Skip to content

The company adheres to the R&D philosophy of “originating from demand, identifying pain points, leveraging advantages, and serving the market”, establishing a research and development model that combines forward-looking strategies led by technological innovation with service strategies guided by market demand, producing one generation while researching the next.

The company’s core technologies focus on meeting customer needs and industrial development demands, primarily emphasizing video codecs, visual processors, display controllers, high-efficiency power conversion, high-precision analog-to-digital converters, artificial intelligence processors, and 3D perception technologies, along with supporting algorithms and systems. At the same time, by integrating high performance and low power consumption in balanced designs, power management chip design, ultra-high-definition video coding and decoding, software development across multiple application platforms, etc., the company forms competitive chip products and solutions, all of which have independent intellectual property rights or core technologies, boasting leading technological advantages.

After years of development and accumulation, the company has built a team of experienced talents, with a sound incentive mechanism and significant talent advantages.

The company has a research and development team specialized in system-level chip design and algorithm research, gathering and training a large number of excellent professionals in design R&D, engineering management, and planning and promotion. As of December 31, 2019, the company had a total of 727 employees, of which 553 were R&D personnel, accounting for 76.07%.

R&D expenses reached 310.08 million yuan, a year-on-year increase of 21.61%, with an R&D expense ratio of 22.03%, up 1.96 percentage points year-on-year. This is mainly due to the company’s high emphasis on R&D, sustained high investment in R&D expenses, and strong R&D innovation capabilities, ensuring that the company can develop products with leading performance that meet market demands.

3. Company’s Discussion and Analysis on Future Development

(1) Industry Structure and Trends

√ Applicable □ Not Applicable

The integrated circuit industry products are widely used in fields such as artificial intelligence, the Internet of Things, and automotive electronics, serving as the core of the information technology industry, and are a leading industry supporting economic and social development and ensuring national security. As a major manufacturing and consumption country of integrated circuits, China has always held a place in the global integrated circuit industry, which is currently in a rapid development phase.

According to the analysis by the Forward Industry Research Institute, from 2015 to 2019, the total output of China’s integrated circuit manufacturing industry showed a year-on-year upward trend, with a growth rate maintained at over 7%. According to preliminary statistics from the National Bureau of Statistics, from January to December 2019, China’s integrated circuit manufacturing industry achieved a cumulative output of 201.82 billion pieces, a year-on-year increase of 16.02%.

Data Source: National Bureau of Statistics

At the same time, the structure of China’s integrated circuit industry is becoming increasingly rationalized. According to statistics from the China Semiconductor Industry Association, the sales revenue of China’s integrated circuit industry in 2019 was 756.23 billion yuan, a year-on-year increase of 15.8%. Among them, the sales revenue of the integrated circuit design industry was 306.35 billion yuan, a year-on-year increase of 21.6%; the sales revenue of the integrated circuit manufacturing industry was 214.91 billion yuan, a year-on-year increase of 18.2%; and the sales revenue of the integrated circuit packaging and testing industry was 234.97 billion yuan, a year-on-year increase of 7.1%. Among the three segments of the integrated circuit industry, the design segment with relatively high technological content has the largest sales share, while the manufacturing industry’s growth rate also exceeds that of the packaging and testing industry, indicating a good development prospect for the integrated circuit design industry.

In 2019, China’s integrated circuit imports reached 300 billion USD, becoming the largest imported commodity in China. According to the goals set in the “Made in China 2025” plan, by 2020, the self-sufficiency rate of the semiconductor industry is expected to reach 40%. In recent years, a large number of policies have been introduced domestically to support the rapid development of the domestic semiconductor industry.

Data Source: China Semiconductor Industry Association

4. Intelligent Application Processor Chips

The company’s intelligent application processor chips are system-level SoC chips, and the application market can be divided into two major application areas: consumer electronics and intelligent IoT, as detailed below:

In 2019, the tablet market began to recover after a 4-year decline. In addition to traditional entertainment functions, users gradually accepted tablets as productivity tools, with stable sales increases for specialized tablets in education, office, and note-taking. The company’s main competitors in the tablet market are MediaTek and Allwinner Technology, where product performance and solution positioning as well as cost-effectiveness are the main competitive factors. The company strengthens the R&D of peripheral devices such as WiFi chips, further reducing system costs and enhancing product cost-effectiveness and competitiveness. In the specialized tablet market, the company effectively guides the market and increases market share through differentiated specifications of chips and targeted technical support or solutions.

2. Power Management Chips

Power management chips are responsible for power conversion, distribution, detection, and other energy management functions. The power management chip market is vast, with the latest research report from Transparency Market Research (TMR) indicating that from 2013 to 2019, the global power management chip market will have a compound annual growth rate of 6.1%. In 2012, the global power management chip market size reached 29.9 billion USD, and it is expected to grow to 46 billion USD by 2019. TI in the US is the industry leader, along with other large companies such as ADI, Maxim, and Infineon. Among domestic companies, companies like Shengbang Co., Ltd., Silan Microelectronics, and Silergy occupy leading positions. In the professional power chip industry, the integrated design and manufacturing model is common among large companies, such as TI having numerous wafer fabs, thus occupying a leading position in processing and cost. Compared to digital chips, power management chips have higher gross profit margins, and the low entry barriers for simple power management chips have attracted many small companies to compete fiercely, leading to unhealthy competition in the low-end market.

In the field of power management chips, the company focuses on high-value-added products in the market layout of power management chips that complement intelligent application processor SoC chips and customized phone matching chips, avoiding low-price competition. Customized chips are precisely designed according to customer needs, featuring high integration, with strong performance advantages in reliability, stability, and power consumption, optimizing costs for mobile phone manufacturers, suitable for large brand mobile phone manufacturers. At the same time, the company continues to promote PMU power management chip upgrade projects, increasing the support for PMU and continuously developing PMU-related products to enhance the company’s market competitiveness in this field.

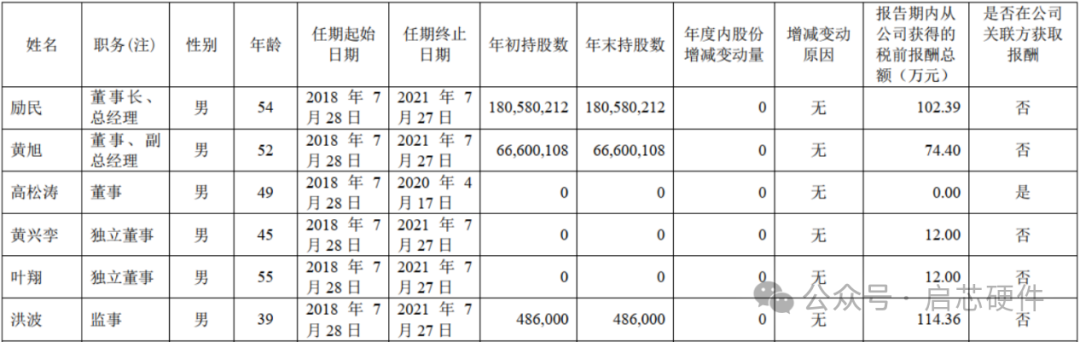

Section 8: Directors, Supervisors, Senior Management Personnel, and Employees

1. Changes in Shareholding and Compensation

(1) Changes in Shareholding and Compensation of Current and Resigned Directors, Supervisors, and Senior Management Personnel during the Reporting Period

√ Applicable □ Not Applicable

The 2021 financial report, with the widespread advancement of China’s 5G network and the continuous implementation of domestic AI application scenarios, indicates that the domestic AIoT market has entered a rapid growth cycle. We believe that the future is the “decade of new hardware”. Rockchip is in the right place at the right time, positioned at the forefront of this decade of growth. The significant growth in 2021 already signals that the company is entering a new rapid growth cycle, and we are confident in achieving high-speed development for many consecutive years.

(3) Future Situation Analysis and Response

1. We expect the overall economy to be relatively cold in 2022, but the overall market size for AIoT is expected to grow by over 20%. According to IDC data and forecasts, the global AIoT market size reached 226.4 billion USD in 2019, and is expected to reach 482 billion USD by 2022, with a compound growth rate of 28.65%. The overall supply of chips remains tight, with limited investment in mature processes like 28nm and above in recent years, and it takes more than 2 years to form effective production capacity. Therefore, the tight supply of mature processes may continue until the second half of 2023. However, compared to Rockchip, the supply in 2022, even for mature processes, will be significantly alleviated compared to 2021.

The company’s core technologies focus on meeting customer needs and industrial development demands, primarily emphasizing video codecs, visual processors, display controllers, high-efficiency power conversion, high-precision analog-to-digital converters, artificial intelligence processors, and 3D perception technologies, along with supporting algorithms and systems. At the same time, by integrating high performance and low power consumption in balanced designs, power management chip design, ultra-high-definition video coding and decoding, software development across multiple application platforms, etc., the company forms competitive chip products and solutions, all of which have independent intellectual property rights or core technologies, boasting leading technological advantages.

After years of development and accumulation, the company has built a team of experienced talents, with a sound incentive mechanism and significant talent advantages.

The company has a research and development team specialized in system-level chip design and algorithm research, gathering and training a large number of excellent professionals in design R&D, engineering management, and planning and promotion. As of December 31, 2019, the company had a total of 727 employees, of which 553 were R&D personnel, accounting for 76.07%.

R&D expenses reached 310.08 million yuan, a year-on-year increase of 21.61%, with an R&D expense ratio of 22.03%, up 1.96 percentage points year-on-year. This is mainly due to the company’s high emphasis on R&D, sustained high investment in R&D expenses, and strong R&D innovation capabilities, ensuring that the company can develop products with leading performance that meet market demands.

3. Company’s Discussion and Analysis on Future Development

(1) Industry Structure and Trends

√ Applicable □ Not Applicable

The integrated circuit industry products are widely used in fields such as artificial intelligence, the Internet of Things, and automotive electronics, serving as the core of the information technology industry, and are a leading industry supporting economic and social development and ensuring national security. As a major manufacturing and consumption country of integrated circuits, China has always held a place in the global integrated circuit industry, which is currently in a rapid development phase.

According to the analysis by the Forward Industry Research Institute, from 2015 to 2019, the total output of China’s integrated circuit manufacturing industry showed a year-on-year upward trend, with a growth rate maintained at over 7%. According to preliminary statistics from the National Bureau of Statistics, from January to December 2019, China’s integrated circuit manufacturing industry achieved a cumulative output of 201.82 billion pieces, a year-on-year increase of 16.02%.

Data Source: National Bureau of Statistics

At the same time, the structure of China’s integrated circuit industry is becoming increasingly rationalized. According to statistics from the China Semiconductor Industry Association, the sales revenue of China’s integrated circuit industry in 2019 was 756.23 billion yuan, a year-on-year increase of 15.8%. Among them, the sales revenue of the integrated circuit design industry was 306.35 billion yuan, a year-on-year increase of 21.6%; the sales revenue of the integrated circuit manufacturing industry was 214.91 billion yuan, a year-on-year increase of 18.2%; and the sales revenue of the integrated circuit packaging and testing industry was 234.97 billion yuan, a year-on-year increase of 7.1%. Among the three segments of the integrated circuit industry, the design segment with relatively high technological content has the largest sales share, while the manufacturing industry’s growth rate also exceeds that of the packaging and testing industry, indicating a good development prospect for the integrated circuit design industry.

In 2019, China’s integrated circuit imports reached 300 billion USD, becoming the largest imported commodity in China. According to the goals set in the “Made in China 2025” plan, by 2020, the self-sufficiency rate of the semiconductor industry is expected to reach 40%. In recent years, a large number of policies have been introduced domestically to support the rapid development of the domestic semiconductor industry.

Data Source: China Semiconductor Industry Association

4. Intelligent Application Processor Chips

The company’s intelligent application processor chips are system-level SoC chips, and the application market can be divided into two major application areas: consumer electronics and intelligent IoT, as detailed below:

In 2019, the tablet market began to recover after a 4-year decline. In addition to traditional entertainment functions, users gradually accepted tablets as productivity tools, with stable sales increases for specialized tablets in education, office, and note-taking. The company’s main competitors in the tablet market are MediaTek and Allwinner Technology, where product performance and solution positioning as well as cost-effectiveness are the main competitive factors. The company strengthens the R&D of peripheral devices such as WiFi chips, further reducing system costs and enhancing product cost-effectiveness and competitiveness. In the specialized tablet market, the company effectively guides the market and increases market share through differentiated specifications of chips and targeted technical support or solutions.

2. Power Management Chips

Power management chips are responsible for power conversion, distribution, detection, and other energy management functions. The power management chip market is vast, with the latest research report from Transparency Market Research (TMR) indicating that from 2013 to 2019, the global power management chip market will have a compound annual growth rate of 6.1%. In 2012, the global power management chip market size reached 29.9 billion USD, and it is expected to grow to 46 billion USD by 2019. TI in the US is the industry leader, along with other large companies such as ADI, Maxim, and Infineon. Among domestic companies, companies like Shengbang Co., Ltd., Silan Microelectronics, and Silergy occupy leading positions. In the professional power chip industry, the integrated design and manufacturing model is common among large companies, such as TI having numerous wafer fabs, thus occupying a leading position in processing and cost. Compared to digital chips, power management chips have higher gross profit margins, and the low entry barriers for simple power management chips have attracted many small companies to compete fiercely, leading to unhealthy competition in the low-end market.

In the field of power management chips, the company focuses on high-value-added products in the market layout of power management chips that complement intelligent application processor SoC chips and customized phone matching chips, avoiding low-price competition. Customized chips are precisely designed according to customer needs, featuring high integration, with strong performance advantages in reliability, stability, and power consumption, optimizing costs for mobile phone manufacturers, suitable for large brand mobile phone manufacturers. At the same time, the company continues to promote PMU power management chip upgrade projects, increasing the support for PMU and continuously developing PMU-related products to enhance the company’s market competitiveness in this field.

Section 8: Directors, Supervisors, Senior Management Personnel, and Employees

1. Changes in Shareholding and Compensation

(1) Changes in Shareholding and Compensation of Current and Resigned Directors, Supervisors, and Senior Management Personnel during the Reporting Period

√ Applicable □ Not Applicable

The 2021 financial report, with the widespread advancement of China’s 5G network and the continuous implementation of domestic AI application scenarios, indicates that the domestic AIoT market has entered a rapid growth cycle. We believe that the future is the “decade of new hardware”. Rockchip is in the right place at the right time, positioned at the forefront of this decade of growth. The significant growth in 2021 already signals that the company is entering a new rapid growth cycle, and we are confident in achieving high-speed development for many consecutive years.

(3) Future Situation Analysis and Response

1. We expect the overall economy to be relatively cold in 2022, but the overall market size for AIoT is expected to grow by over 20%. According to IDC data and forecasts, the global AIoT market size reached 226.4 billion USD in 2019, and is expected to reach 482 billion USD by 2022, with a compound growth rate of 28.65%. The overall supply of chips remains tight, with limited investment in mature processes like 28nm and above in recent years, and it takes more than 2 years to form effective production capacity. Therefore, the tight supply of mature processes may continue until the second half of 2023. However, compared to Rockchip, the supply in 2022, even for mature processes, will be significantly alleviated compared to 2021.