Arm has long been hailed as the “Swiss Army Knife” of the chip industry, dominating the embedded field. However, the company’s strategic vision clearly extends beyond this, as rumors about Arm designing its own chips have been persistent.

Yesterday, Arm CEO René Haas explicitly stated that the company is officially developing its own chips. This marks a significant shift from Arm’s long-standing core model of “licensing chip design blueprints to other companies.”

From CSS to Self-Designed Chips

Haas told the media that the finished chips are the physical embodiment of Arm’s product called the Compute Subsystem (CSS). “We have consciously decided to invest more funds — (in) going beyond (designing) and building something, building Chiplets and even the possibility of solutions.“

Arm has been exploring self-designed chips for some time. In recent years, Arm has been promoting semi-customized IP integration services, expanding revenue and increasing profits through the “ Compute Subsystem (CSS)” platform, combined with high-margin new products and increasing per-chip royalties. Direct sales of self-designed chips to customers may be an extension of this direction.

In December 2024, during the court hearing of the technology licensing lawsuit between Arm and Qualcomm, Qualcomm accused Arm of competing with customers by providing CSS services in areas such as client and data center processors. At that time, Qualcomm’s legal team presented documents from Haas to the Arm board, indicating that Arm was considering directly designing chips to sell to customers, which would make it a direct competitor to clients like Qualcomm. In response, Haas explicitly denied, stating that Arm “does not manufacture chips and has never ventured into that field.”

However, by February 2025, the Financial Times reported that Arm had initiated a self-designed chip project, with the first product expected to launch as early as this summer, manufactured by TSMC, and Meta may become one of the first customers. This means that Arm plans to integrate its CPU, GPU, and other IP with CSS solutions into a system platform, ultimately transforming into physical chips for external sales — although this will lead to competition with customers, its primary target appears to be the more profitable data center market, which may primarily impact this field in the short term.

Financial reports indicate that Arm had sales of $1.05 billion in the first quarter, slightly below the market expectation of $1.06 billion; adjusted earnings per share were 35 cents, in line with expectations. For the second fiscal quarter, Arm predicts adjusted earnings per share between 29 cents and 37 cents, with the median of this range ( 33 cents) lower than the average analyst expectation of 36 cents; revenue expectations are between $1.01 billion and $1.11 billion, consistent with market expectations of $1.06 billion.

Four Key Pieces of Information: Stargate, AI, CSS, Chiplets

It is noteworthy that while releasing the second fiscal quarter performance forecast, Arm also held a conference call. The wealth of information disclosed during the meeting indicates that its ongoing exploration and layout in multiple cutting-edge fields may be the foundation for Arm’s decision to personally enter the chip manufacturing arena:

First, the collaboration with SoftBank’s “Stargate.” Haas stated that the business relationship with SoftBank has expanded to help realize a greater and broader vision for artificial intelligence. From a macro perspective, Stargate is a joint venture between SoftBank and OpenAI, planning to expand the total investment scale to 10 gigawatts in the coming years. This requires a massive amount of computing resources and provides enormous potential for various design opportunities.

“SoftBank has a very broad vision for artificial intelligence, and we hope to help them realize that vision. We will not mention specific products and application areas, but today, all Stargate projects use Arm as the core CPU, and we have a unique opportunity to provide solutions. Much work has already begun, but we cannot disclose any specific information about products or timelines.“ Haas said.

Second, the ongoing investment in AI. Haas stated that driven by the insatiable computing demands of artificial intelligence, Arm has started the 2026 fiscal year with strong momentum. Arm is the only one providing AI performance across the full power and performance range from milliwatts to megawatts. Especially in the field of artificial intelligence, its leadership is amplified by an unparalleled software development ecosystem. Over 22 million developers, accounting for over 80% of global developers, build on Arm.

Currently, over 70,000 companies run AI workloads on Arm Neoverse data center chips, a year-on-year growth of 40%, and a 14-fold increase since 2021. Arm Neoverse CPUs now support the world’s most important AI infrastructure, includingNVIDIA Grace, AWS Graviton, Google Axion, and Microsoft Cobalt. For example, driven by performance and high-efficiency computing, NVIDIA Grace Blackwell’s energy efficiency is 25 times higher than previous systems based on x86. It is expected that this year, the market share of top-tier hyperscale enterprises based on Arm Neo chips will reach nearly 50%.

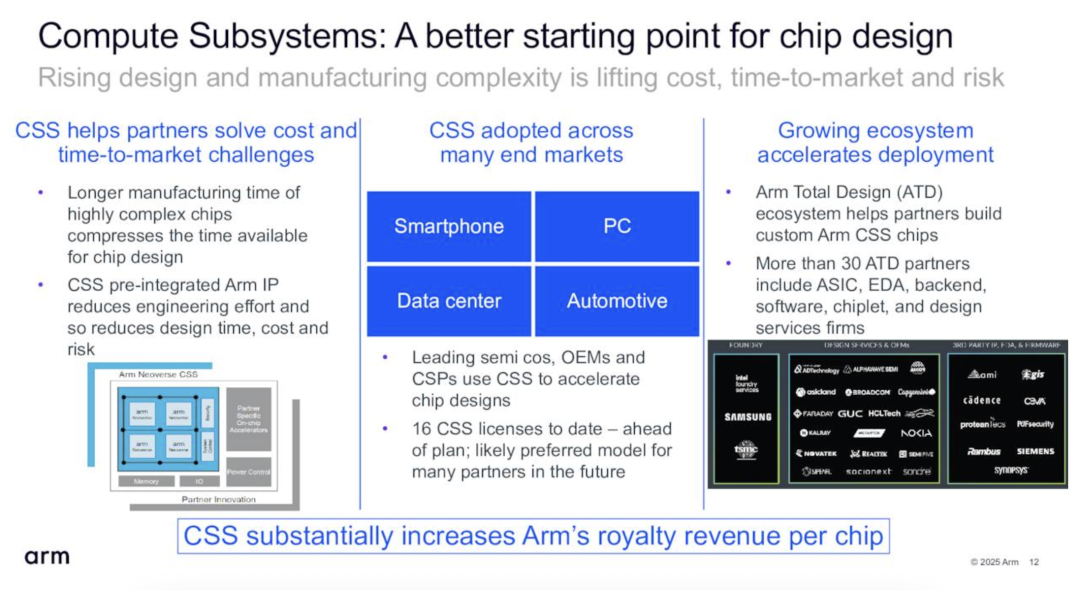

Third, the CSS subsystems have significantly enhanced Arm’s royalty fees. Currently, the first generation of CSS has been launched, with five customers, providing royalties that are double that of Armv9. So far, Arm has signed 16 CSS licenses with 10 companies, more than double the number from the same period last year. Five companies have begun shipping CSS-based chips, all of which are market leaders. This quarter, Arm signed three additional CSS licenses with existing CSS customers, two for data centers and one for PCs, more than double from a year ago. Recently, Samsung’s Exynos 7 Galaxy Flip 2500 and a certain smartphone manufacturer have adopted the latest Arm Compute Subsystem platform.

“We will continue to explore the possibility of transitioning from the current platform to subsystems, Chiplets, and potential full-end solutions. Subsequent generations of CSS platforms offer greater value, functionality, and time to market, bringing us the highest royalty rates we have seen to date. This includes the launch of platforms optimized for AI-driven automotive workloads, such as the Zena CSS. Similarly, in this quarter, a major smartphone OEM has committed to using the GPU platform to accelerate graphics and AI,” Haas said.

Fourth, the exploration of Chiplets has reached a deep level. Haas stated that many small chips currently under development are based on Arm IP, and have been supported by the Arm Total Design ecosystem for small chip development, one of the outcomes being the multi-vendor program Project Leapfrog. Arm is now studying the feasibility of moving beyond the current platform to other subsystems, Chiplets, or potential complete solutions.

Currently, Arm’s small chip system architecture (CSA) has the support of over 70 partners. Arm believes that the highlight of small chips lies in supporting modular design, allowing independent scaling of computing or memory, effectively diversifying SKUs, and optimizing power/ thermal budgets more finely. For smaller players, this opens the door to enter complex markets without the need for single-chip SoC investments. Through Arm KleidiAI, developers can run inference tasks across different hardware on a unified AI software stack from the cloud to Raspberry Pi.

The Impact of Arm’s Self-Designed Chips

The market has reacted strongly to this, primarily due to the following key impacts:

First, this will break the long-standing neutrality and trust between Arm and its existing customers. By launching self-designed chips, Arm will transform from a pure partner to a direct competitor to major clients like NVIDIA and Qualcomm. Customers may worry that Arm will withhold advanced technologies in future licensing, prioritizing the latest technologies for its own products, thereby weakening their competitiveness in the market.

Second, this may be an inevitable choice for Arm to pursue higher profit growth. Although its IP licensing business is very successful, the royalties and licensing fees still have a ceiling compared to the enormous profits that can be obtained from directly selling high-performance chips. Especially in the wave of AI, the demand for high-performance, energy-efficient computing chips in data centers is exploding, growing into a trillion-dollar track.

Furthermore, Arm is also taking this step to better showcase the full potential of its technology. By designing and launching its own “demonstrative” or “benchmark” chips, Arm can demonstrate the ultimate performance and efficiency of its latest architecture to the market, especially in competition with Intel’s x86 architecture, this move can more powerfully promote the adoption of its technology in high-end markets such as data centers.

It is worth noting that Arm does not intend to establish its own Fab, but will adopt a Fabless model like Apple and NVIDIA. Nevertheless, from design to tape-out, and then to market launch, the entire process is still a comprehensive test of Arm’s capabilities and introduces new variables to the semiconductor industry landscape.

In my opinion, Arm’s entry into chip manufacturing is perhaps expected. Currently, the AI data center field is very hot, and Arm itself has a very comprehensive solution and has explored the subsystem field for many years, making it reasonable to seize the market. This business model is not unique to Arm; for example, BYD also provides batteries, chips, and other solutions while manufacturing cars. Advanced subsystem solutions, through silicon validation of chips, are actually more convincing.

· END ·

Follow the subscription account of EEWorld: "Robot Development Circle"

Reply "DS" to receive the complete version of "DeepSeek: From Beginner to Expert"

Scan to add the assistant and reply “robot”

to join the group and exchange experiences face-to-face with electronic engineers