondence

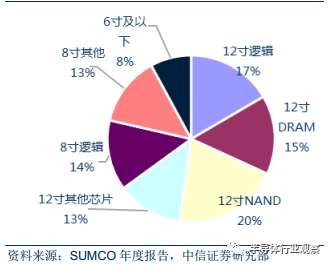

In terms of total wafer demand, the 12-inch NAND and 8-inch markets are the core driving forces. The share of 12-inch silicon wafers for storage reaches 35%, making it the largest, followed by 8-inch and 12-inch logic. In terms of sales revenue, among global integrated circuit products, memory accounts for about 27.8%, logic circuits account for 33%, and microprocessor chips and analog circuits account for 21.9% and 17.3%, respectively. According to our predictions, the global demand for 12-inch silicon wafers in the second half of 2016 was approximately 5.1 million pieces per month, with demand for logic chips at 1.3 million pieces per month, DRAM demand at 1.2 million pieces per month, NAND demand at 1.6 million pieces per month, and other demands including NOR Flash, CIS, etc., at 1 million pieces per month; demand for 8-inch silicon wafers was 4.8 million pieces per month, which, when converted to 12-inch wafers by area, is approximately 2.13 million pieces per month, while demand for wafers below 6 inches is approximately equivalent to 12-inch wafers at 620,000 pieces per month.

Demand Structure for 12-inch, 8-inch, and 6-inch Wafers

Estimating from this, the demand for 12-inch wafers for storage, including NAND and DRAM, accounts for about 35% of total demand, while 8-inch wafer demand accounts for about 27%, and demand for 12-inch wafers for logic chips accounts for about 17%. In terms of demand, memory currently contributes the most to wafer demand, followed by 8-inch mid-to-low-end applications.

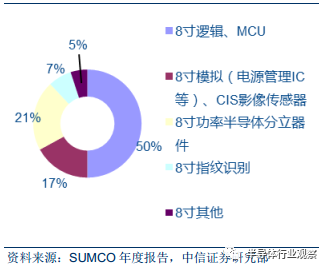

8-inch Wafer Demand Structure

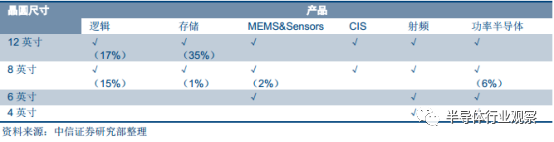

Wafer Size Correspondence with Product Types

Looking at downstream specific applications, 12-inch wafers with advanced processes below 20nm have strong performance and are mainly used in mobile devices and high-performance computing fields, including main chips for smartphones, computer CPUs, GPUs, high-performance FPGAs, ASICs, etc. 14nm-32nm advanced processes are used for DRAM, NAND Flash storage chips, mid-to-low-end processor chips, image processors, digital TV set-top boxes, and other applications. The mature processes of 12-inch wafers ranging from 45-90nm are mainly used in fields with slightly lower performance requirements but high cost and production efficiency demands, such as mobile basebands, WiFi, GPS, Bluetooth, NFC, ZigBee, NOR Flash chips, MCUs, etc. 12-inch or 8-inch wafers with 90nm to 0.15μm are mainly used for MCUs, fingerprint recognition chips, image sensors, power management chips, LCD driver ICs, etc. 8-inch wafers with 0.18μm-0.25μm are mainly used for non-volatile storage such as bank cards and SIM cards, while those above 0.35μm are mainly for power devices such as MOSFETs and IGBTs.

Process-Size Correspondence for Downstream Application Demand Breakdown

Compound Semiconductors: Key Materials for 5G, 3D Sensing, and Electric Vehicles

The landscape of compound semiconductor wafer supply vendors is dominated by Japan, the US, and Germany, forming an oligopoly.

In the substrate market, high technical barriers have led to an oligopoly in the compound semiconductor substrate market, dominated by manufacturers from Japan, the US, and Germany. Currently, the GaAs substrate market is occupied by four companies: Japan’s Sumitomo Electric, Germany’s Freiberg, America’s AXT, and Japan’s Sumitomo Chemical, with these four companies holding over 90% of the market share. Sumitomo Chemical acquired Hitachi Cable’s (Hitachi Metals) compound semiconductor business in 2011 and transferred it to its subsidiary Sciocs in 2016. The self-supporting GaN substrates are primarily monopolized by three Japanese companies: Sumitomo Electric, Mitsubishi Chemical, and Sumitomo Chemical, with a combined share exceeding 85%. The leading SiC substrate manufacturer is America’s Cree (Wolfspeed division), which holds over one-third of the market share, followed by Germany’s SiCrystal, America’s II-VI, and America’s Dow Corning, with these four companies holding over 90% of the market share. In recent years, China has also seen the emergence of SiC substrate manufacturers with certain production capabilities, such as Beijing Tianke Heda Semiconductor Co., Ltd.

Competitiveness of Compound Semiconductor Suppliers

In the epitaxy growth market, UK-based IQE holds over 60% market share, being the absolute leader. IQE and Taiwan’s New Optoelectronics together account for 80% of the market. Epitaxy growth mainly includes the MOCVD (Metal-Organic Chemical Vapor Deposition) technology and MBE (Molecular Beam Epitaxy) technology. For instance, both IQE and New Optoelectronics utilize MOCVD, while Epistar employs MBE technology. HVPE (Hydride Vapor Phase Epitaxy) technology is mainly used for the production of GaN substrates.

Competitiveness of Compound Semiconductor Epitaxy Suppliers

Demand Vendor Landscape for Compound Semiconductor Wafers: Coexistence of IDM and Foundry Giants

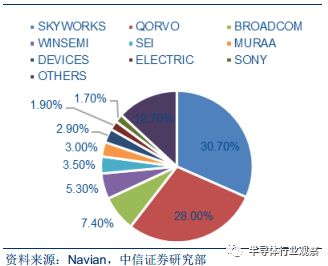

The compound semiconductor industry chain exhibits an oligopolistic competitive structure. IDM manufacturers include Skyworks, Broadcom (Avago), Qorvo, Anadigics, and others. In 2016, the global compound semiconductor IDM market was characterized by three major players, with Skyworks, Qorvo, and Broadcom occupying 30.7%, 28%, and 7.4% market shares in the GaAs sector, respectively. The industry chain shows a trend of multi-model integration, with design companies moving away from wafer production and IDM capacity outsourcing becoming an inevitable trend.

Global GaAs Device (Including IDM) Market Value Distribution

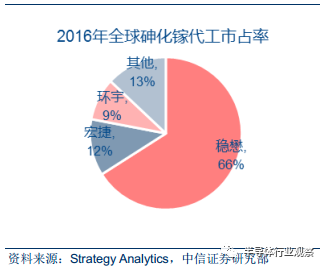

The compound semiconductor wafer foundry field is led by Win Semiconductors, which holds a 66% market share, making it the absolute leader. The second and third places are occupied by Advanced Wireless Semiconductor Company (AWSC) and Global Communication Semiconductor (GCS), with shares of 12% and 9%, respectively. Domestic design pushes for foundry, and a leading compound semiconductor foundry from mainland China is emerging. Currently, domestic PA design has seen companies like RDA, Vanchip, Han Tianxia, and Feixiang Technology come to the forefront.

Global GaAs Foundry Market Share

Domestic compound semiconductor design firms have currently captured low-end applications in consumer electronics markets such as 2G, 3G, 4G, and WiFi. Sanan Optoelectronics mainly focuses on LED applications and is expected to fill the domestic gap in compound semiconductor foundry. Its fundraising and production line construction are progressing smoothly, and it is expected to achieve a capacity of 4,000-6,000 pieces per month by the end of 2018, becoming the first large-scale GaAs/GaN compound wafer foundry enterprise in mainland China.

Downstream Applications of Compound Semiconductor Wafers: Unique Performance, Self-Contained System

Downstream specific applications of compound semiconductors can be divided into two main categories: optical devices and electronic devices. Optical devices include LED light-emitting diodes, LD laser diodes, PD photodetectors, etc. Electronic devices include PA power amplifiers, LNA low-noise amplifiers, RF switches, analog-to-digital converters, microwave integrated circuits, power semiconductor devices, Hall elements, etc. For GaAs materials, SC GaAs (single crystal gallium arsenide) is mainly used in optical devices, while SI GaAs (semi-insulating gallium arsenide) is primarily used in electronic devices.

Compound Semiconductor Wafers Corresponding Downstream Applications

In optical devices, LEDs account for the largest share, while LD/PD and VCSEL have significant growth potential. Cree derives about 70% of its revenue from LEDs, with the remainder coming from power, RF, and SiC wafers. SiC substrates account for 80% of the market for diodes. Among all wide-bandgap semiconductor substrates, SiC materials are the most mature. Different LED materials made from compound semiconductors correspond to different wavelengths of light: GaAs LEDs emit red and green light, GaP emits green light, SiC emits yellow light, and GaN emits blue light. The application of GaN blue LEDs to excite yellow phosphor materials can produce white light LEDs. Additionally, GaAs can produce infrared LEDs, commonly used in remote control infrared emitters, while GaN can produce ultraviolet LEDs. GaAs and GaN can produce red and blue laser emitters, respectively, which can be used for reading CDs, DVDs, and Blu-ray discs.

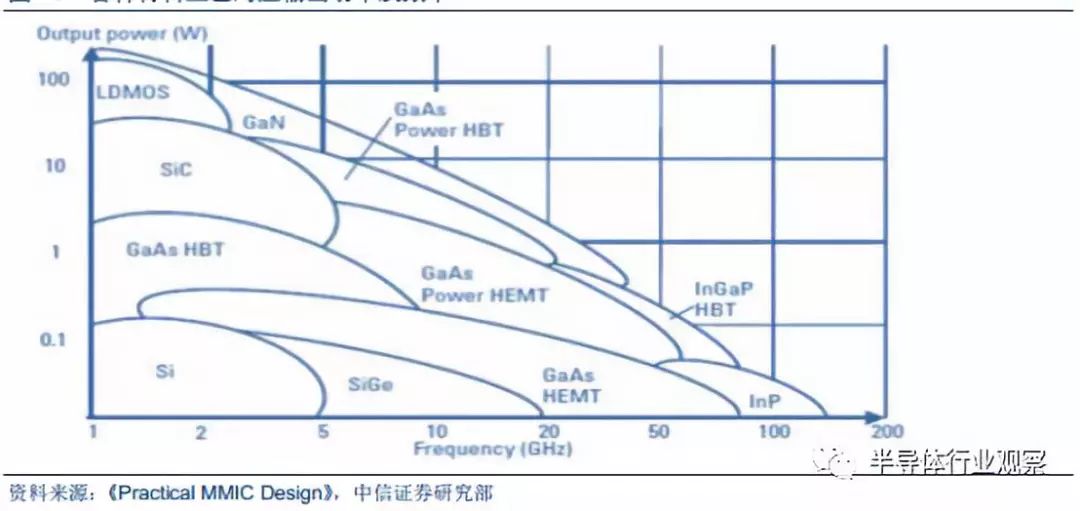

Output Power and Frequency Corresponding to Various Material Processes

In electronic devices, the primary applications are RF and power applications. GaN on SiC, self-supporting GaN substrates, GaAs substrates, and GaAs on Si are mainly used in RF semiconductors (such as RF front-end PAs); while GaN on Si and SiC substrates are mainly used in power semiconductors (such as automotive electronics).

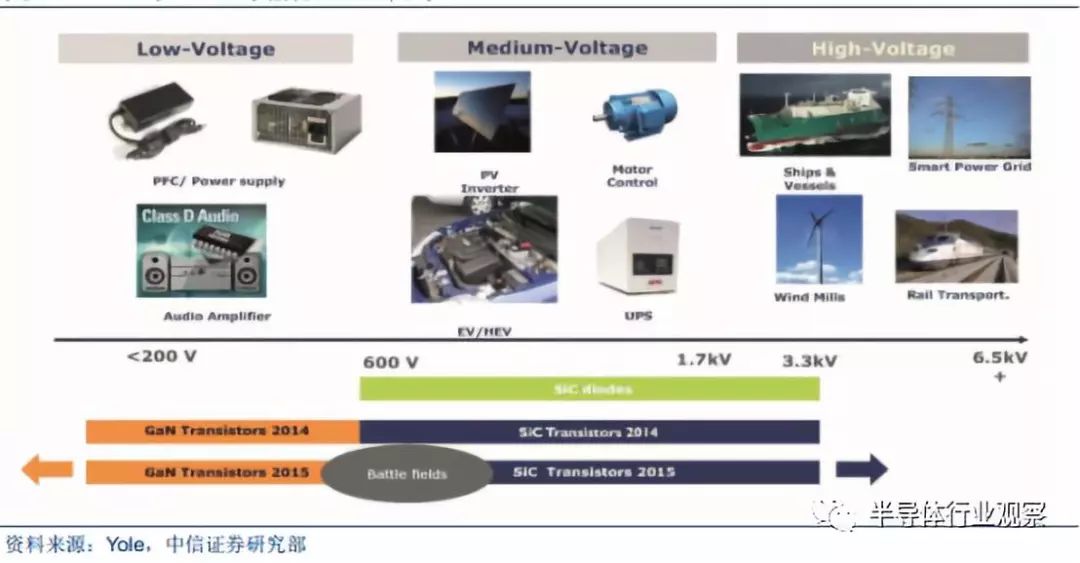

Comparison of GaN and SiC Power Device Application Scope

Due to its high power density, GaN has unique advantages in high-power devices for base stations. Compared to silicon substrates, SiC substrates offer better thermal conductivity. Currently, over 95% of GaN RF devices use SiC substrates, such as those used by Qorvo, which are based on SiC substrate processes. Silicon-based GaN devices can be manufactured on 8-inch wafers, providing greater cost advantages. In the power semiconductor field, SiC substrates and GaN on Silicon only compete in a few small areas. The GaN market is mostly in low-voltage areas, while SiC is applied in high-voltage areas. Their boundary is approximately 600V.

Downstream Major Application Analysis: Examining Chip Localization from Process Materials

(1) Smartphones: IC design is catching up first, while foundry and materials still need breakthroughs.

The core chips of smartphones involve advanced processes and compound semiconductor materials, with a low localization rate. Taking Huawei smartphones, which currently use a relatively high number of domestically produced chips, as an example, we can see the “ceiling” of domestic chips.

Internal Chip Correspondence of Smartphones – Huawei P20

Currently, Huawei’s HiSilicon can independently design CPUs, and there are also fabless design companies like Xiaomi’s Pinecone. However, due to the use of the most advanced 12-inch processes, manufacturing mainly relies on Taiwanese companies; there are currently no domestic companies mass-producing DRAM or NAND flash memory; the front-end LTE modules and WiFi and Bluetooth modules use GaAs materials, with production concentrated in American IDM companies like Skyworks and Qorvo, as well as Taiwanese foundries like Win Semiconductors. There are currently no GaAs foundry manufacturers in mainland China; RF transceiver modules, PMICs, and audio ICs can be designed by HiSilicon and foundry manufactured, while charging control ICs, NFC control ICs, and sensors like pressure and gyroscopes are mainly provided by European and American IDM manufacturers. Overall, the localization rate of core chips in smartphones remains low, with some chips like DRAM, NAND, and RF modules having almost zero localization.

Taking the mainstream flagship smartphone iPhone X as an example, we can see the position of mainland Chinese chip manufacturers in the global supply chain. The CPU uses Apple’s self-designed chip manufactured by TSMC using advanced processes, while DRAM and NAND come from IDM manufacturers in Korea, Japan, and the US; the baseband is designed by Qualcomm and manufactured by TSMC using advanced processes; the RF module uses GaAs materials from IDM companies like Skyworks, Qorvo, or Broadcom + Win Semiconductors; analog chips, audio ICs, NFC chips, touch ICs, image sensors, etc., are all sourced from companies outside mainland China. The share of mainland Chinese chips in Apple’s supply chain is zero. However, most components other than chips and screens have suppliers from mainland China, with some even being exclusively supplied by mainland manufacturers. This shows that the competitiveness of mainland Chinese chip companies on a global scale remains low.

Internal Chip Correspondence of Smartphones – iPhone X

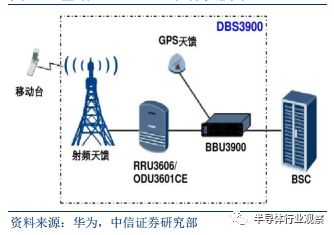

(2) Communication Base Stations: High Dependency on US Chips for High-Power RF Chips

Communication base stations have a very high dependency on foreign chips, primarily from American chip companies. Currently, base station systems mainly consist of baseband processing units (BBUs) and remote radio units (RRUs), with one BBU typically corresponding to multiple RRU devices. In comparison, the localization rate of RRU chips is even lower, leading to a high dependency on foreign suppliers.

BBU + RRU System Schematic

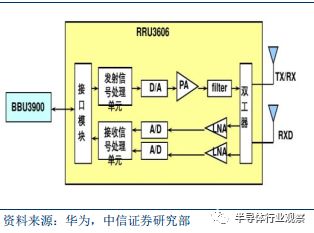

The main difficulties lie in that RRU chip devices involve high-power RF scenarios, usually using GaAs or GaN materials, while mainland China lacks the corresponding industrial chain.

RRU Internal Chips Have the Highest Barriers

American firms monopolize high-power RF devices. Specifically, the PA, LNA, DSA, and VGA chips in RRU devices mainly use GaAs or GaN processes, sourced from companies like Qorvo and Skyworks, with GaN devices typically using SiC substrates, i.e., GaN on SiC. RF transceivers and analog-to-digital converters use silicon-based and GaAs processes, with major suppliers including TI, ADI, and IDT, all of which are American companies. Therefore, the dependency of communication base station chips on US firms is extremely high.

Main Chips in Base Station Communication Equipment

(3) Automotive Electronics: Industry Technology Becoming Mature, Some Achievements in Localization

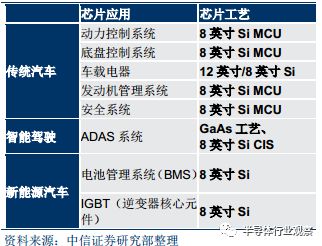

Automotive electronics primarily demand semiconductor devices such as MCUs, NOR Flash, and IGBTs. Traditional vehicles mainly have high demand for MCUs, including power control, safety control, engine control, chassis control, and in-car electronics, among various aspects. New energy vehicles also include electronic control units (ECUs), power control units (PCUs), vehicle control units (VCUs), hybrid vehicle control units (HCUs), battery management systems (BMS), and core components like IGBT inverters.

Internal Chips in Traditional Vehicles

In addition to the above-related systems, NOR Flash is also required for code storage in emergency braking systems, tire pressure detectors, airbag systems, etc. MCUs typically use 8-inch or 12-inch 45nm-0.15μm mature processes, while NOR Flash generally uses 45nm-0.13μm mature processes, with domestic production having been largely achieved.

Chips Inside Automotive Electronics

Semiconductor devices used in intelligent driving include high-performance computing chips and ADAS systems. High-performance computing chips currently use advanced processes on 12-inch wafers, while millimeter-wave radar in ADAS systems involves GaAs materials, which are currently not produced in mass in China.

(4) AI and Mining Machine Chips: New Growth Drivers, Domestic Design Firms Achieve Breakthroughs

AI chips and mining machine chips are categorized as high-performance computing devices, requiring advanced processes. In AI and blockchain scenarios, traditional CPU computing power is insufficient, leading to the emergence of new architecture chips as a development trend. Currently, there are traditional architecture paths such as GPU, FPGA, and ASIC (TPU, NPU, etc.), as well as paths that completely overturn traditional computing architectures by using structures that simulate human brain neurons to enhance computing power. In the cloud domain, the GPU ecosystem is leading, while specialization in terminal scenarios is the future trend.

Overview of Core AI Chips

According to the technology roadmaps published by NVIDIA and AMD, GPUs will enter 12nm/7nm processes in 2018. Currently, AI and mining-related FPGA and ASIC chips are also using advanced processes ranging from 10nm to 28nm. Domestic firms like Cambrian, Deep Vision Technology, Horizon, and Bitmain have emerged as excellent IC design companies that have achieved breakthroughs, while manufacturing primarily relies on advanced process foundries like TSMC.

Future Outlook: Some Fields Expected to Break Through First, More Participation in Global Division of Labor

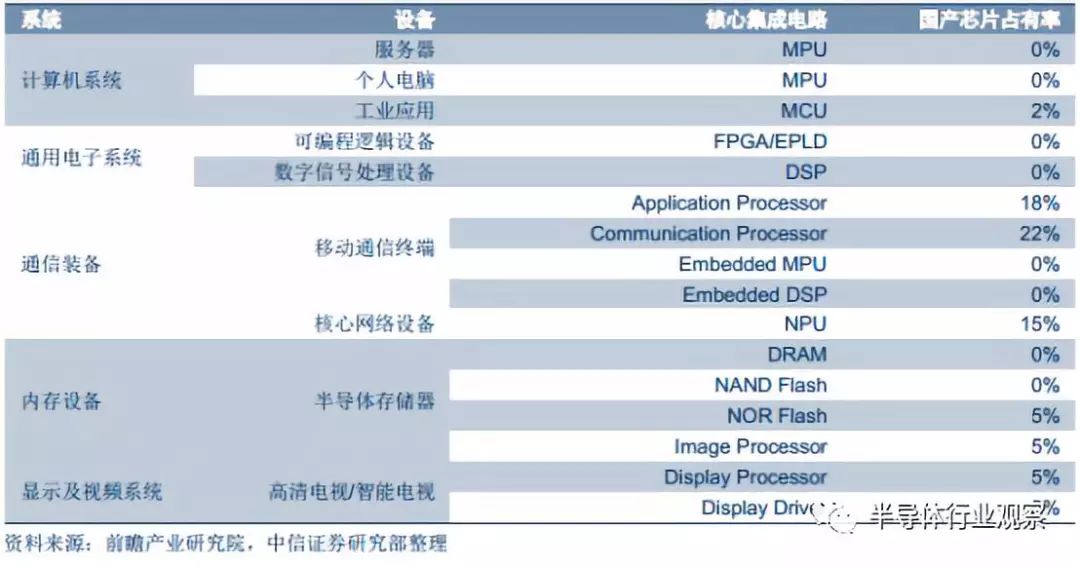

At present, the level of localization is low, and the semiconductor industry actually relies on global cooperation. Although China’s semiconductor industry is currently in a rapid development stage, overall, there are issues such as low overall capacity, weak competitiveness in the global market, low localization levels in core chip fields, and high dependency on foreign suppliers. China’s semiconductor industry chain is highly dependent on imports in several high-end fields, including materials, equipment, manufacturing, and design. Achieving self-sufficiency in the semiconductor industry will require a long journey.

Current Market Share of Domestic Core Integrated Circuit Chips

According to IC Insight data, in 2015, China’s integrated circuit companies held only 3% of the global market share, while the US, South Korea, and Japan held 54%, 20%, and 8%, respectively. In fact, even the US, South Korea, and Japan cannot achieve 100% self-sufficiency in the semiconductor industry chain. For example, in the core equipment for advanced process manufacturing, photolithography machines still rely on the Dutch company ASML. More participation in the global division of labor, gradually increasing the localization ratio in the process, is a practical development path for the semiconductor industry.

The downstream demand side of mainland China’s chips is fully equipped, and the supply side is expected to tilt towards mainland China. (1) Demand side: The downstream terminal application market is fully equipped, and the scale conditions are gradually maturing. As global terminal product capacity shifts to China, it has become a global manufacturing base for terminal products. In 2017, China’s automobile and smartphone shipments accounted for 29.8% and 33.6% of the global total, respectively. Chip demand fully covers both silicon-based and compound semiconductor markets, with huge market space for chips. (2) Supply side: Currently, there are only a few IC design, wafer foundry, and storage manufacturers in mainland China with significant output scale, and the technical level has not yet reached a leading position. The manufacturing of mid-to-high-end chips and compound semiconductor chips is severely reliant on imports. As terminal demand gradually shifts to mainland China alongside industries like smartphones, this demand shift may drive manufacturing transfer, and the downstream chip supply side is beginning to shift to the mainland.

Domestic policies accelerate the development of the semiconductor industry. In recent years, China’s integrated circuit support policies have been intensively issued, with financing, taxation, and subsidy policies continuously optimized. Especially the “National Integrated Circuit Industry Development Promotion Outline” issued in June 2014, which sets the tone for “design as the leader, manufacturing as the foundation, equipment and materials as support,” aims to promote the development of China’s integrated circuit industry with growth cycles of 2015, 2020, and 2030: the goal is to exceed 350 billion yuan in sales revenue for the integrated circuit industry by 2015; to achieve an average annual growth rate of over 20% in sales revenue by 2020; and to reach international advanced levels in major segments of the integrated circuit industry chain by 2030, with a number of enterprises entering the first tier internationally and achieving leapfrog development.

This article is sourced from: The World of Lithographers