PCB Network City News

This article is an original piece from the “Focus” section of the November 2022 issue of “Printed Circuit News” titled “The Shift of the PCB Industry to Southeast Asia: Opportunities and Risks”. Unauthorized reproduction by any individual or organization is prohibited. For reprints, please contact us for permission. Thank you!

In the past two years, the domestic PCB industry has faced numerous challenges, including the pandemic, trade wars, and geopolitical black swan events, accelerating overseas investments by PCB companies, particularly in Southeast Asia. Dr. Yun Wenjie from the Shenzhen University Research Center for China’s Special Economic Zones pointed out that Southeast Asia is the preferred region for Chinese electronics industry overseas investments. On one hand, the signing of the Regional Comprehensive Economic Partnership (RCEP) has promoted economic and trade cooperation between Chinese enterprises and ASEAN countries. On the other hand, the expansion of the industrial and value chains in the Guangdong-Hong Kong-Macao Greater Bay Area will continue to drive companies seeking greater profits towards ASEAN and Belt and Road countries.

The Taiwan Printed Circuit Association (TPCA) noted that, in light of the need to diversify production risks, Taiwanese manufacturers are not only continuing to expand new capacities in Taiwan and mainland China but are also actively laying out the Southeast Asian market. Regions such as Malaysia and Thailand have seen Taiwanese companies announce expansion investments, continuously injecting new vitality into Taiwan’s PCB industry. Thailand has become a major production hub for Taiwanese companies in Southeast Asia, emerging as a new settlement outside of the two sides of the Taiwan Strait. In mainland China, many PCB companies feel the demand from customers to diversify production bases and have begun planning or have officially started building overseas production bases, with Southeast Asia being the preferred location.

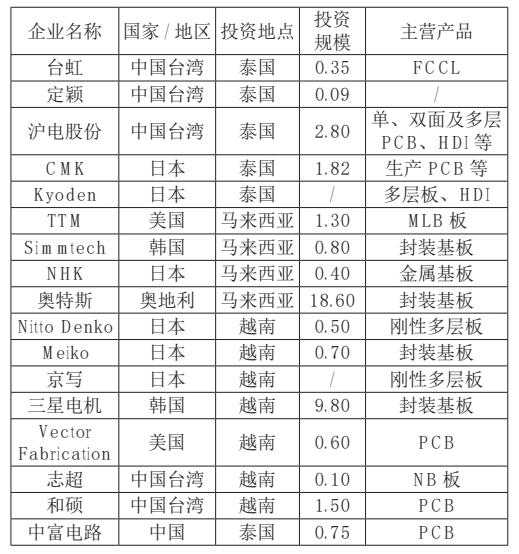

Table 1: New PCB Investment Projects in Southeast Asia

(Unit: 100 million USD)

What is Southeast Asia?

Southeast Asia is a region name that emerged during the late stages of World War II, strategically located between Asia and Oceania, connecting the Pacific and Indian Oceans. Southeast Asia consists of two main parts: the Indochinese Peninsula and the Malay Archipelago, comprising 11 countries: Vietnam, Laos, Cambodia, Thailand, Myanmar, Malaysia, Singapore, Indonesia, Brunei, the Philippines, and East Timor, with a total land area of 4.44 million square kilometers, playing a crucial role in the Belt and Road Initiative. Except for the newly established East Timor, the ten countries in the region form the Association of Southeast Asian Nations (ASEAN), aimed at promoting regional cooperation and integration in economic, political, security, military, education, and socio-cultural aspects among member states and other Asian countries (On November 11, 2022, ASEAN stated that it “principally agreed” to accept East Timor as a new member state).

In recent years, ASEAN countries have maintained a high economic growth rate, becoming the fifth largest economy in the world. In the post-pandemic era, they have shown a strong recovery trend compared to other economies. In the third quarter of 2022, Malaysia’s GDP grew by 14.20% year-on-year, with a growth of 9.36% in the first nine months of this year; Vietnam’s GDP growth also reached 13.67%; the Philippines and Indonesia grew by 7.60% and 5.72% year-on-year, respectively. The Asian Development Bank predicts that the overall GDP of Southeast Asian countries is expected to grow by about 5.2% in 2022.

As the value chain position of Southeast Asia becomes more prominent, its share of internal added value continues to rise, and the global value chain is beginning to shift towards Southeast Asia. Anna Marindog, an expert on international relations in the Philippines, told the Global Times that first, ASEAN countries generally have a demographic dividend. For example, the population of the Philippines has rapidly increased from 78 million in 2000 to 110 million today, with a growing young population and relatively good education levels providing a solid foundation for economic development. The population size and structure of other ASEAN member countries, such as Indonesia and Vietnam, are also suitable for manufacturing development. Second, there is a natural resource dividend. The Philippines ranks third globally in gold reserves, and its copper and nickel reserves are also among the top. Third, many livelihood projects have been built in recent years, laying a foundation for this round of economic development. Fourth, there is a certain relationship with the international environment, especially since the China-U.S. trade friction in 2018, where multinational companies from the U.S. and Europe have shifted some manufacturing to Southeast Asia, benefiting the ASEAN economy. Finally, the “dividend” brought by Chinese investments cannot be overlooked. Data released by the Ministry of Commerce, the National Bureau of Statistics, and the State Administration of Foreign Exchange show that in 2021, China’s direct investment in the ten ASEAN countries reached $19.73 billion, an increase of 22.8%.

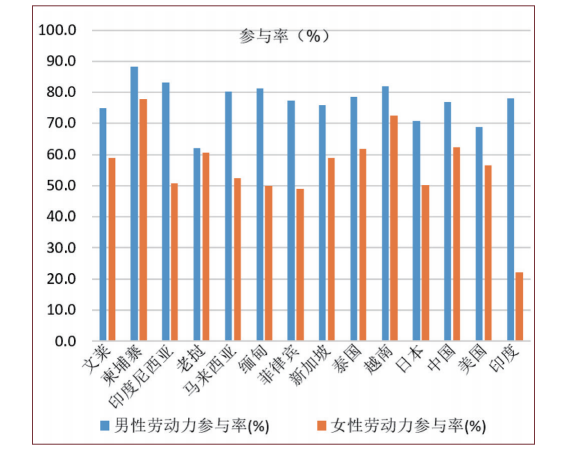

Figure 1: Average Labor Force Participation Rate by Gender in ASEAN and Comparison Countries (in %)

Figure 1: Average Labor Force Participation Rate by Gender in ASEAN and Comparison Countries (in %)

On January 1, 2022, the Regional Comprehensive Economic Partnership (RCEP) officially came into effect. RCEP was initiated by the ten ASEAN countries and includes major countries in East Asia and Southeast Asia. According to estimates by the Chinese Ministry of Commerce, ASEAN will benefit the most at the macroeconomic level from RCEP: by 2035, the cumulative GDP growth rate of ASEAN will increase by 4.47% due to the implementation of RCEP. The Malaysian Ministry of International Trade and Industry stated that RCEP will be a “key driver” for the country’s economic recovery post-pandemic, with an expected increase in revenue of $200 million through RCEP exports. Data from the Thai Ministry of Commerce shows that in the first two quarters after RCEP officially came into effect, trade between Thailand and RCEP member countries reached $169.04 billion, a 13% increase compared to the same period last year. A report from the Philippine Institute for Development Studies indicates that once the country ratifies the RCEP, its exports will grow by 10.47%, driving GDP growth by 2.02%.

Why Move to Southeast Asia?

With economic development and increasing integration, Southeast Asia’s global influence is growing. The “Free and Open Indo-Pacific Strategy” proposed by Japan, the “Indo-Pacific Strategy” launched by the United States, China’s implementation of the “Belt and Road Initiative”, and the effectiveness of RCEP have further enhanced Southeast Asia’s strategic position globally. In recent years, the advantages of Southeast Asia in investment policies, future potential markets, and labor costs have gradually become prominent. Southeast Asia has a rich population resource, with a total population of 660 million across the ten ASEAN countries, and the demographic dividend is being released. Except for Singapore, most of Southeast Asia is classified as developing countries, with the manufacturing sector’s share of GDP continuously rising.

With the rise of economic circles such as the Belt and Road Initiative and RCEP, as well as geopolitical influences, more and more circuit board companies are beginning to invest and establish factories in Southeast Asia. Currently, the PCB industry in Southeast Asia is mainly concentrated in six countries: Thailand, Vietnam, Malaysia, the Philippines, Singapore, and Indonesia, primarily involving Japanese, Korean, and Taiwanese enterprises. Taiwanese companies have indicated that in Thailand, the local automotive supply chain is well-developed, with Japanese automakers having a complete layout in the area, making the automotive market one of the targets for Taiwanese businesses. Additionally, there are concerns about policy risks in China and issues related to electricity and labor supply in Taiwan, as well as the need to diversify risks for end customers.

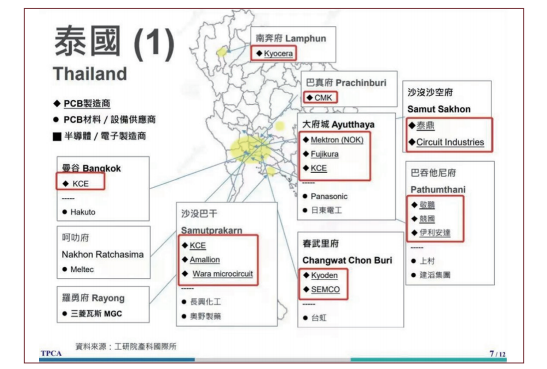

Figure 2: Distribution Map of PCB Enterprises in Thailand

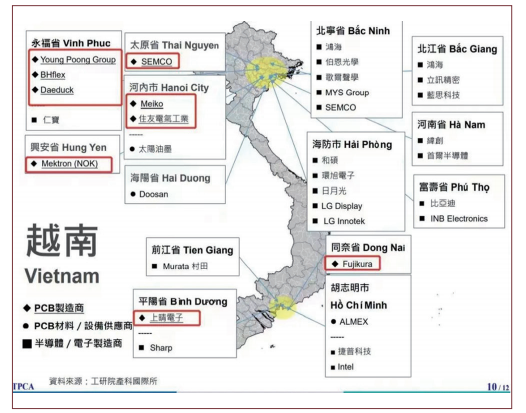

Figure 3: Distribution Map of PCB Enterprises in Vietnam

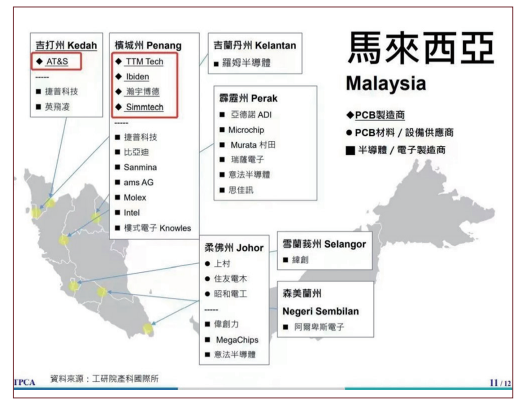

Figure 4: Distribution Map of PCB Enterprises in Malaysia

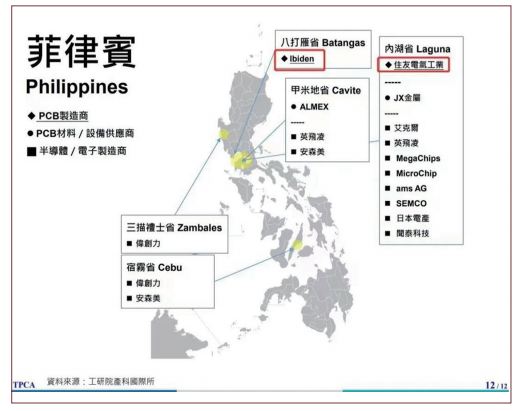

Figure 5: Distribution Map of PCB Enterprises in the Philippines

In the post-pandemic era, coupled with geopolitical risks, domestic companies are also beginning to establish production bases in Southeast Asia. On July 29, Zhongfu Circuit announced that the company plans to invest in establishing a subsidiary in Thailand, with an investment amount not exceeding $75 million, focusing on the design, production, and sales services of PCBs and electronic products. Zhongfu Circuit’s General Manager Wang Xianfeng stated: “Investing in Thailand is mainly based on the need to diversify customer risks, and on the other hand, it also responds to the national demand for the Belt and Road Initiative.”

Overseas investment, in addition to being driven by customer and policy factors, is also considered by some companies as part of their global layout strategy. Mingyang Circuit is one such company. Chairman Zhang Peike stated that Mingyang Circuit’s strategic direction is internationalization, and investing in Southeast Asian countries is a measure of the company’s global strategic layout. When discussing the site selection for investment in Southeast Asia, Chairman Zhang Peike believes that considering factors such as personnel, logistics, industrial chain, and geographical advantages, Vietnam, Thailand, and Malaysia can be key countries for investment layout in Southeast Asia; taking into account transportation costs and other factors, Thailand and Malaysia have prominent advantages. Data shows that Vietnam’s economy is developing rapidly, with clear outward-oriented economic characteristics, gradually optimizing its industrial structure, and steadily growing domestic consumption market, with major industries including energy, food, textiles, chemicals, construction, electronics, information technology, and processing manufacturing. Malaysia and Thailand rank among the top in Asia in terms of economic development levels, with economies primarily based on industry, manufacturing, tourism, and agriculture, and in recent years actively developing shipping, finance, and logistics industries. Additionally, Thailand is the largest overseas processing base for the Japanese automotive industry.

General Manager Zhou Jianxin of Cheng’an Group also provided insights from a supply chain perspective. He stated that from the perspective of material suppliers, considering various factors such as customer requirements for shipping timeliness and quantity, the trend of product diversification, the feasibility of setting up factories overseas, the origin of recycled copper, and the existing market in Southeast Asia, trade companies recommend choosing Singapore, while factories are recommended to be set up in Thailand. Compared to other Southeast Asian countries, Thailand has a relatively complete logistics system, and market demand is larger than in other Southeast Asian countries. Among the 11 countries in Southeast Asia, several major PCB manufacturers are located in Thailand, including APEX and KCE, which together have a production value of $1.018 billion.

Furthermore, Southeast Asian countries continue to introduce favorable business policies to further stimulate foreign investment. In 2021, Thailand’s Board of Investment (BOI) announced modifications to investment incentives for the semiconductor manufacturing and PCB manufacturing industries. They encourage the development of advanced PCB manufacturing, including FPC and multilayer PCBs, such as PCBFAB, FALab, SMT, PTH, and PCBA testing, with a minimum machine investment of 1.5 billion Thai Baht to enjoy an 8-year corporate income tax exemption; if the machine investment is less than 1.5 billion Thai Baht, a 5-year corporate income tax exemption is granted.

Local officials have stated in media interviews that over the past decade, many Southeast Asian countries have continuously increased investment in public infrastructure, providing more job opportunities and improving people’s living standards. As the focus of the Belt and Road Initiative, the construction or upgrading of high-speed rail, highways, and other infrastructure in the 11 Southeast Asian countries will mean greater market opportunities.

What Challenges Are There in Moving to Southeast Asia?

According to the Taiwan media “Commercial Times”, Taiwanese electronics manufacturers are actively laying out in Southeast Asia, especially PCB manufacturers, with companies such as Taidong-KY, Jingpeng, and Jingguo having production capacities in Thailand, while companies like Jingchengke have announced their entry into Southeast Asia this year. Despite the investment boom in Southeast Asia, the challenges behind it are also concerning. For example, Vietnam is positioned at the downstream of the international industrial chain, and due to the lack of a complete domestic industrial chain, it still relies heavily on upstream countries like China for raw materials, key technologies, and core equipment.

Some Taiwanese companies that have laid out in Southeast Asia have stated that the advantages of Southeast Asia include diversifying production risks, meeting customer demands, and lower labor costs. However, the current disadvantages include an incomplete supply chain, high procurement costs, and while labor costs are low, it is difficult to find mid-level engineering personnel, and expatriate Taiwanese staff require higher salary packages. Zhongfu Circuit’s General Manager Wang Xianfeng stated: “We hope more companies will go out and form a scale and environment for industrial matching overseas… The issue of raw material transportation affecting overseas investment will change in the next 3-5 years.” In the view of Xingmeike’s Chairman Tu Yixin, the employee issue in setting up factories in Vietnam will be a challenge: first, there are relatively fewer male employees, with more females, and males hold a relatively higher status, making personnel management a significant challenge; second, training costs for personnel are relatively high compared to domestic levels, and employee work efficiency is lower than that of domestic employees; additionally, there are challenges such as low product yield rates, high logistics costs, and less complete electrical infrastructure. Liu Tianming, Chairman of Si Hui Fushi, stated that as customer quality requirements become increasingly stringent, some overseas customers require factory certifications, thus overseas investment requires substantial funding, and he hopes the association can organize overseas inspection teams so that Guangdong PCB companies can band together to go out and form a matching scale, creating a good investment environment.

Geopolitical conflicts are also a concern. Currently, the strategic competition between China and the U.S. and the U.S. government’s sanctions and technological blockade against China’s high-tech industries have intensified geopolitical conflicts in the Asia-Pacific region, increasing the uncertainty of enterprises investing and developing in Southeast Asia. Dr. Yun Wenjie from Shenzhen University suggests that when investing overseas, special circumstances should be considered, and trade routes should be planned in advance, ensuring that product lines do not form complementary relationships.

According to Filipino scholar Anna, ASEAN countries have relatively small economic volumes; their technological innovation capabilities are weak, and they can only passively undertake part of the supply chain from developed economies without being able to lead the industrial chain; the amount of funding is not large, and development mainly relies on external investment. She stated that Southeast Asia’s economic development still faces some complex factors, such as political instability in some countries, inadequate infrastructure, and insufficient protection for foreign investment. “Countries like the Philippines are greatly affected by climate change, with many environmental concerns, and hold a rejection attitude towards some industries.”

On November 15, the Guangdong Circuit Board Industry Association/Shenzhen Circuit Board Industry Association organized a roundtable forum, inviting Dr. Yun Wenjie from Shenzhen University, Mingyang Circuit’s Chairman Zhang Peike (online), Si Hui Fushi’s Chairman Liu Tianming, Cheng’an Copper’s General Manager Zhou Jianxin, and Xingmeike’s Chairman Tu Yixin to interpret the overseas market environment.

“Printed Circuit News” November 2022 e-book is now online. Readers can scan the QR code below to view more exciting content.

“Printed Circuit News” November 2022 e-book is now online. Readers can scan the QR code below to view more exciting content.

On November 17, the 2022 South China PCB International Trade Procurement Expo successfully concluded at the Shenzhen International Convention and Exhibition Center (Bao’an New Hall)! During this exhibition, Diancao Live partnered with the 2022 South China PCB International Trade Procurement Expo to build a “cloud exhibition” platform, with the entire exhibition live-streamed, showcasing the exhibitors on-site and presenting the overall view of the exhibition online. Scan the QR code below to review the exhibition highlights and the exhibitors’ profiles!

On November 17, the 2022 South China PCB International Trade Procurement Expo successfully concluded at the Shenzhen International Convention and Exhibition Center (Bao’an New Hall)! During this exhibition, Diancao Live partnered with the 2022 South China PCB International Trade Procurement Expo to build a “cloud exhibition” platform, with the entire exhibition live-streamed, showcasing the exhibitors on-site and presenting the overall view of the exhibition online. Scan the QR code below to review the exhibition highlights and the exhibitors’ profiles!

For more PCB industry news, long press the QR code below to view.

For more PCB industry news, long press the QR code below to view. ▲GPCA Official Account▲

▲GPCA Official Account▲