Click the blue text

Follow us

This public account is a non-profit MEMS technology dynamics and industry reporting platform under the Guangdong Microtechnology Industrial Research Institute. We publish in-depth reports on MEMS, track industry dynamics, and provide technical popularization every week. This article is an in-depth report and is the 129th article of the public account.

In the previous article, we deeply analyzed the five major technical paths of MEMS pressure sensors—resistive, capacitive, resonant, fiber optic, and piezoelectric—discussing their working principles, performance differences, and selection logic. We clarified the core characteristics of different technologies in terms of sensitivity, power consumption, and environmental adaptability, as well as their preliminary application directions in automotive, medical, and industrial fields.

This article, as a follow-up, will focus on the industrial implementation level: starting from the oligopolistic market structure globally, we will analyze the progression path of domestic companies from technology followers to partial breakthroughs, delve into the innovative applications of MEMS pressure sensors in emerging scenarios, and look forward to the technological evolution trends in materials, processes, and intelligence, presenting a more complete industrial ecosystem to industry practitioners.

01

Market Size and Growth Drivers

The MEMS pressure sensor market is in a steady expansion phase, with both global and Chinese markets showing strong growth potential, driven by rigid demands from various fields such as automotive, consumer electronics, medical, and industrial.

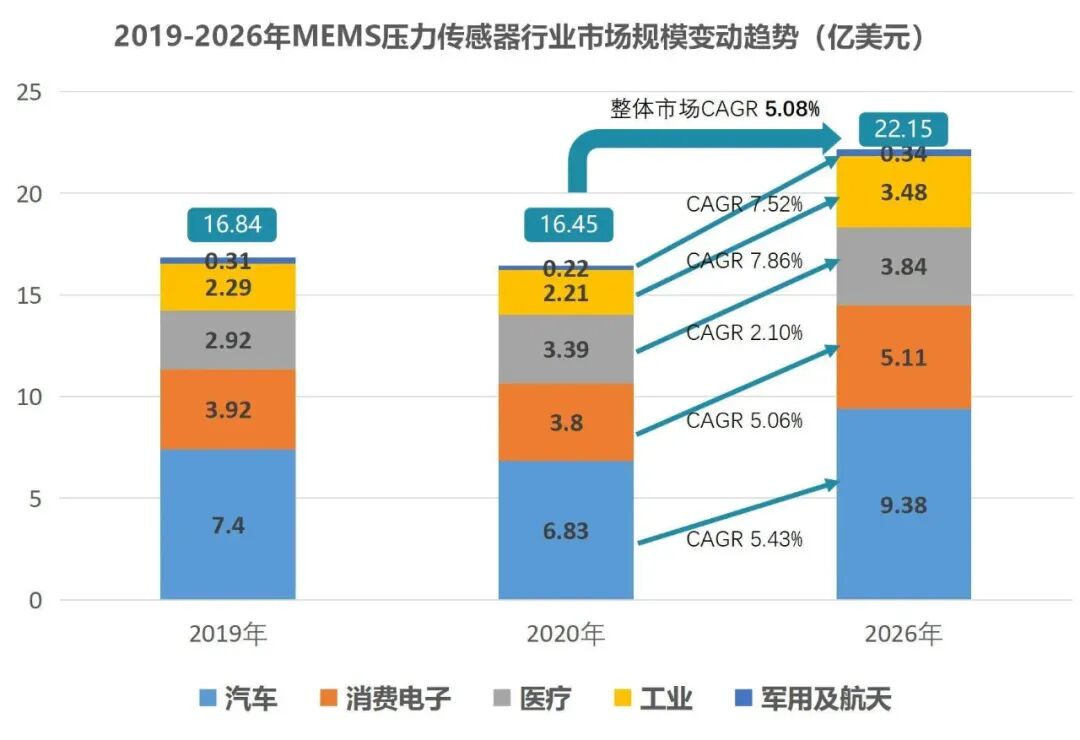

From a global market perspective, Yole data shows that the global MEMS pressure sensor market size was $1.684 billion in 2019, and it is expected to reach $2.215 billion by 2026, with a compound annual growth rate (CAGR) of about 5%; shipments are expected to grow from 1.485 billion units to 2.183 billion units, with a CAGR of about 4.9%. Another organization, ReportLinker, predicts that the market size will reach $2.36 billion in 2023 and exceed $3.19 billion by 2028, with the CAGR increasing to 6.2%, driven mainly by the explosive demand from industrial automation and miniaturized consumer devices (such as wearable devices and IoT terminals).

The growth of the Chinese market is even more rapid. In 2020, the MEMS pressure sensor market size in China was about 13.5 billion yuan, driven by consumer electronics, wearable devices, drones, and medical fields, combined with the accelerated localization process. It is expected to approach 30 billion yuan by 2025, with a CAGR exceeding 16%. This growth rate far exceeds the global level, reflecting the urgent need for the domestic industry chain to have independent control over core components.

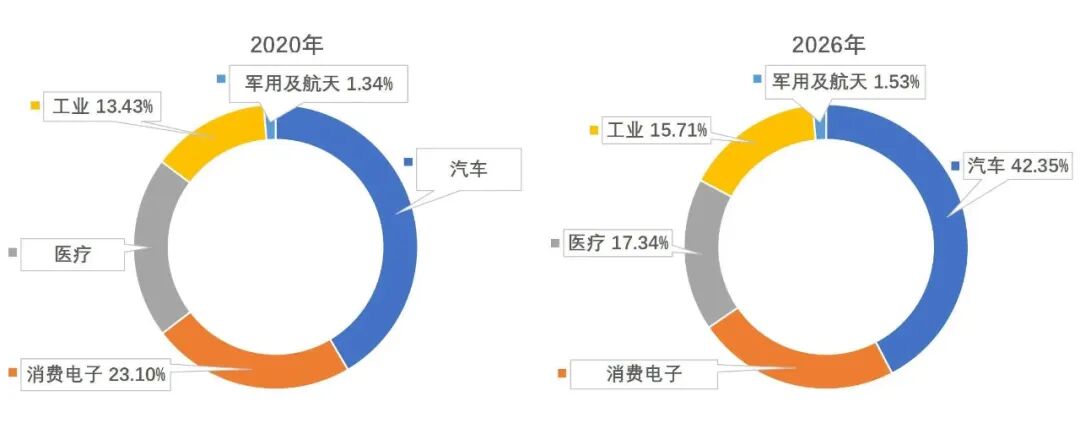

By sector, the automotive industry is the largest application market, accounting for over 40% of global sales. High-end vehicles typically equip 30-50 MEMS sensors, of which about 10 are pressure sensors used in critical areas such as braking systems, tire monitoring, and engine management. Consumer electronics follow closely, accounting for about 23%, with barometers and altimeters in smartphones and smartwatches, as well as altitude monitoring in drones relying on their performance. The medical field accounts for 17%, where the accuracy of devices such as ventilators and blood pressure monitors directly depends on the stability of the sensors; industrial automation and aerospace account for 15% and the remaining share, respectively, with the former focusing on pipeline pressure monitoring and the latter imposing strict requirements for high temperature and reliability.

02

Market Structure

The MEMS pressure sensor industry has long been dominated by foreign companies due to high technical barriers and complex processes, resulting in a market structure characterized by “oligopoly dominance and local weakness.” However, in recent years, there has been a glimmer of hope for domestic substitution.

1

International Companies

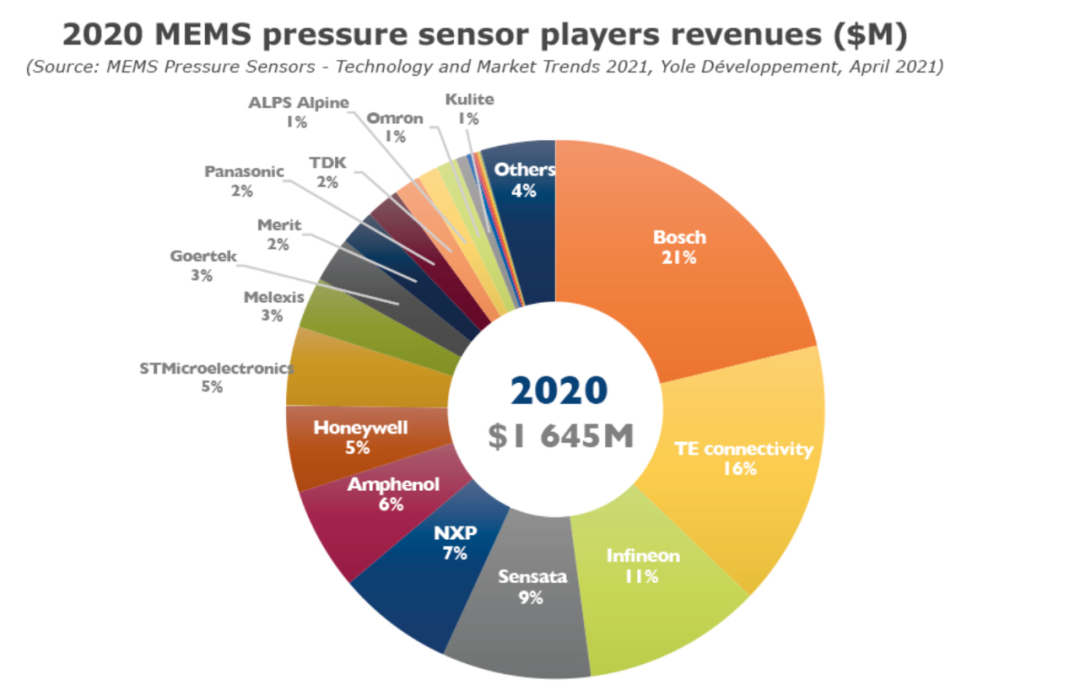

The global market is highly concentrated, with the CR3 (market share of the top three companies) reaching 77%. Leading manufacturers include Bosch, TE Connectivity, Infineon, and Sensata. Among them:

Bosch, as the world’s largest automotive technology supplier, is known for its MEMS pressure sensors’ high reliability and accuracy. The BMP581 capacitive barometric sensor launched in 2022 is widely used in consumer electronics and automotive fields due to its small size and low power consumption;

Sensata monopolizes the assembly and core chip market for medium and high-pressure pressure sensors, holding over 50% of the automotive exhaust temperature sensor market;

STMicroelectronics‘s VENSENS technology enhances reliability through a suspended membrane design, with products covering automotive, medical, and other scenarios;

Honeywell focuses on industrial and aerospace fields, with its full range of products supporting a pressure range from 3 psi to 8000 psi, featuring outstanding corrosion resistance.

In the segmented field, the differential pressure sensor assembly market is controlled by Bosch, DENSO, and Delphi, while core chips are dominated by NXP, Infineon, and Melexis, with domestic companies’ market share being almost negligible.

2

Domestic Companies

Domestic companies started relatively late, mainly consisting of small and medium-sized enterprises, most of which rely on imported chips for assembly, with a localization rate of less than 5%. However, in recent years, some companies have achieved breakthroughs in niche areas through technological research and development and industrial chain integration, gradually breaking the foreign monopoly from consumer electronics to automotive-grade, from industrial scenarios to extreme environments.

-

Naixun Micro

Focusing on automotive and consumer electronics, it has shipped over 150 million pressure sensors. In the medical field, its NSPGS5 series sensors for ventilators replace imported solutions with 1.5% accuracy; in the automotive field, the NSPAD1N series ultra-small absolute pressure sensors are suitable for seat airbags and massage functions, supporting both analog and digital outputs, meeting AEC-Q100 standards, and have entered overseas battery pack thermal runaway monitoring projects; in industrial scenarios, the NSA/C2860 series conditioning chips are applied in petrochemical transmitters, gradually replacing overseas solutions.

-

Minxin Co., Ltd.

In 2024, the revenue share of pressure sensors will rise to 41.85%, with products embedded in the supply chains of consumer electronics such as Samsung and Xiaomi, achieving import substitution in blood pressure monitors and health monitoring devices. It is also expanding into humanoid robotics, developing three-dimensional force sensors for finger joints and wrists, as well as glove-type tactile sensors, with related products advancing customer sampling, expected to seize opportunities in emerging scenarios.

-

Amperelong

As a leading domestic substitute for automotive-grade pressure sensors, its pressure sensor revenue reached 468 million yuan in 2024, a year-on-year increase of 32.17%. Its MEMS pressure sensors are supplied in bulk to international automakers such as Stellantis, with products like carbon canister desorption pressure sensors and crankcase ventilation pressure sensors entering overseas supply chains; in critical scenarios, brake system vacuum sensors and exhaust system differential pressure sensors have been designated by well-known European OEMs, and glass micro-melting pressure sensors have won bids for domestic leading new energy vehicle projects, achieving import substitution in core automotive components.

-

Qitai Sensor

It has established the only domestic mass production line for metal-based pressure-sensitive chips and sensors, specializing in metal-based thin-film pressure-sensitive chips and sensors for hydraulic equipment, breaking the long-standing reliance on imports for hydraulic sensors in China’s engineering machinery. Its products achieve international leading levels in range, accuracy, and zero-point temperature drift, widely used in rail transit, engineering machinery, automotive, smart firefighting, and petrochemical fields. Relying on key heterogeneous film process technology, it fills the gap in the large-scale industrial production of metal-based pressure-sensitive chips in China, laying the foundation for the localization of pressure sensors in high-end equipment fields.

-

Jingwei Precision

It has broken through the “bottleneck” technology of deep-sea pressure sensors, with its CYH1454606 product achieving over 99.9% measurement coincidence with internationally renowned temperature-salinity-depth profilers (CTD) during kilometer sea trials, with indicators comparable to imported sensors, breaking China’s reliance on imported sensors in marine survey fields and providing autonomous and controllable solutions for deep-sea exploration.

-

Jinchip Max

One of the few domestic companies capable of high-precision MEMS pressure sensor chip design and mass production, with annual shipments exceeding 1 million units in the industrial field, ranking first among domestic chips. Its process industry sensors achieve an accuracy of 0.0004, and the M series sensors have been supplied in bulk to Chuan Instrument Co., fully replacing international brands such as First Sensor and Nova Sensor, becoming the largest supplier of high-precision pressure chips for the domestic process industry.

-

Jintianhong Technology

It has developed high-precision MEMS resonant pressure sensors with a precision level of 0.0001, surpassing traditional sensors by 1-2 orders of magnitude, featuring digital output and radiation resistance, and has been applied in aerospace atmospheric data systems and petrochemical pressure measurements in high-end fields, achieving domestic autonomy and control of core chips in this field.

-

Zhaoyi Innovation

With a differentiated product portfolio covering multi-scenario needs, its GDY1121 barometric sensor consumes only 3.5μA at a 1Hz sampling rate, with an absolute accuracy of ±0.5hPa, suitable for high-end scenarios such as rugged smartphones; GDY1122, with a waterproof rating of 10ATM (supporting underwater detection up to 100 meters) and thrust resistance of 4000-5000g, has become a core component for wearable devices and underwater detection, already in mass production in products from internationally renowned manufacturers. In 2025, it will launch high-end products with integrated water depth measurement functions, capable of measuring water pressure up to 4000hPa, further expanding into high-end markets.

-

Duwei Intelligent

Its DWSPD series MEMS micro-differential pressure sensors highlight zero-point stability, covering a measurement range of ±500Pa to ±35KPa, with an initial error of less than ±1.0% F.S., leading the industry in full-life accuracy. They are widely used in ventilation and air conditioning systems, biological laboratory pressure differential monitoring, fire residual pressure control, and medical ventilators, significantly reducing environmental interference through high-performance ASIC calibration compensation technology, making them a reliable choice for industrial and medical scenarios.

-

Huamei Aotong

It has launched the ATP993 series silicon MEMS pressure sensor chip, with complete independent intellectual property rights, sensitivity, temperature stability comparable to international brands, and outstanding cost performance. Its products cover medical monitoring, industrial control, drones, and meteorological monitoring scenarios, and its “low power consumption + high quality” advantage is expected to accelerate import substitution in consumer and industrial markets.

03

Technological Evolution

The technological breakthroughs of MEMS pressure sensors focus on three major directions: material systems, packaging processes, and structural designs, driving products towards high temperature, high precision, high reliability, and miniaturization.

1

Material Innovation

Traditional silicon-based sensors are prone to PN junction leakage failure in high-temperature environments, failing to meet industrial and aerospace demands. The application of new materials has become key to breaking through this bottleneck.

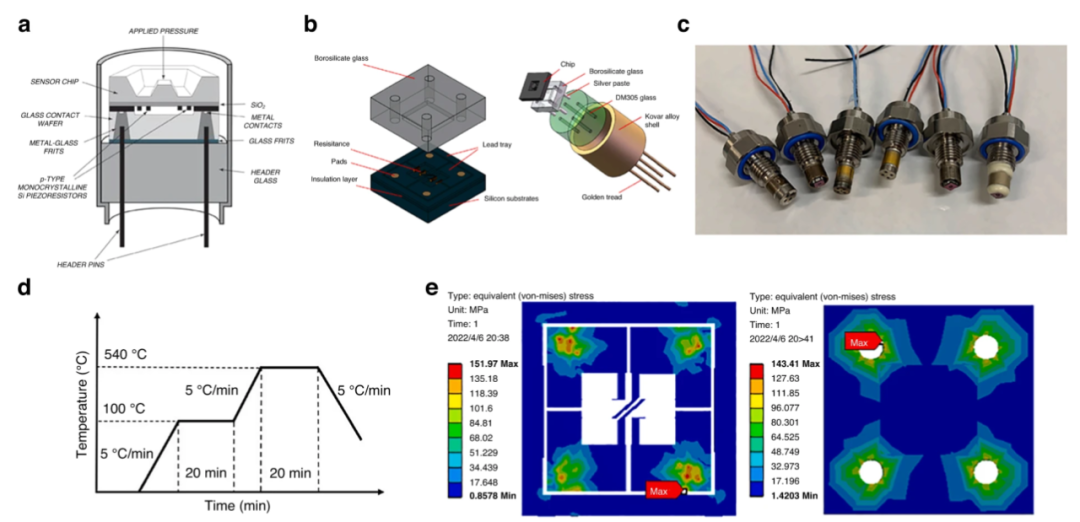

SOI (Silicon on Insulator): By isolating the pressure-sensitive resistor from the substrate with an embedded oxide layer, the leakage current is three orders of magnitude lower than traditional silicon-based sensors, with a temperature resistance of up to 220°C, making it the most mature high-temperature sensor solution on the market;

SOS (Silicon on Sapphire): Using sapphire as the substrate, with a melting point of 2040°C and a working temperature of up to 350°C, it has radiation resistance and corrosion resistance, but stress issues due to lattice mismatch limit its application mainly to large range gauge pressure measurements;

SiC (Silicon Carbide): A third-generation wide bandgap semiconductor material, with a temperature resistance of up to 750°C, excellent radiation and chemical stability, suitable for extreme environments such as rocket engines and gas turbines, but with high manufacturing difficulty and cost, not yet industrialized on a large scale.

Domestic research institutions have made progress in the SiC sensor field, such as the development of SiC sensitive elements using a fully MEMS process, which are small in size and meet micro-pressure measurement needs, providing new options for high-temperature scenarios.

2

Packaging Processes

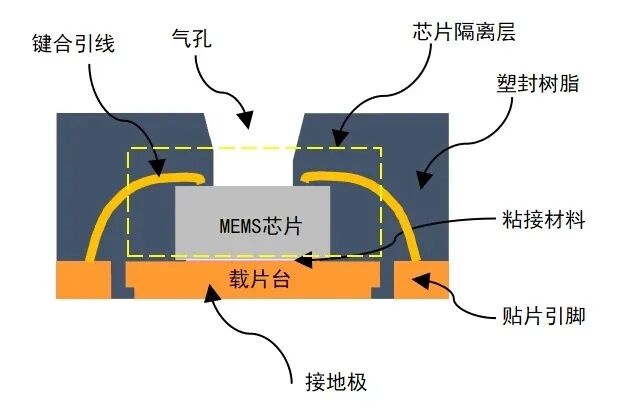

Packaging is key to the commercialization of MEMS pressure sensors, needing to achieve mechanical support, environmental isolation, signal transmission, and heat dissipation functions simultaneously. In recent years, innovative processes have emerged.

Open package technology: Developed by Zhixin Sensor, it adopts an overall plastic sealing mode, blocking the impact of packaging residual stress on the force-sensitive film through a stress isolation structure, reducing costs by 60%, and significantly improving stability through thousands of hours of solvent resistance testing.

Leadless packaging: Based on TSV (Through-Silicon Via) or sintering technology, it reduces stress interference caused by wire bonding, suitable for high-temperature environments.

Oil-filled packaging: Used in deep-sea and high-pressure scenarios, such as the 70MPa resonant sensor developed by the Chinese Academy of Sciences, which adapts to complex hydraulic environments through an oil-filled isolation structure, achieving an accuracy of 0.01% FS.

3

Structural Design

Structural innovation is key to optimizing sensor performance, with typical directions including:

“Beam-Membrane-Island” structure: Used for micro-differential pressure sensors (MDPS), enhancing sensitivity through increased stress concentration effects, achieving up to 66μV/V/kPa, suitable for medical ventilators and fire residual pressure monitoring.

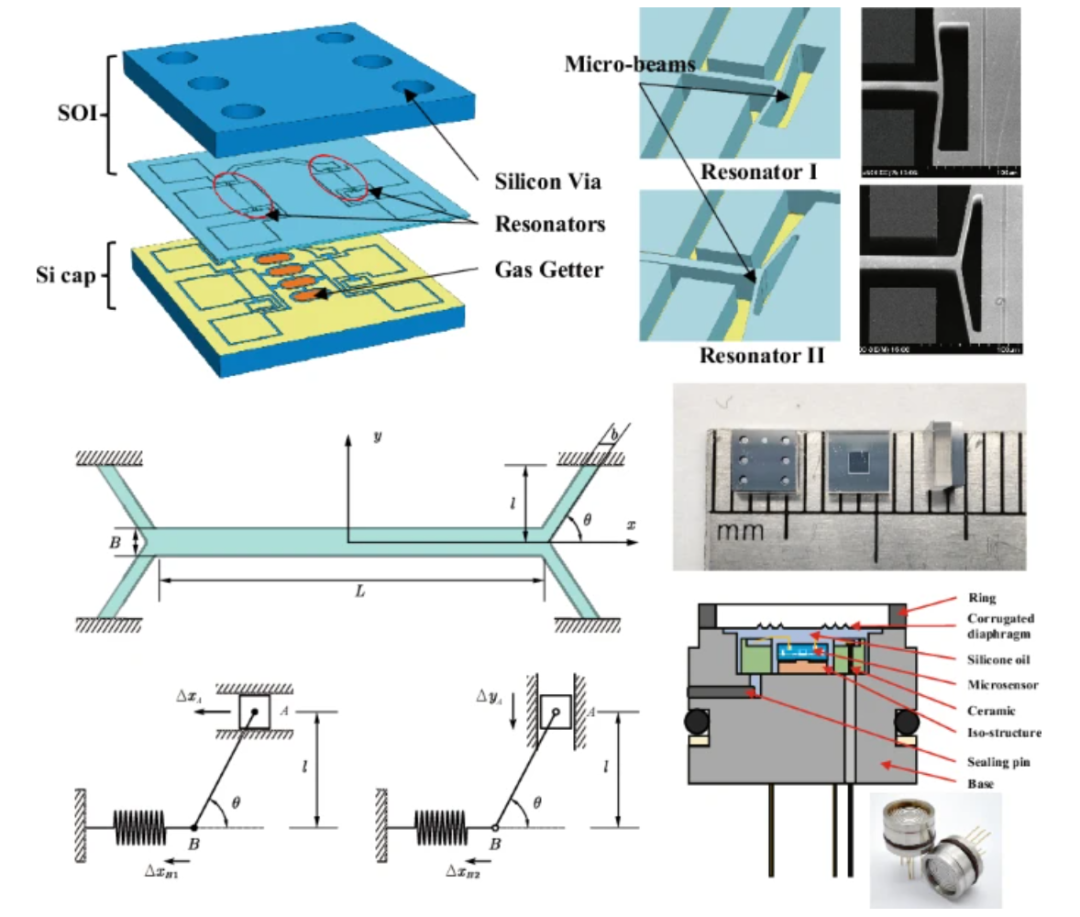

Dual resonator design: For example, the silicon-based resonant sensor developed by the Chinese Academy of Sciences achieves temperature self-compensation through differential pressure sensitivity of two resonators, with accuracy better than 0.01% FS in the range of -10~50℃ and 0.1~70MPa.

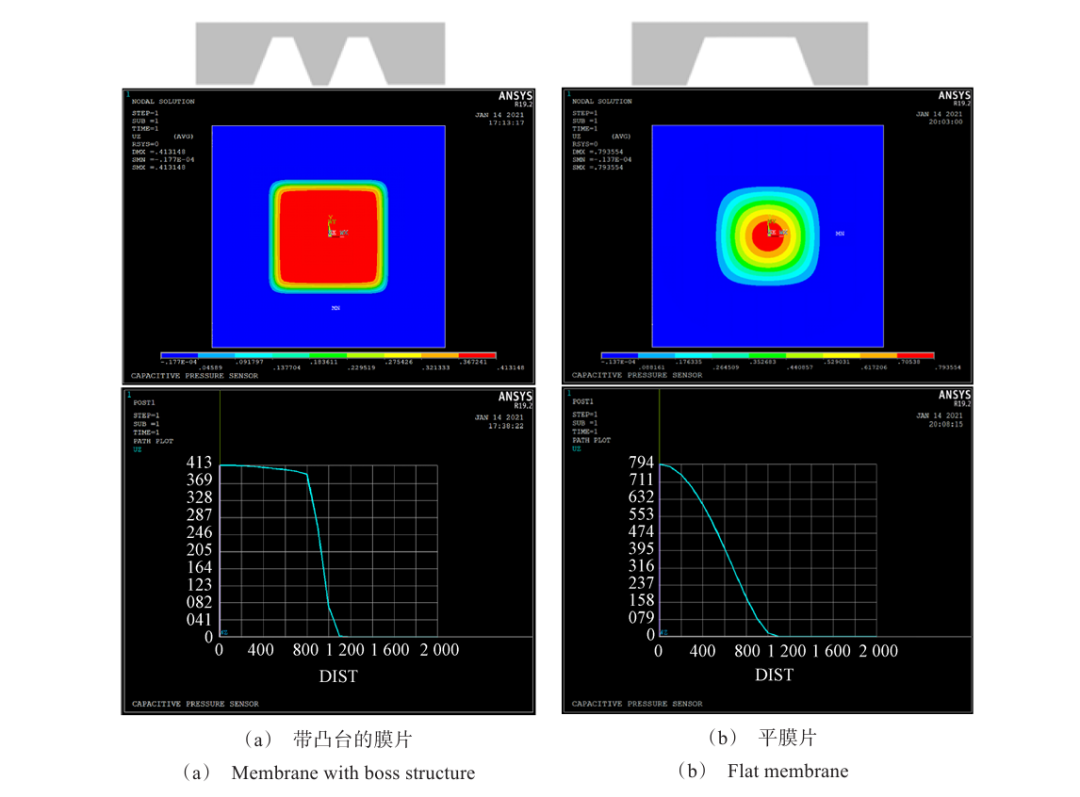

Domed diaphragm structure: The capacitive sensor developed by Peking University adopts this design, reducing non-linearity from 17% to 7%, achieving an accuracy of 0.30%, suitable for implantable medical devices.

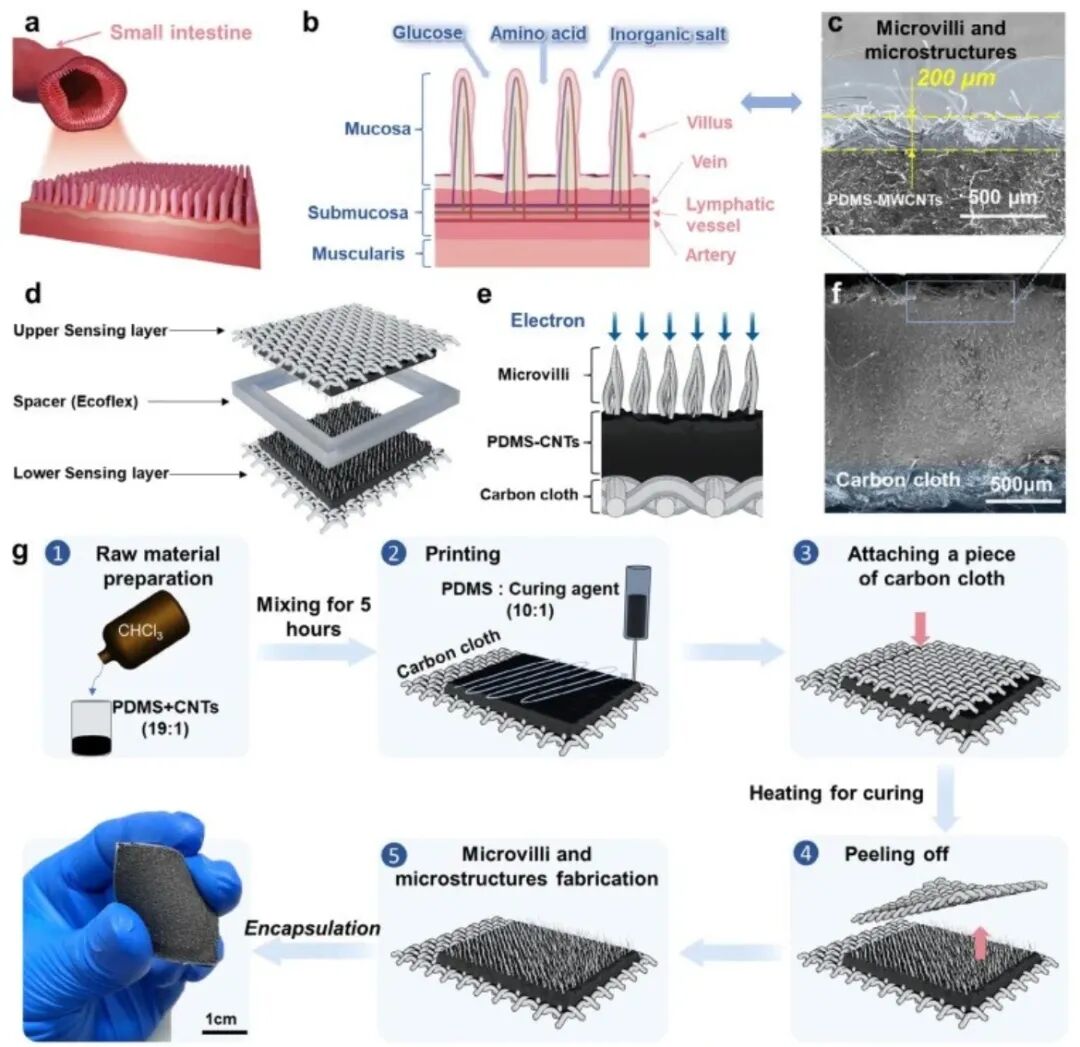

Micro-fiber flexible structure: The flexible pressure sensor developed by Shenzhen University achieves an ultra-wide range of 50Pa to 782.5kPa through the synergistic effect of “micro-fiber electronic transfer enhancement + increased contact area + reduced spacing of carbon nanotubes,” still able to detect 5kPa small changes under 750kPa high pressure, with a response time of only 9ms, providing new solutions for physiological health monitoring and human-computer interaction.

04

Future Trends

The development of MEMS pressure sensors will revolve around three major directions: “performance upgrades, scenario expansion, and ecosystem integration,” driving the industry into a new growth cycle.

1

Continuous Breakthroughs in Performance Indicators

Accuracy, temperature range, and stability remain core pursuits, such as resonant sensors advancing towards 0.001% FS accuracy, high-temperature sensors upgrading to withstand temperatures above 800°C, while also implementing AI algorithms for dynamic compensation to reduce environmental interference.

2

Application Scenarios Continuously Extend

Robotics and Low-altitude Economy: Sensors developed by Minxin Co., Amperelong, and Qitai Sensor are used for robotic joint control, while the demand for barometric monitoring in drones drives the development of miniaturized, low-power sensors.

Deep-sea and Space Exploration: Jingwei Precision’s deep-sea sensors and Jintianhong’s resonant pressure sensors provide core support for marine monitoring and aerospace engineering.

Smart Medical: Peking University’s high-precision MEMS capacitive gauge pressure sensors and the MEMS absolute pressure sensors developed by China Electronics Technology Group 58 Institute promote the development of implantable medical devices, non-invasive diagnostics, and precision treatment.

Flexible Electronics: The flexible pressure sensors developed by Shenzhen University provide new perception solutions for wearable health devices and bionic robots, expected to open new scenarios for human-computer interaction.

3

Accelerated Integration of the Industrial Chain

Domestic companies will transition to the IDM model, achieving vertical integration of chip design, packaging testing, and calibration, such as Naixun Micro constructing a closed loop of “MEMS + ASIC + calibration system” to reduce external dependence. At the same time, mergers and acquisitions will intensify, with leading companies enhancing market concentration by integrating technology teams and product lines.

05

Conclusion

The MEMS pressure sensor industry is at a critical stage of “foreign monopoly and domestic breakthrough,” with steady global market growth and explosive domestic substitution demand providing vast space for the industry. Although challenges such as technical barriers and talent shortages remain, with the support of policies, R&D investment, and scenario expansion, domestic companies have achieved breakthroughs in automotive, medical, and industrial fields. In the future, with material innovation, process upgrades, and ecosystem improvement, MEMS pressure sensors are expected to become an important breakthrough point for China’s semiconductor industry to achieve autonomy and control, contributing the “China solution” to the global industrial chain.

END

Welcome to reprint,

Please indicate the source from the public account “Smart Sensor Network”!